Dynamic Decision Making Based on Past Experience in Risk Perception

180 likes | 274 Vues

Explore how past experiences influence risk perception in decision-making processes, with a focus on insurance demand and intertemporal decisions. This paper presents modeling techniques and empirical evidence on the impact of past events on choice behaviors.

Dynamic Decision Making Based on Past Experience in Risk Perception

E N D

Presentation Transcript

Dynamic Decision Making when Risk Perception depends on Past Experience Michèle COHEN, CES, Université de Paris 1 Johanna ETNER, GAINS, Univ. du Maine et CES, Paris 1 Meglena JELEVA, GAINS, Univ. du Maine et CES, Paris 1

Introduction • Behavior at a point of time • Dynamic choice • An illustrative example: past experience and insurance demand FUR XII, Rome 2006

1. Introduction (1/3) • Risk and wealth perception may be influenced by the agent context when he takes his decisions • Context = framing, past experience, feelings etc. • In this paper: focus on past experience • Some empirical evidence: • Relation between insurance decisions and individual prior-experience related to risk: • Kunreuther (1996), Brown, Hoyt (2000); • Weather conditions influence investment decisions: • Hirshleifer, Shumway (2003) FUR XII, Rome 2006

1. Introduction (2/3) • Past experience can concern different events: • Past realizations on the decision-relevant events (accidents); • Realizations of events, independant on the relevant decision problem (weather). • To better capture the long term impact of past experience, we model intertemporal decisions. • A first step consists in considering a one period decision problem where preferences are defined on pairs (decision, past experience); FUR XII, Rome 2006

1. Introduction (3/3) • We adapt RDU axiomatic system of Chateauneuf (1999); • The obtained criterion is used in the construction of a dynamic choice model under risk; • We model intertemporal decisions by a recursive model à la Kreps, Porteus (1978). FUR XII, Rome 2006

2. Behavior at a point of time (1/4) • Decision problem characterized by: • L: set of lotteries over Z R; • S: set of past (realized) states; • (s , L): « past experience dependent lottery »; • : preference relation on S L. FUR XII, Rome 2006

2. Behavior at a point of time (2/4) • Preferences representation on S L in 3 steps: • for any fixed s, s on s L, from Chateauneuf (1999): • S Z on S Z, axioms to guarantee the existence of a utility function on S Z. • Additional axioms to guarantee the consistency of the conditional preference relations. FUR XII, Rome 2006

2. Behavior at a point of time (3/4) • Theorem on S L is representable by a function V: FUR XII, Rome 2006

2. Behavior at a point of time (4/4) • Some particular cases: • Realized states influence only the probability transformation function: • Realized states influence only the utility function: FUR XII, Rome 2006

3. Dynamic choice (1/5) • In the spirit of Kreps, Porteus modelling • Some notations and assumptions: • T periods; • Zt = Z R; • Past experience at time t: st = (e0, e1,…,et) with et Et; • St : set of possible past experiences up to time t such that: S0 = E0 and St = St-1 Et; • M(Et): set of distributions on Et. FUR XII, Rome 2006

3. Dynamic choice (2/5) • At period T, • LT: set of distributions on ZT ; • XT: set of closed non empty subsets of LT. • Recursively, • Lt: set of probability distributions on Ct = Zt Xt+1M(Et+1), with Xt+1 the set of closed non empty subsets of Lt+1. FUR XII, Rome 2006

3. Dynamic choice (3/5) • For the same period, assumption of compound lotteries reduction (ROCL) is made between distributions of wealth and events. • Between two consecutive periods, ROCL remains relaxed. FUR XII, Rome 2006

3. Dynamic choice (4/5) • For each period t, t on st Lt, for a given st represented by: • Temporal consistency axiom For any t, s t, et+1,zt, xt+1, x’t+1, FUR XII, Rome 2006

3. Dynamic choice (5/5) • Representation theorem There exist 2 sequences of utilities ut and vt and a sequence of t such that: FUR XII, Rome 2006

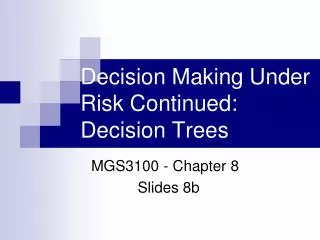

4. An illustrative exemple (1/4) • Insurance demand • An individual faces a risk of loss and has to choose an amount of insurance coverage, ; • Insurance contracts are subscribed for one period (year) • Risk characteristics: • loss of an amount L with probability p; • P(loss in period t/ loss in period t-1) = p FUR XII, Rome 2006

4. An illustrative exemple (2/4) • Optimal insurance strategy of an individual for 3 periods of time? • Insurance contracts: subscibed for 1 year, fair premium • Past experience at t: sequence of loss realizations before t et= e if « loss at period t », et= e’ if « no loss at period t » st = (st-1, et) FUR XII, Rome 2006

L3 z3 a3 z2 p 1-p z3 z1 L2 a2 s2=(e0,e1,e2) p z’3 z2 L’3 a’3 p s1=(e0,e1) 1-p 1-p z’3 s’2=(e0,e1,e’2) L1 z0 a1 p z’’3 z’2 L’’3 s0=e0 a’’3 p 1-p L’2 s’’2=(e0,e’1,e2) 1-p z’’3 z1 a’2 z’’’3 p z’2 L’’’3 s’1=(e0,e’1) a’’’3 1-p s’’’2=(e0,e’1,e’2) z’’’3 1-p 4. An illustrative exemple (3/4) p FUR XII, Rome 2006

4. An illustrative exemple (4/4) • Let • Results: • 1 = 0; • 2 = 0 if no loss at period 1; 2 [0, 1] if loss at period 1; • 3 = 0 if no loss at periods 1 and 2; 3 = 1 if loss at periods 1 and 2; 3 [0, 1] else. FUR XII, Rome 2006