Re-Pricing Underwater Stock Options

20 likes | 153 Vues

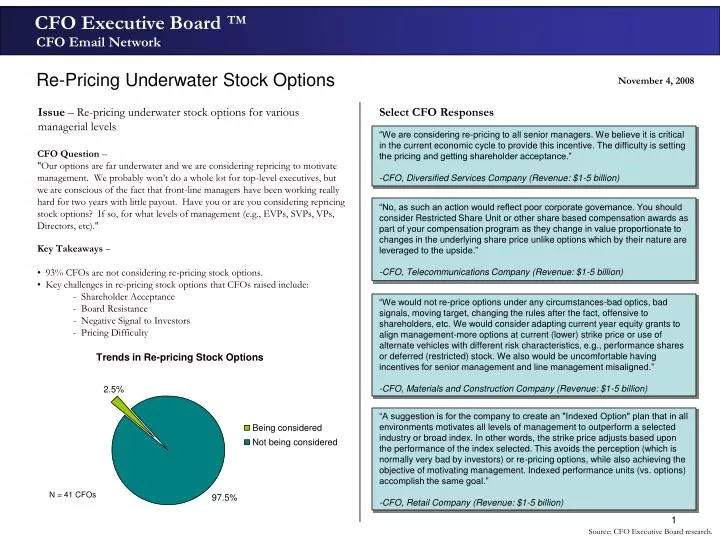

A significant 93% of CFOs are not considering re-pricing underwater stock options, reflecting concerns around governance, investor signals, and the complexities of pricing. Some CFOs advocate for alternative compensation methods to align management incentives without the drawbacks of re-pricing. Various strategies, including indexed options and performance shares, are suggested to motivate management effectively. This article reviews CFO insights on the challenges of re-pricing in the current economic climate and highlights the considerations for different managerial levels.

Re-Pricing Underwater Stock Options

E N D

Presentation Transcript

Trends in Re-pricing Stock Options 2.5% Being considered Not being considered 97.5% Re-Pricing Underwater Stock Options November 4, 2008 Issue – Re-pricing underwater stock options for various managerial levels Select CFO Responses “We are considering re-pricing to all senior managers. We believe it is critical in the current economic cycle to provide this incentive. The difficulty is setting the pricing and getting shareholder acceptance.” -CFO, Diversified Services Company (Revenue: $1-5 billion) CFO Question – "Our options are far underwater and we are considering repricing to motivate management. We probably won’t do a whole lot for top-level executives, but we are conscious of the fact that front-line managers have been working really hard for two years with little payout. Have you or are you considering repricing stock options? If so, for what levels of management (e.g., EVPs, SVPs, VPs, Directors, etc)." “No, as such an action would reflect poor corporate governance. You should consider Restricted Share Unit or other share based compensation awards as part of your compensation program as they change in value proportionate to changes in the underlying share price unlike options which by their nature are leveraged to the upside.” -CFO, Telecommunications Company (Revenue: $1-5 billion) • Key Takeaways – • 93% CFOs are not considering re-pricing stock options. • Key challenges in re-pricing stock options that CFOs raised include: • - Shareholder Acceptance • - Board Resistance • - Negative Signal to Investors • - Pricing Difficulty “We would not re-price options under any circumstances-bad optics, bad signals, moving target, changing the rules after the fact, offensive to shareholders, etc. We would consider adapting current year equity grants to align management-more options at current (lower) strike price or use of alternate vehicles with different risk characteristics, e.g., performance shares or deferred (restricted) stock. We also would be uncomfortable having incentives for senior management and line management misaligned.” -CFO, Materials and Construction Company (Revenue: $1-5 billion) “A suggestion is for the company to create an "Indexed Option" plan that in all environments motivates all levels of management to outperform a selected industry or broad index. In other words, the strike price adjusts based upon the performance of the index selected. This avoids the perception (which is normally very bad by investors) or re-pricing options, while also achieving the objective of motivating management. Indexed performance units (vs. options) accomplish the same goal.” -CFO, Retail Company (Revenue: $1-5 billion) N = 41 CFOs Source: CFO Executive Board research.