Download

1 / 69

690 likes | 892 Vues

Full Economic Costs (fEC) of Research Projects . An Introduction Presented by:. Objective of Presentation. To introduce academics and administration managers to fEC as a basis for costing Research projects.

E N D

Full Economic Costs (fEC) of Research Projects An Introduction Presented by:

Objective of Presentation • To introduce academics and administration managers to fEC as a basis for costing Research projects. • To emphasize the support provided by Research Administration during and after project implementation. • To introduce a short summary of the costing requirement including changes to existing methodology.

Topics of Discussion • Background - where did fEC come from ? • Why is fEC important ? • How is fEC calculated ? • Budgeting academic time. • Admin. support & implementation timescale. • Research Council Costing Requirement.

Background - where did fEC come from ? (1) • Transparency Review (TRAC) introduced 1998 in response to JIF and SRIF1. • HEIs more transparent about how they spend between Teaching (T), Research (R) and Other Activities (O). • Figures reported to Funding Councils and consolidated for UK sector. • UK sector figures showed big losses in R. • Treasury accepted conclusions: SRIF2

Background - where did fEC come from ? (2) • R project costs on a fEC basis (from TRAC). • Government emphasised HEIs should recover fEC to ensure sustainability of R. • Extra £120M pa for current volume of Research Council (RC) projects from 2005/06. • RCs will fund 80% of fEC - balance from institution’s funds and /or dual support (RAE). • Govt.depts.should fund 100% of fEC. • Charities ? • Lots of info at: http//www.jcpsg.ac.uk

Why is fEC important? • Sustainability • “ An institution is being managed on a sustainable basis if, taking one year with another, it is recovering its full economic costs across its activities as a whole, and is investing in its infrastructure (physical, human, and intellectual) at a rate adequate to maintain its future productive capacity appropriate to the needs of its strategic plan and students, sponsors and other customer requirements.” (Definition in TRAC Volume III) • Issues - fEC, strategic, pricing, project management/cost recovery, investment

A Point to Remember ! • fEC is the methodology used to cost projects to ensure sustainability etc of Research. • Research proposals contain a PRICE for the Research which may be different to the cost.

Current Costing Method RA costs Technician costs Non-staff direct costs O/H recovery (if applic.) eg.46% for RCs fEC RA costs Technician costs Non-staff direct costs Estates costs as direct Indirect costs PI costs Replacement cost of departmental equipment Estates now includes Infrastructure costs, Indirect costs now include COCE, both previously not included in College costs. How is fEC calculated ? (1)

How is FEC calculated ? (2) • Estates costs as direct: - RCs will fund. Other sponsors may follow. - Charge on basis of £X / acad.staff member (FTE) • Indirect costs: - Charge on basis of £X / acad.staff member (FTE) • PI costs: - PIs to estimate time spent on projects (actual hrs) - Apply cost according to grade of staff. Research Councils will fund 80% of all of this on ESTIMATE. No need to record actual time by project for RCs. Sponsored PGRs and equipment costs over £50,000 are exceptions to the rule.

Budgeting academic time (PI costs) (1) • Time should be estimated in actual hours. • Include time for project mgmt., writing papers, dissemination, etc. • Exclude PGR training/supervision unless it is a studentship included in the sponsor’s project. • PIs to keep simple records to verify time eg.notes/log book of events, meetings, etc.

Budgeting academic time (2) • No prescribed methods for estimating time . • Could base on hours required each month over project life; or on standard proxy e.g. [2 hours] a week per RA plus [2 hours] a week per project (more if more complex project) • Research Councils will be comparing estimates • Overall reconciliation (at institutional level) of estimated time with actual time spent (from annual TRAC time allocation schedule data)

Administration Support • Usual one to one support provided by Research Admin through application process. • All costing done within RACE 2 by authorized staff. • Database of estimated PI time on awarded projects will be kept to verify commitment of time. • RA contacts: • Unresolved Issues:

Implementation Timetable (1) • January 2005: fEC rates calculated • XXXXX: Institutional systems for fEC established. • XXXXX: Training on new processes provided. Costing/managing projects on fEC basis begins.

Implementation Timetable (2) • July 2005: Release of RC forms Training on new forms provided • September 2005: All RC applications made (and funded) on fEC basis. Projects will start April-Dec.2006.

Summary • Introduction to costing R projects on FEC basis. • Involvement of academics (budgeting time). • Central support from RAdmin.

Conclusion • Potential increase in net R income from RCs (pa) c.£XX for (Institution name) in 2010. • Opportunity to improve cost recovery from other funders. • Improved resource will directly benefit R active academics.

ANY QUESTIONS ? Open Discussion !

