Investment Insights: Financial Opportunities and Risks Across Leading Indian Corporations

Explore strategic investment rationales across various sectors, including Shriram Transport Finance, IDFC, Federal Bank, ICICI Bank, Phoenix Mills, Bharat Electronics, and Hind Dorr Oliver. Each company presents unique opportunities in niche markets, high yield financing, and diverse revenue streams, alongside potential risks linked to macroeconomic conditions, asset quality, and market competition. Delve into insights that highlight growth prospects, financial strength, and the strategic positioning of these industry leaders against current economic challenges.

Investment Insights: Financial Opportunities and Risks Across Leading Indian Corporations

E N D

Presentation Transcript

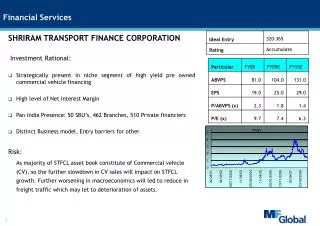

Financial Services SHRIRAM TRANSPORT FINANCE CORPORATION Investment Rational: • Strategically present in niche segment of high yield pre owned commercial vehicle financing • High level of Net Interest Margin • Pan India Presence: 50 SBU’s, 462 Branches, 510 Private financiers • Distinct Business model, Entry barriers for other Risk: As majority of STFCL asset book constitute of Commercial vehicle (CV), so the further slowdown in CV sales will impact on STFCL growth. Further worsening in macroeconomics will led to reduce in freight traffic which may let to deterioration of assets.

Financial Services IDFC Investment Rational: • Project Finance business – Huge demand potential despite near term concern • Assets management and investment banking – Strategy towards diversifying revenue streams and reducing capital intensity of business • Low Leverage & High ROE • Capital Adequacy Ratio • High Assets Quality Risk: As due to current down turn we expect that management cautious instance will impact the balance sheet growth & time deferment of carry profit which will keep some resistance on growth

Financial Services FEDERAL BANK Investment Rational: • Among sector one of the best cost efficient • Access to low cost NRI deposits • Well capitalized bank, with an CAR is among higher in industry • Venture into other business insurance, broking. Risk: As due to current down turn in we expect that quality of assets is a biggest concern. Large AFS book may let pressure on profit in term of MTM.

Financial Services ICICI BANK Investment Rational: • Huge Banking network & with an access to rural part of country supports growth going forward • Diversification in business like insurance, Brokerage, venture capital may phase problem in current scenario but ramp up will quickly with economic turnaround . • With softening in interest rate support to maintain margins & with restructuring relaxation delinquency may reduce Risk: As exposure to foreign assets & unsecured loan portfolio keeps pressure in current quarters. Loan Deferment in economic turnaround will keep much pressure on bank assets

REAL ESTATE PHEONIX MILLS LTD Investment Rational: • Current price is even discount to stress book value which just factor revenue from High street Phoenix Mills. • Proposed project are in Tier I & Tier II cities the area are still un penetrated. • Diversification of project like residential, hotels, retail & segregation of project gives viability of project. • Risk free balance sheet for project delay/deferment Risk: We expect that current slow down defers projects tenure, this we expect lead to delay in carry on equity investment made by pheonix in respective SPV’s

Bharat Electronics Investment Rational: • BEL company manufactures these products for all major defense establishments like Army, Navy, Air Force, Paramilitary forces, Indian Meteorological Department and others Space Technology Agencies. It commands a market share of approximately 57% against stiff competition from international companies. • It has an order backlog of Rs95.86bn that is 2.3x FY08 sales; Rs37.63bn orders would be executed in FY09. Another 25% revenues would come from run of the mill civilian orders.It has signed MOU with the defense ministry for achieving sales of Rs46.50bn implying a growth of 12% on yoy basis. • Strong Balance sheet, it is a debt free company with cash equivalents of approximately Rs 25.34bn (Rs316 per share). It has reserves of Rs31.53bn on small equity base of Rs800mn (Rs10 paid up) with Book value of Rs418per share. • It has enormous potential to capitalize from the offset clause in future as it is the only major player with the required expertise and technology collaborations in place with Lockheed Martin, Boeing, Raytheon,EADS, Northrop Grumman and Honeywell. • It is available at attractive valuations of 8.4x we look at the core business then it is available at 5x close to its historical low valuation. • Risk: It is dependent on foreign companies for the latest technology, which comes at exorbitant cost and constantly needs to upgrade its skills sets. In future the government plans to allow private sector to participate in the Defense Sector.

HIND Dorr Oliver Investment Rational: • With order book of Rs11.8bn and book to bill ratio of 3.6x it gives strong visibility for next 2-3yers. • Almost 65% of order book is from mineral beneficiation with clients like Vedanta and Uranium Corporation for their on-going projects, thus we do not foresee any risk to its core business. • Debt free company with cash on Books of Rs350mn, recurring other income of Rs32mn from lease rentals and every year cash generation of another Rs250-300mn. • With CAGR of more than 40% and good management pedigree the stock is available at attractive valuations of 3x. Risk: We expect significant slowdown in its manufacturing business which accounts for 15-20% of revenues. Due to turmoil in the economy we may see some pressure on the margins which may decline by 170bps to 9.5 in FY09 & FY10E.

