Download

1 / 24

250 likes | 651 Vues

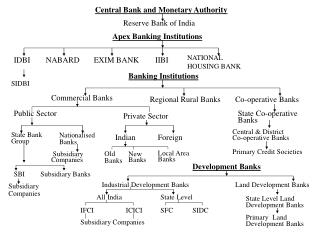

Central Bank and Monetary Authority. Reserve Bank of India. Apex Banking Institutions. NATIONAL HOUSING BANK. IDBI. NABARD. EXIM BANK. IIBI. Banking Institutions. SIDBI. Commercial Banks. Regional Rural Banks. Co-operative Banks. Public Sector. Private Sector. State Co-operative

E N D

Central Bank and Monetary Authority Reserve Bank of India Apex Banking Institutions NATIONAL HOUSING BANK IDBI NABARD EXIM BANK IIBI Banking Institutions SIDBI Commercial Banks Regional Rural Banks Co-operative Banks Public Sector Private Sector State Co-operative Banks Central & District Co-operative Banks Nationalised Banks Indian Foreign State Bank Group Primary Credit Societies Old Banks Local Area Banks Subsidiary Companies New Banks Development Banks SBI Subsidiary Banks Industrial Development Banks Land Development Banks Subsidiary Companies All India State Level State Level Land Development Banks IFCI ICICI SFC SIDC Primary Land Development Banks Subsidiary Companies

CONCLUDING OBSERVATIONS • Challenge to the Public Sector Banks to Retain their share • Stiff Competition by New Private Sector Banks to the Foreign Banks • Focus primarily on Profitability • Interest Rate Spread has declined in case of Public & Private Sector Banks • Public Sector has brought a reduction in the Wage Component

OFF-BALANCE SHEET ACTIVITIES • Loan Commitments • Guarantees • Swap & Hedging Transactions • Investment Banking Activities

RISKS OF OBS ACTIVITIES • Operational risks • Funding Risks • Position Risks • Credit Risks

ROUND UP • SBI edges up position • NABARD plans to enter retail banking • Commercial Banks beef up Tier- II Capital • NPA’s of 27 PSBs Rise

LIKELY CHALLENGES FACING BANKS Transparency in Balance Sheets New Content in Corporate Planning Interest Deregulation Asset / Liability Management Risk Management Prudential Regulations Provisions Income Recognition & Capital Adequacy Norms Recourse to Market Competition Changing Mindsets 1991-92 2000-01

BANKING SECTOR Introduction to Banking BANKING (% PENETRATION ) PUBLIC SECTOR BANK 70% FOREIGN BANK 8% PRIVATE BANK 22 %

TRADITIONAL BANKING SECTOR • Highly segmented market • Limited competition • Less alternative products offered • Minimal use of technology • Preponderance of Brick & Mortar • Controlled foreign exchange regime • Highly regulated financial sector

REFORM MEASURES • Direct access to Capital Market • Better transparency through disclosure • Prudential accounting norms • Deregulation of Interest Rate • Bank Rate lowered by 50 basis point from 7% to 6.5% • CRR slashed in two stages from 7.5% to 5.5% ( Reduction by 200 basis points ) • Interest on CRR Balances with RBI raised to 6.5% from 6%

The result Rs 8000 crore unlocks MORE MONEY WITH BANKS TO LEND FALL IN CRR LENDING ACTIVITY INVESTMENT OUTPUT ECONOMIC GROWTH

LOOPHOLES • Excess staff in PSB • Low technology penetration • High NPA’s • Less No. of products under one roof • Large No. of unprofitable branches

PARADIGM SHIFT • One stop service to customer • Technology & I.T. penetration • From “ Brick & Mortar ” to “ Click & Mortar ” • Emerging trend of Universal Banking

UNIVERSAL BANKING WORKING CAPITAL TERM LENDING UNIVERSAL BANK MORTGAGE INSURANCE CAPITAL MARKET

Private Sector Indian Banks ICICI Bank HDFC Bank Indusind Bank GTB UTI Bank Centurion Bank Vyasa Bank Federal Bank etc…. Private Sector Foreign Banks Citibank Stanchart HSBC Bank of Baroda ABN Amro AM-EX etc…. LEADING BANKS

TECHNOLOGY IMPACT • Save in time • Save in cost • Save in Paper work • Increase in efficiency • Increase in service • Increase in transparency

Role of Commercial Banks • Financial Interface • Facilitating Payments Mechanism • Providing Financial Services • Other Misc. Services

CHALLENGES • Financial Disintermediation • Competitions from Mutual Funds • Deregulation of Interest Rate • Declining Spread • Burden of NPA’s • Issuing Capital Adequacy Norms • Asset / Liability Management • Technology & Computerisation • Disclosure & Financial Transparency • VRS • Increased Accountability

STRATEGIES • Retail Banking Initiatives • Multiple Delivery Channels • “ Anytime & Anywhere Banking ” • Focus on fee based income • Better Asset / Liability Management • Proper Risk Management • Supervision of Loans & Check on NPA’s • Financial Services Supermarket • Customer Orientation Approach • Better Corporate Governance