Download

1 / 27

270 likes | 290 Vues

This document provides an overview of the budget process, including the role of the National Treasury, assessment criteria for budget submissions, and key milestones. It emphasizes the importance of allocating resources to political priorities and using the budget as a tool for improving the effectiveness of spending.

E N D

The Budget Process, Documents and the Appropriation Bill NATIONAL TREASURY Dr Kay Brown : Expenditure Planning 22 February 2011

Overview • The budget is a key statement of the policy of the government. It is a process through which choices have to be made about competing priorities • The budget must fulfil 3 functions: • Spending, taxation and borrowing must support economic objectives • Resources must be allocated to political priorities • Budget and budget information must be tools to improve quality and effectiveness of spending for service delivery

How the MTEF works • Since 1997, Government runs a rolling 3 year budget process • Lets assume the police budget published in 2010 is as follows • R100 in 2010/11, R105 in 2011/12 and R110 in 2012/13 • For the 2011 budget, the R105 and the R110 are the budget baseline figures for police • To get the new third year, we increase the R110 by 6% for example, lets call it R116 in 2013/14 • Now we have a MTEF baseline of R105 in 2011/12, R110 in 2012/13 and R116 in 2013/14 • MTEF budget baselines are then thoroughly examined to identify possible savings and areas which require additional funding

Government priorities • The medium term strategic framework (MTSF) is a statement of government’s chosen priorities. It is adopted by Cabinet every five years and then updated annually • Within the Fiscal Framework - the Budget transfers resources in line with priorities • Outcomes Approach: • sets out 12 clear measurable outcomes which are to lead the attainment of government’s priorities • and thus form the focus of government policy and service delivery implementation and targeting • Government has prioritised its efforts and resources more rigorously to support particularly following government outcomes, namely: • Job creation specifically focused on youth employment • Education and skills development • Health • Integrated and sustainable human settlements • Vibrant, equitable and sustainable rural communities

National Treasury’s technical role • Provide the overall Division of Revenue proposal between the 3 spheres based on the decisions made at a political level on priorities and on further analyses • Provide the technical guidelines for budget submissions • Conduct the evaluation of those budget submissions • Maintain ongoing communication with other government departments and agencies throughout the budget process • Make recommendations on the budget that should be proposed

Criteria for assessment of budget submissions • The following factors are considered when assessing budget submissions: • link of budget submission proposal to broad government priorities • research on policy options for delivering • funding in previous MTEF periods • evidence of underspending and/or unwise spending • proper plans and proper costing • appropriately aligned implementation and spending plans • appropriate monitoring and evaluation • execution according to budget planning, seen in strategic planning documents, etc

Role players in the budget process • The MTEC is an interdepartmental committee - comprising of representatives from NT, DPSA, Planning Commission, DPME and DCog • MTEC considers the allocation of funds in respect of each grouping of departments, in line with the outcomes approach (previously individual departments were not grouped by government function for budgeting) • Departments • Intergovernmental technical forums • Relevant entities and donors • Ministers’ Committee on the Budget • Budget Council (Minister and provincial MECs for Finance) • Budget Forum (Budget Council plus local government) • Cabinet • Financial and Fiscal Commission • Legislatures • Portfolio Committees, Finance Committees, Appropriations Committees

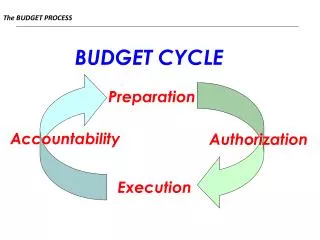

Key milestones Policy review Departmental planning Parliament & budgeting Departments prepare budget, including detailed spending plans for new proposals April June July Aug Sept Oct Division of Revenue Act passed Review, evaluate and decide on new major policy proposals Intergovernmental and technical forums Appropriation Bill and Revenue Bills passed Propose fiscal and budget framework, and division of resources Executive/s consider frameworks and division of resources Sector and focused budget hearings Table Medium Term Budget Policy Statement

Key milestones Policy review Departmental planning Parliament & budgeting Portfolio committees submit BRRR reports, adopt fiscal framework, pass Money Bills Nov Dec Jan Feb March Cabinet approves new MTEF allocations Departments revise medium term plans and finalise budget inputs Departments revise medium term plans and finalise budget inputs National Budget tabled (includes response to BRRR) Strategic Plans tabled Provincial budgets are tabled (14 days after National budget is tabled) Adoption of fiscal framework

Budget documents • Parliament’s recommendations are considered and allocation letters are sent in November/December, including the earmarking of certain amounts or stated conditions • Budget documents are then prepared: • Budget Speech • Budget Review • Peoples’ Guide • Appropriation Bill • Estimates of National Expenditure • Division of Revenue Bill