PTC Investment Rational: • PTC has signed 26 contracts of 10.5GW under PPA, out of this PPA’s 6.9GW are under 25-30 year agreement, it has also entered into MOU for another 28.5GW. We expect that PTC would be trading 24% of the additional capacity planned under the 11th five-year plan. • It is also entering power tolling, it has plans to acquire coal mines of upto 10mt in Indonesia, it would supply the coal from these mines to IPP and after paying a fixed charge for production of electricity it would trade the power produced, this would be a high ROE business. • It has also taken stake in selective power projects the book value of these investments comes to Rs7.5per share, these assets in good market conditions may be valued at more than 2-3x the book value . • But the icing on the cake is that the company has a book value of Rs55per share and is a zero debt company also it has cash & cash equivalents worth Rs57.5per share. Risk: The slow down in the economy could increase the gestation period for the commissioning of the power projects. Many power projects have not been able to secure feedstock fuel and achieve financial closure. The power trading segment is highly regulated, under CERC guidelines for the short term access the company can charge only 4 paisa per unit traded.

Sintex Industries Investment Rational: • Diversification across products, geography and segment to help withstanding slowdown in any project, region or segment. • Strong orderbook of Rs15bn in monolithic business. • Strong outlook of prefab construction segment • Steady performance of textile division • Strong cash balance of Rs17bn to supports its expansion plan and withstand downturn. • Faster pace of integration of various acquired companies. • Access to key customers like Philips, Siemens, GE, Renault, General Motors etc though acquisitions of companies like, Wausaukee, Nief, Nero etc. • Strong customers relation help the company to increase cross selling across products and geographic. • Production outsourcing to India may improve consolidated margins in long term. Risk: • The company is witnessing slowdown across the board, particularly in overseas subsidiaries Wausaukee, Nero, Nief, and domestic subsidiary like Bright Brothers • Fluctuation in input cost and currencies may put pressure on margins.

Simplex Infrastructures Investment Rational: • Diversification across sectors like power, urban infra, transportation, piling, building, etc to help withstanding slowdown in any sector and geographic. • Strong orderbook of Rs102bn (2.1x FY09E sales) as on Dec’08. The company is L1 for Rs9.3bn and prequalified for projects worth Rs260bn. • Of total orderbook building contributed 18%, transportation 23%, Industrial 21%, piling 4%, power 19% and urban infra 15% respectively. • Lower dependence on subcontractor would help better control of execution and working capital. • No commitment to non construction business i.e. real estate and BOT projects • Majority of capex required for expansion has been achieved in FY08 and FY09, hence not much commitment for FY10 is required on capex front. • Strong project management skills • Ownership of modern equipments would help company to timely serve multi-location site and have edge over operational efficiency. Risk: • Higher exposure to private sector and Middle East should deteriorate orderbook quality. Of total orderbook exposure to real estate developer is 5% in India and 11% to Middle East. • We expect the company’s balance sheet to remain leveraged in near future with FY09E D/E ratio of 1.9x.

IVRCL Infrastructures and Projects Investment Rational: • Irrigation and water management sector has huge growth opportunities of ~Rs3trn in XI plan and IVRCL being the leader in the segment is well geared to tap the growth opportunity. • Strong orderbook of Rs143 bn (2.9x FY09E sales). The company is L1 for Rs17 bn, and has submitted bids for projects worth Rs50 bn. Strong Orderbook would help the company to grow by 35-40% CAGR in near future. • Balance Sheet comfort on debt side would help company to deliver such robust growth. • Of total order 98% of the order comes from Government, and since these projects are beneficially to the Government, chances of cancelation of these orders are minuscule. • Of total order book, 65%-70% is on account of water & irrigation, 20% on account of buildings, and balance 4-5% is on account of transportation and power each. • IVRCL has 4 BOT projects, 3 in roads sector and one water desalination projects. All these BOT projects would start contributing by Q1FY10E onwards, management expect these projects to contribute Rs14 mn per day on full utilization. • Subsidiary Hindustan Dorr Olivier, specialize in mineral beneficiation has strong order book of Rs11.8 bn and expected to report robust performance. Risk: • The company has advanced Rs2600 mn to IVR Prime with another Rs150mn as interest accrued. IVR Prime has to repay Rs800 mn in the current year itself and rest over period of time. IVR Prime has paid Rs250mn till date, considering the current situation of IVR Prime it looks little bit difficult to repay balance amount. • IVR Prime is required to pay another Rs3.75 bn to Noida Authorities for the development rights. It seems difficult for IVR Prime to pay this amount and may need support from the parent for this amount also.