DEBENTURE

Understand debentures in business with this comprehensive guide. Learn about definition, types, documents, registration, cases, receivership, and more. Essential for business students.

DEBENTURE

E N D

Presentation Transcript

DEBENTURE SIRHOLY GIMPA BUSINESS SCHOOL

OUT LINE SESSION 1: Definition of debentures SESSION 2: Types of debentures SESSION 3: Documents relating to debentures SESSION 4: Registration of particulars of charge SESSION 5: Case review SESSION 6: Appointment of a receiver

SESSION 1: DEFINITION OF DEBENTURES According to s. 80 (2) a debenture is a written acknowledgement of indebtedness by a company setting out the terms and conditions of the loan. A debenture form part of the company's “loan capital) (s. 80 (1)).

SESSION 1: DEFINITION OF DEBENTURES We have debenture simpliciter and debenture stock. A debenture stock is a unit of a block of loan of a prescribed amount. The block of loan – the single debt is the debenture. Loan-block is acknowledged in a document called the debenture and each unit of the loan by debenture stock certificate.

SESSION 1: DEFINITION OF DEBENTURESFeatures of debenture stock • There is a block loan of a prescribed amount to the company; • The block loan is created by deed; • The block loan is divided into parts; • The different parts may be issued by different holders; and • The parts are represented by debenture stock certificate.

SESSION 1: DEFINITION OF DEBENTURES One merit of a DS is that the company can obtain one vast loan of a prescribed amount with different contributors advancing smaller and more affordable funds.

SESSION 1: DEFINITION OF DEBENTURESParticulars of a debenture • Amount of money lent; • The rate of interest; • The amount of monthly payments; • The date when the principal and the interest will be paid off; • The circumstances when the principal becomes payable; and • The security for the loan if any.

SESSION 1: DEFINITION OF DEBENTURESDebenture holders and shareholders • Debenture holders are creditors of the company and not members, hence have no right to attend and vote at meetings. • Shares must not be generally be issued at a discount to shareholders but this does not apply to debenture holders.

SESSION 1: DEFINITION OF DEBENTURESDebenture holders and shareholders 3. A company is prohibited from purchasing its own shares but there is no such prohibition on a company from purchasing its own debentures. 4. Interest on debentures must be paid at all means when they fall due and can be paid out of profits or capital but dividends can only be paid out of profits, not capital.

SESSION 1: DEFINITION OF DEBENTURESDebenture holders and shareholders 5. Interest on debentures is charged before determining a company’s profit. They are treated as an expense which are deducted before determining profit. Taxes are then paid on debenture interest. Dividends are however, paid out of the corporate profits which have already been taxed.

SESSION 2: TYPES OF DEBENTURES There are various types of debentures: • Perpetual or redeemable • Convertible or non-convertible • Naked or secured

SESSION 2: TYPES OF DEBENTURESPerpetual debentures or redeemable debentures A perpetual debenture according to s. 84 is one which is not redeemable by the company. A redeemable debenture is one which the company can redeem. A debenture can only be redeemed on the happening of an event, on the expiration of period. The redemption shall be cancelled if the Regulations forbid it.

SESSION 2: TYPES OF DEBENTURESConvertible debentures or non-convertible debentures A convertible debenture is one that, in lieu of redemption or repayment, may, at the option of the holder be converted into shares in the company upon such terms as are stated in the debenture. A non-convertible debenture cannot be converted into shares.

SESSION 2: TYPES OF DEBENTURESNaked debentures or Secured debentures A naked debenture is one which creates no charge over the company’s property to secure the loan. A receiver or a manager shall not be appointed as a means of enforcing debentures not secured by any charge s. 88 (4). A secured debenture creates a charge either fixed or floating charge.

SESSION 2: TYPES OF DEBENTURESSecured debentures A debenture secured by a fixed charge is a loan to a company for which specific property of the company is used as security to ensure repayment of the loan. A debenture secured by floating charge is one in which the general assets of the company is used as a security and nothing in particular is used as security.