Estimates of National Expenditure layout • Introduction • Summary of additional allocations to departments • Summary tables • Main budget framework • Additional allocations to national votes • Expenditure by national vote • Expenditure by economic classification • Amounts to be appropriated to national votes for 2011/12 by economic classification • Conditional grants to provinces and municipalities by national vote • Training expenditure per vote • Infrastructure spending per vote • Personnel expenditure per vote • Departmental receipts per vote • Guide to information contained in each chapter

ENE layout • One chapter per vote • 38 votes with selected public entities and other agencies • Votes arranged according to functional groupings • Functional groupings: • Central government administration • Financial and administrative services • Social services • Justice, crime prevention and security services • Economic services and infrastructure • More detailed information for each vote available on www.treasury.gov.za. More comprehensive coverage of vote specific information, particularly goods and services, transfers, donor funding, public entities and lower level institutional information

Information contained in each chapter • Budget summary

Information contained in each chapter • Expenditure allocation for 2011/12 (corresponds with 2011 Appropriation Bill information) • Appropriation: the approval by Parliament of spending from the National Revenue Fund, or by provincial legislature from a Provincial Revenue Fund • Totals disaggregated into current payments, transfers and subsidies, payments for capital assets and payments for financial assets • Current payments are payments made by a department for its operational requirements • Transfers and subsidies are payments made by a department for which the department does not directly receive anything in return • Payments for capital assets are payments made a department for an asset that can be used for more than one year and from which future economic benefits or service potential are expected to flow. • Payments for financial assets mainly consist of payments made by departments as loans to public corporations or as equity investments in public corporations. The reason for expensing the payments rather than treating them as financing is that, unlike other financial transactions, the purpose of the transaction is not profit oriented. This column is only shown in votes where such payments have been budgeted for. Payments for theft and losses are included in this category; however these payments are not budgeted for and will thus only appear in the historical information, which can be seen in the expenditure estimates table. • Estimates for 2012/13 and 2013/14

Information contained in each chapter • Aim – department’s strategic objectives • Programme purposes • Strategic overview: 2007/08 – 2013/14 • Policy and mandate developments and legislative changes • Department’s contribution to the achievement of outcomes attributed to it and related outputs listed in Service Delivery Agreements • Savings and cost effectiveness measures– details of reprioritisation of budgets effected and savings and cost reduction measures

Information contained in each chapter • Table of selected performance indicators • Indicators are numerical measures that track a department’s or entity’s progress towards its goal • Programme column links indicator to the programme associated with it

Information contained in each chapter • Expenditure estimates

Information contained in each chapter • Expenditure trends • Main expenditure trends and vote programme structure changes from 2007/08 financial year to 2013/14 financial year described • Spending focus over the MTEF period • Nominal annual growth rates calculated for the full or MTEF period • Real annual growth rates – growth rate deflated by CPI - calculated in certain instances • Summary of new (additional) allocations to the baseline budget • Personnel information • Summary of personnel posts per programme by salary level • Infrastructure spending • Expenditure on existing, new and mega infrastructure

Information contained in each chapter • Departmental receipts • Departmental receipts for MTEF period described in relation to receipts for 2010/11

Information contained in each chapter • Detailed discussion by programme • Programme objectives and measures • Objectives and measures shown for each programme (except programme 1: Administration) • Example: Improve the provision of services and products to eligible citizens and residents (strategic intent/objective) by reducing the time taken to issue passports and travel documents (specific intervention) from 10 days in 2010/11 to 5 days in 2013/14 (progress measure) • Purposes and activities of subprogrammes in respect of the programme • Expenditure estimates per programme table • Expenditure trends per programme

Information contained in each chapter • Public entities and other agencies • Additional tables • Summary of expenditure trends and estimates per programme and economic classification (2 years) • Details of approved establishment and personnel numbers per salary level • Summary of expenditure on training (by category) • Summary of departmental public private partnerships projects • Summary of expenditure on infrastructure (by type) • Tables available on www.treasury.gov.za • Summary of conditional grant payments • Departmental specific tables • Summary of donor funding (including spending focus)

The Appropriation Bill • Bill provides for the appropriation of money from the National Revenue Fund in terms of section 213 of the Constitution and section 26 of the PFMA • Bill sets out allocations by Vote and main division within votes • An aim is set out for each vote and a purpose is set out for each programme • Headings group some listed items • Allocations marked with an * refer to specifically and exclusively appropriated amounts • Conditional grants are specifically and exclusively appropriated and are also listed in the Division of Revenue Bill • Spending is subject to the PFMA and provisions of the Appropriation Bill • Section 29 of the PFMA applies, until Appropriation Act signed • Key tool for oversight and management