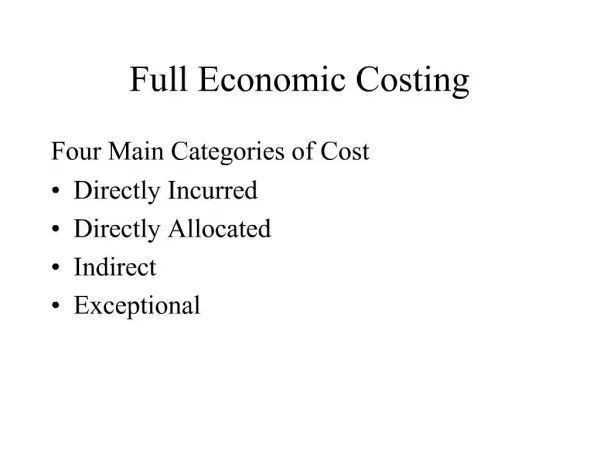

fEC Costing - a Under fEC there is a subtle reclassification of certain categories of cost. “Direct” costs remain. Indirect costs are analysed and identified as either “Directly Allocated” or “Indirect” costs.

fEC Costing - b DirectCosts • Research Staff Salaries Researchers Technicians (inc animal techs) Other Direct administration Computing/computing support staff Casual staff etc • Travel & Subsistence • Consumables • Equipment • Large Capital

fEC Costing - c Directly Allocated charges • Principal Investigator • Other Academic staff • Other staff subject to Time Allocation excluded from “Indirect Cost” calculation • Replacement Cost of Departmental Equipment • Estates/Premises Costs ( as £/FTE Academic Staff & PGR’s)

fEC Costing - d Indirect costs • Indirect costs (as £/FTE Academic Staff & PGR’s)

fEC Costing - e Under fEC the main changes relate to an analysis of “Overhead” charges. This identifies - • PI and Associates time. • Equipment. • Estates/Premises Costs. • Indirect Costs (All other overheads)

fEC Costing - f New costs are introduced. - “Infrastructure” and “Cost of Capital Employed”. • Infrastructure cost is added to Estates/Premises cost to reflect the full long-term maintenance of College Infrastructure. • Cost of Capital Employed is added to Indirect costs to reflect the legitimate costs of running and financing the business.

fEC Costing – g.1 PI and Associates Time - 1 • All Academic time to be identified and costed. (Includes Research Fellows). • Expressed as hours/day/week/year (not %). • £ per hour based on national fEC standard hours of 1650 pa (220 days @ 7.5 hrs per day).

fEC Costing – g.2 PI and Associates Time - 2 • Includes ALL estimated time dedicated to project. • Time spent training/supervising PGR students to be separately identified. • These costs are charged to Directly Allocated Charges

fEC Costing - h Other Staff • Non-academic staff subject to time allocation (principally Pool Technicians) will be charged to Directly Allocated Charges and their costs excluded from the Indirect Cost calculation in TRAC

fEC Costing - i Equipment - New • All new equipment purchased for the project to be charged as Direct Cost.

fEC Costing - j Equipment – Departmental etc. • Replacement cost charged to Directly Allocated Charges. • Formulated cost based on use/depreciation.

fEC Costing - k Estates/Premises Cost • TRAC produces a £/FTE cost. • Based on total annual E/P cost adjusted for estimated use of existing equipment. • Relates to Academic R staff and PGR student FTE. • Nationally imposed and locally derived weighting. [Academic staff @ 1.0x fte, PGR Lab based @ 0.8x fte, PGR other based @ 0.5x fte] • These costs are charged to Directly Allocated Charges.

fEC Costing - l Indirect Costs • TRAC produces a £/FTE cost. • Relates to Academic R staff and PGR student FTE. • Nationally imposed weightings. [Academic staff @ 1.0x fte, PGR @ 0.2x fte] • Calculated from all central costs. (College + school + department).

fEC Costing - m Infrastructure Costs • Part of the TRAC basic calculation, additional to statutory accounts figures. NOT identified separately for fEC.

ANY QUESTIONS ? Open Discussion !

Simple Case Study Group Work 45 Minutes for Consideration

CASE STUDY – 0.1 Question: • Calculate the fEC of the project based on the specific data. • Show the split of costs as follows: • Directly Incurred costs, • Directly Allocated costs, • Indirect costs..

Simple Case Study Model Answer

CASE STUDY – 1.0 Note 1: PI– to Directly Allocated • Annual cost = 750/5 x £60,000/1650 • Annual PGR student support = 215 x £60,000/1650

CASE STUDY – 1.1 Note 2: Co-Investigatorto Directly Allocated • Annual cost = 200 x £40,000/1650 year 1 • Annual cost = 200 x £41,000/1650 year 2 • Annual cost = 200 x £42,000/1650 year 3 • Annual cost = 200 x £43,000/1650 year 4 • Annual cost = 200 x £44,000/1650 year 5

CASE STUDY – 1.2 Note 3: Research Assistant – to Direct • Annual cost = 1650 x £25,000/1650 year 1 • Annual cost = 1650 x £26,000/1650 year 2 • Note: Years 1 + 2 only

CASE STUDY – 1.3 Note 4: Research Assistant – to Direct • Annual cost = 1650 x £30,000/1650

CASE STUDY – 1.4 Note 5: 2 x Technicians – to Direct • (1) £20,000 each year (1 – 5) • (2) £15,000 year 1 • (2) £15,500 year 2 • (2) £16,000 year 3 • (2) £16,500 year 4 • (2) £16,500 year 5

CASE STUDY – 1.5 Note 6: Dedicated Clerical post – to Direct • £20,000 year 1 • £20,500 year 2 • £21,000 year 3 • £21,500 year 4 • £22,000 year 5

CASE STUDY – 1.6 Note 7: Travel – to Direct • Annual cost = £10,000

CASE STUDY – 1.7 Note 8: Consumables – to Direct • Annual cost = £20,000

CASE STUDY – 1.8a Note 9: Equipment – to Direct • £51,000 charged at start of project • £150,000 charged at start of project