SESSION 2: TYPES OF DEBENTURESSecured debentures In Illingworth v Houldsworth Lord Macnaghten posits that: “A specific charge, I think, is one that without more fastens on ascertained and definite property capable of being ascertained and defined; a floating charge, on the other hand, is ambulatory and shifting in its nature, hovering over and so to speak floating with the property which is intended to affect, until some event occurs or some act is done which causes it to settle and fasten on the subject of the charge within its reach and grasp.”

SESSION 2: TYPES OF DEBENTURESSecured debentures In Re Yorkshire Woolcombers Association Ltd., Romer, L. J. postulates three characteristics of a floating charge: • If it is a charge on a class of assets on a company present and future; • If that class is one which, in the ordinary course of the business of the company, would be changing from time to time; and • If you find that by the charge it is contemplated that, until some future step is taken by or on behalf of those interest in the charge, the company may carry on its business in the usual way as far as concerns the particular class of assets.

SESSION 2: TYPES OF DEBENTURESSecured debentures Edusei J. said in the case of George Cohen (W.A.) Ltd. V Comet Construction Co. Ltd: Ghana Commercial Bank that: “A floating charge which is quiet distinct from a specific charge does not fasten on any definite property but is an equitable charge on property which is constantly changing, e. g. stock in trade. However, if a debenture holder, on the happening of some event stated in the debenture takes steps to have the floating charge crystallized the charge then becomes specific or fixed charge.”

SESSION 2: TYPES OF DEBENTURESCrystallization This refers to the events which trigger a floating charge to become fixed and enforceable. Edusei J. posits that crystallization takes place, among other things, and in this case, the judgment of a debtor cannot deal with the property compromised in the security without the consent of the debenture holders.

SESSION 2: TYPES OF DEBENTURESCrystallization S. 87 (1) & (2) defines a float charge and crystallization as follows: • A floating charge is an equitable charge over the whole or a specific part of the company’s undertaking and assets both present and future; • The security becomes enforceable and the holder thereof pursuant to power in that behalf in the debenture or the deed securing the same, appoints a receiver or manager or enters into possession of such assets; • The courts appoints a receiver or manager of such assets on the application of the holder; • The company goes into liquidation; and • On the happening of any such events the charge shall be crystallized.

SESSION 2: TYPES OF DEBENTURESCrystallization-floating charge The courts may appoint a receiver or manager: • When the security of the debenture holder becomes enforceable; • Even though the security has not become enforceable it nevertheless is in jeopardy

SESSION 2: TYPES OF DEBENTURESCrystallization-floating charge Security is in jeopardy when events occur or about to occur which satisfy the courts that it is reasonable in the interest of the debenture holder that the company should retain the power to dispose of its assets (s. 88 (3)).

SESSION 2: TYPES OF DEBENTURESCrystallization-fixed charge A fixed charge generally has priority over a floating charge affecting the same property. In exceptional cases, a floating charge will have priority over a fixed charge affecting the same property if the terms of which the floating charge was granted prohibited the company from granting any later charge was granted had actual notice of the said prohibition at the time when the charge was granted to him (s. 87 (4)).

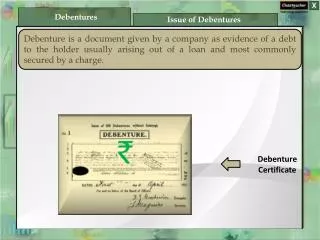

SESSION 3: DOCUMENTS RELATING TO DEBENTURES A debenture stock is represented by a debenture certificate. It is also crucial to have a register of debenture holders. Within 2 months after the allotment of debentures a company must issue a certificate to the holders.

SESSION 3: DOCUMENTS RELATING TO DEBENTURESDebenture stock certificate According to s. 82 (1) a company shall issue a debenture stock certificate under the common seal of the company. A company may also issue a new or certified true copy of a defaced, lost or destroyed certificate upon the payment by the debenture holder out-of-pocket expenses for investigating the reported defacement, loss or destruction.

SESSION 3: DOCUMENTS RELATING TO DEBENTURESDebenture stock certificate As with share certificate, statements made in a debenture or debenture stock certificate under the company’s seal have two related effects.

