Download

1 / 0

0 likes | 149 Vues

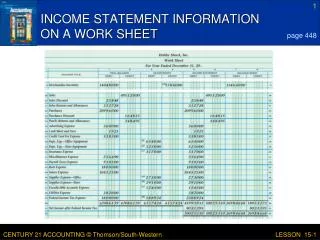

Income Statement and Balance Sheet Reformulatio n. Southwest and AirTran Acquisition. On May 2, 2011, Southwest acquired all of the outstanding equity of AirTran Holdings, Inc . whose parent company was AirTran Airways

E N D