Download

1 / 6

60 likes | 193 Vues

Explore strategies in resolution plans to mitigate risks in insurance and banking sectors, covering areas like liquidity, cooperation, and corporate governance. Understand rehabilitation and liquidation processes, emphasizing protection of policyholders. Learn about state laws, receivership, and successful closure strategies.

E N D

Winding-up and exit from the market Monica Lindeen Insurance Commissioner State of Montana

Resolution Plans & Banking Regulation in the US • Positive Aspects of Resolution Plans • Address the risk of discontinuing critical operations and services • Address the risk of derivative or counterparty actions • Address the risk of insufficient liquidity • Force Discuss on the risk that lack of cooperation could lead to ring-fencing of assets. • Bail In Concept in Banking • Banking Tied to the Real Economy • Insurance Should be Resolved Differently than Banking

Tools For Crisis Management • Access to Data • Risk Based Capital-Ladders of intervention • Hazardous Condition/Supervision-Risk based intervention • Stay provision • Runoff • Portfolio transfers • Reduce expenses including commissions by specified methods • Increase capital • Suspend dividends • Withdraw from • Correct corporate governance deficiencies

Resolutions Under State Law • Receivership governed by state law • Marshall the assets to provide continued coverage • Rapid resolution not appropriate for insurers • Ring fencing • Importance of laws to protect legal entity; despite push for group supervision • All policyholders in all jurisdictions must be treated the same

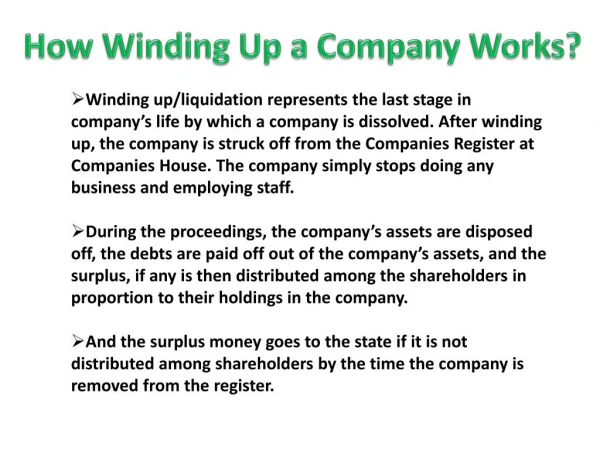

Rehabilitation & Liquidation • Rehabilitation • Used to implement sale, claims runoff, or trigger liquidation • Rehabilitation plan • Termination of rehabilitation • Liquidation • Policies are cancelled • Proofs of claim filed and processed • Distribution to creditors according to priority • Termination of qualified financial contracts • Closure of estate • State Guaranty Funds

Summary & Questions • NAIC currently Considering Resolution Plans On Certain Large Groups • Run on the Bank Covered By Broad Authority • Policyholder Benefits Protected As Opposed to Paid out In Cash • Protection of Monies Once Liquidated • Must Work Cooperatively in Resolving Companies in the same Group Together