SESSION 3: DOCUMENTS RELATING TO DEBENTURESDebenture stock certificate Effects of debenture stock certificate 1. According to s.83 (1) statements made in a debenture stock certificate under the common seal of the company shall be prima facie evidence of the title of the person named therein as the registered holder and of the amounts secured by these documents. 2. S.83 (2) states that the company may be stopped from denying the continued accuracy of statements in a certificate and if anyone shall change his position to his detriment relying in good faith on accuracy of the statement on the certificate, the company shall compensate such a person for any loss.

SESSION 3: DOCUMENTS RELATING TO DEBENTURESRegister of Debenture Holders s. 96 (1) maintain that a company which issue debentures shall maintain a register of debenture holders. This register shall be kept and maintained at the same address at which the register of members is kept (s. 96(2)). If there are more than 50 debenture holders, an index is required and a notice sent to the Registrar when the register is kept at any other place than the registered office of the company.

SESSION 4: REGISTRATION OF PARTICULARS OF CHARGE The Code only required the particulars of a charge created by a company together with the original or certified copy of the instrument, be registered with the Registrar within 28 days of the creation of the charge (s. 107 (1)). It is the particulars of the charge and not the charge itself that is registered.

SESSION 4: REGISTRATION OF PARTICULARS OF CHARGEParticulars of the charge to be registered • The date of creation of the charge; • The nature of the charge; • The amount secured by the charge; • Short particulars of the property charged; • The person entitled to the charge; • For a floating charge, the nature of any restrictions on the power of the company to grant further charges ranking in priority with the charge thereby created.

SESSION 4: REGISTRATION OF PARTICULARS OF CHARGEFailure to register charge The failure to register the particulars of the charge shall make the charge void to the extent that it purports to confer security on the company’s property. The fact that the charge becomes void does not prejudice any contract for repayment of the money thereby secured: as soon as the charge is void, the money secured shall be immediately become payable, notwithstanding any provisions to the contrary in any contract (s. 107 (2)).

SESSION 4: REGISTRATION OF PARTICULARS OF CHARGEDelivery of particulars to the Registrar for registration In accordance with s. 111 of Act 179, it is the duty of the company to deliver the particulars mentioned earlier to the Registrar for registration, but any person interested in the particulars can also effect the registration. If the registration is effected by any other person, that person shall recover the expenses of registration from the company

SESSION 4: REGISTRATION OF PARTICULARS OF CHARGEDelivery of particulars to the Registrar for registration Failure to register the particular by the company and the interested party shall result in a fine up to a prescribed amount payable by the company and every officer in default. Gower's report maintain that the primary duty to register is on the company, but the charge is the main sufferer if it fails to do so when registration is required under s. 107 of Act 179. Please let’s look at page 138.

SESSION 4: REGISTRATION OF PARTICULARS OF CHARGESatisfaction of discharge and enforcement of security Two other important matters that require registration are: • Satisfaction of discharge; and • Enforcement of security The purpose of these entries is to constitute actual notice about all relevant developments regarding charges on a company’s property (s.118).

SESSION 4: REGISTRATION OF PARTICULARS OF CHARGESatisfaction of discharge and enforcement of security Once the Registrar is satisfied based on evidence that the debt for which a charge was given has been paid or satisfied in whole or in part or part of the property charged has been released from the charge or has ceased to form part of the company’s property, the Registrar shall enter on the register of particulars of charge a memorandum of satisfaction in whole or in part or of the fact that the property has released of the charge. The Registrar shall furnish the company with a copy of the memorandum.

SESSION 5: CASE REVIEW Cohen v. Comet: GCB raises primarily the matter of priority between a bank as a debenture holder and an execution creditor.

SESSION 6: PUBLICATION IN THE GAZETTEPublication in the Gazette A publication in the Gazette constitutes constructive notice of the matter published. But a publication of a void event is notice of a void event. It should be noted that if a charge becomes void through non-registration it is ineffective even as regards creditors who had actual notice of it.

SESSION 6: PUBLICATION IN THE GAZETTEConsequences of Non-Registration THANK YOU