Understanding Systemic Risk

Explore the complex world of systemic risk, focusing on Lehman Brothers' downfall and its repercussions on the global financial system. Delve into the concepts of fire sales, contagion risks, hysteresis, and black swan events to comprehend the fragility of interconnected markets. Gain insights into modeling systemic risks and monitoring tools needed to navigate today's complex financial landscape.

Understanding Systemic Risk

E N D

Presentation Transcript

Understanding Systemic Risk The National Institute of Finance

Lehman Brothers Failure Did they know what was going on? Did they have a choice?

Lehman Brothers Failure Exposed to Lehman Brothers – Owned $785M Lehman bonds ‘Broke the Buck’ Share price cut to 97¢ $2 Trillion Market

Lehman Brothers Failure Exposed to Lehman Brothers – Owned $785M Lehman bonds ‘Broke the Buck’ Share price cut to 97¢ $2 Trillion Market

“If this crisis has taught us anything, it has taught us that risk to our system can come from almost any quarter. We must be able to look in every corner and across the horizon for dangers and our system was not able to do that.” Secretary Geithner, opening remarks, testimony to Senate Banking Committee, June 18, 2009.

What is Systemic Risk? New equilibrium below full production Disruption of access to credit Punishing the system, not the firm

Domino Risk $3T CDS Notional outstanding

Domino Risk $3T CDS Notional outstanding AIG goes down, who else goes? $185b Gov. Loans

Fire Sale Risk Portfolio insurance, trading strategy – Mimic put option, sell stock in decline

Fire Sale Risk Rating Agency Arbitrage + Mortgage market decline = Toxic Assets

Model of Systemic Risk Stressed firms sell assets (adjust balance sheet) Contagion I - Market (Liquidity) failure, firms sell new assets and stress new markets Contagion II - Market panic and there are runs on markets Hysteresis - Long term freezing of markets

Contagion Risk I What is the correlation?

Contagion Risk I $10.80 $21.62 • Hunt Brothers ‘cornered’ Silver market • 1980 controlled 1/3 of world silver • Family fortune of $5b • Margin requirements were changed • Price dropped 50% on March 27, 1980

Contagion Risk I • Hunt Brothers ‘cornered’ Silver market • What else did the Hunt Brother’s own? • Fire sale in silver • Liquidity dried up • Fire sale in cattle • Correlations driven by?

Contagion Risk I • The Russian Financial Crisis • 1998 Long Term Capital Management • Small exposure to Russian debt • Large leveraged exposure to Danish debt

Contagion Risk I • The Russian Financial Crisis • 1998 Long Term Capital Management • Russia defaulted 1998 • Holders of Danish debt hit by default • Fire sale in Danish debt • LTCM connected to everyone

Contagion Risk I • The Credit Crisis • Citibank’s exposure to CP Market?

Contagion Risk I • The Credit Crisis • Citibank’s exposure to CP Market? • Off balance sheet, obligation to provide short term financing to SIVs Citi had invented and formed.

Contagion Risk I • The Credit Crisis • Citibank’s exposure to MBS Market? • SIVs bankruptcy remote – have to sell when in trouble and what did they own – MBS ‘Toxic Assets’

Contagion Risk II Confidence in the market is gone, no-one knows who is solvent

Contagion Risk II Flight to quality (US Treasury), credit markets freeze

Hysteresis How long can companies ‘hold their breath’?

Hysteresis Experiment Repeat Experiment The Economy is ‘path dependent’

Probability of a Black Swan • Predicting Fire Sales • Leverage of System • Liquidity Capacity • Velocity, depth of trading • Capacity for bargain hunting • Linkages – Book Correlation

Black Swan Losses • Loss Distribution • Tail events are rare – very little data • Typically strong model assumptions

Black Swan Losses We are not in Kansas anymore • Loss Distribution • Tail events are rare – very little data • Typically strong model assumptions • Liquidity Failures • Can’t hedge • No replicating portfolios • Mean & Variance • Game Theory

Black Swan Losses • Loss Distribution • Tail events are rare – very little data • Typically strong model assumptions • Liquidity Failures • Scenario Analysis • Linkages – rights, obligations (Not Netting!) • Granular Macro Economics • Understanding Domino Risk

Black Swan Losses • Loss Distribution • Tail events are rare – very little data • Typically strong model assumptions • Liquidity Failures • Scenario Analysis • Economic Impact • CaR – Credit at Risk • DoL – Distribution of Loss

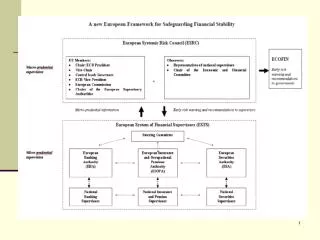

Monitoring Systemic Risk • Monitoring health of Economy • Regime shifting models • Summaries reflecting stress • Historical data • Derivatives data • Looking for Black Swans • Leverage measures • Concentrations, Bubbles • Liquidity capacity • Linkages and Transparency

Current Risk Systems • Not predicting cascading failures • Determine loss by counterparty • Do not predict probability of failure of counterparties • Do not account for Linkages

Data and Analytics Legal authorities must be strengthened Regulators must understand the network Regulators must understand aggregation Regulators are ‘outgunned’

(Partial) Solutions • Exchanges and Clearing Houses • Increase Liquidity • Concentrate Risk • System views with existing resources • Historical Data • Market Data • Firm Risk Systems

Solution:Increase Transparency • Data Transparency • Reference Data – • Legal entities • Product descriptions (Prospectus, Cash-flows, …) • Details that ‘fit into’ a model • Transactions/Price Data – • Exchange, Clearing House, OTC (like TRACE) • Position (Trading Book) data • Essential for calibrating models

Solution:Increase Transparency • Model Transparency • Price a complex OTC (How many can price?)

Solution:Increase Transparency • Model Transparency • Getting a 2nd opinion

Solution:Increase Transparency • Model Transparency • Getting a 2nd opinion • Building an active research community • Banks are not doing long-term research • Regulators have limited efforts • Academics have hard time getting data and funding

Solution:Increase Transparency • Model Transparency • Getting a 2nd opinion • Building an active research community • Current research efforts are incomplete • Models under stress/Transition to new equilibrium • Are markets complete (hedge-able)? • National Weather Service equivalent? • Competitive modeling environment (multiple Hurricane models).

Solution:The National Institute of Finance Proposed by concerned citizens Part of regulatory reform legislation Collect system-wide transaction data Develop analytic tools

Solution:The National Institute of Finance Part of the Federal Government Protect data at highest level of security Metrics to monitor risk – early warning NTBS – post-mortum investigations

The National Institute of Finance Internal Systems (All Obligation) -Reference Data -Reporting Language Prototypes -Reference Data -Systemic Model (MBS) Hedge Fund Risks -Hedge Fund Counter-party network -Hedge Fund wide risk assessment Is it feasible? Market participants are close

The National Institute of Finance www.ce-nif.org