結合穩定型複式交易策略

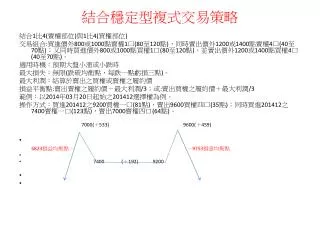

結合穩定型複式交易策略. 結合 1 比 4( 賣權部位 ) 與 1 比 4( 買權部位 ) 交易組合 : 買進價外 800 或 1000 點賣權 1 口 (80 至 120 點 ) ,同時賣出價外 1200 或 1400 點賣權 4 口 (40 至 70 點 ) ;又同時買進價外 800 或 1000 點買權 1 口 (80 至 120 點 ) ,並賣出價外 1200 或 1400 點買權 4 口 (40 至 70 點 ) 。 適用時機:預期大盤小漲或小跌時 最大損失:無限 ( 跌破均衡點,每跌一點虧損三點 ) 。 最大利潤: 結算於賣出之買權或賣權之履約價

結合穩定型複式交易策略

E N D

Presentation Transcript

結合穩定型複式交易策略 結合1比4(賣權部位)與1比4(買權部位) 交易組合:買進價外800或1000點賣權1口(80至120點),同時賣出價外1200或1400點賣權4口(40至70點);又同時買進價外800或1000點買權1口(80至120點),並賣出價外1200或1400點買權4口(40至70點)。 適用時機:預期大盤小漲或小跌時 最大損失:無限(跌破均衡點,每跌一點虧損三點)。 最大利潤:結算於賣出之買權或賣權之履約價 損益平衡點:賣出賣權之履約價-最大利潤/3;或:賣出買權之履約價+最大利潤/3 範例:以2014年03月20日起始之201412選擇權為例。 操作方式:買進201412之9200買權一口(81點),賣出9600買權四口(35點);同時買進201412之7400賣權一口(123點),賣出7000賣權四口(64點)。 7000(+533) 9600(+459) 6823損益均衡點- -9753損意均衡點 • 7400 (+192) 9200