Download

1 / 19

900 likes | 4.06k Vues

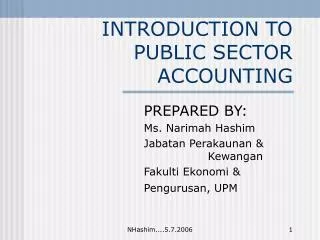

Introduction to Public Sector Accounting. What is Public Sector?. Types of Organizations. Organizations. Private sector. Public sector. Non-profit. Profit. Profit. Non-profit. Enterprises (GLCs). Corporations. Foundations, Charities, religious inst. Schools, Hospitals, Army.

E N D

Introduction to Public Sector Accounting SAS/2005

Types of Organizations Organizations Private sector Public sector Non-profit Profit Profit Non-profit Enterprises (GLCs) Corporations Foundations, Charities, religious inst. Schools, Hospitals, Army

WHAT IS PUBLIC SECTOR? • “Those industries and services in a country that are owned and run by the state, such as (by many countries) the education services and the railways …” Longman Dictionary of Contemporary English • “a device for regulating human activities so that man and women can live together in reasonable harmony… Derbyshire (1987) • “any entities, established and owned by central, state or local government and any entity established under any Act of Parliament, which requires the presentation of the annual financial statement to the Parliament…” MACPA Guideline No. 1 1990

Forms of Government • Absolute monarchy One person rule • Aristocracy wealthy minority rule • Democracy based on a belief in the value of the individual eg choice of selecting representatives Make criticism? Rights being protected? Taking part in politics? Public interest is a priority?

Terms related to government • Power The ability to get things done • Authority The right to get things done (formal evidence to power) • Nation A group of people, often from a different backgrounds or races, live together and adopt a common identity • State the whole apparatus of government that a a nation sets up

Terms related to government • Nation state A government formed by a group of people, often from a different backgrounds or races, adopt a common identity and live together peacefully (as opposed to artificial state) • Constitutional state A government with a written system (constitution), which incorporate a bills of rights guaranteeing individual freedoms • Constitution Basic law of a state that sets out the system of a government

Features of Public Sector • No individual shares of ownership • Operate within a framework of public authorization and control • Plurality of objectives • No direct financial interest or benefits to the contributors of resources • Varying accounting principles and practices • Political rather than financial control

Objectives of Public Sector • To preserve law and order with minimum interference in social affair; • Regulating aspects of industry and economy; • The provision of services and public goods to the society or the people; • Defence, security, law, health, education, transportation, international diplomacy etc. • Various agencies, government departments and public enterprises were set up to realise the provision of the services and public goods • Public administration, defence, internal security and laws

COMPONENTS OF PUBLIC SECTOR • Ministries • Departments • Public Enterprises FEDERAL GOVERNMENT STATE GOVERNMENT • Departments • Public Enterprises • City Council • Municipal Council • District Council LOCAL GOVERNMENT

WHAT IS PUBLIC SECTOR ACCOUNTING? • a process of identifying, measuring, recording and communicating public sector economic information to permit informed judgment and decisions by the users . • Process of studying the accounting practices of public sector organizations in ensuring accountability in providing services to the public at large.

Objectives of PSA • Providing information useful for making economic, political and social decisions, and demonstrating accountability and stewardship; • Providing information useful for evaluating managerial and organizational performance. (National Council on Governmental Accounting (NCGA), p.126)

Roles of Accounting PSO • To execute the function of stewardship over public resources • Stewardship – to demonstrate the enstrusted assets have not been appropriate • To discharge public accountability over all kind of public resources • Accountability – responsibility for your actions to someone else (to include the performance of the assets) • To establish an appropriate accounting system for the purpose of accounting public monies and assets

Users of PSA Information • Taxpayers • Grantors • Investors • Fee-paying service recipients • Employers • Vendors (suppliers) • Legislative bodies • Management • Voters • Oversight bodies

PSA Policy-Making • International Level • Several international standard setters • 1977 – International Federation of Accountants (IFAC) • It works with its 158 member organizations in 118 countries • 1998 – The Public Sector Committee was set up to deal with issues of public sector organizations • International Organisation of Supreme Audit Institutions – reports on issues of the development of international accounting standards for governments

The Public Sector Committee of IFAC • Objective: • to develop programs aimed at improving public sector financial management and accountability, including developing accounting standards and promoting their acceptance • Authorized to issue International Public Sector Accounting Standards (IPSASs) • IPSASs adapt IASs (by IASC) wherever possible unless there a certain public sector issue that warrants a departure • Website : http://ifac.org/PublicSector/ • Due Process: • Exposure Drafts to the relevant parties (4 months) • Issuance of IPSAS upon approval by PSC

IPSASs • Scope of the standards: • applicable to all public sector entities including national governments, local governments and their component governments • Not applicable to Government Business entities • At present, 20 IPSASs have been issued by PSC (IPSAS 1 to IPSAS 20)

IPSASs • IPSAS 1 - Presentation of Financial StatementsIPSAS 2 - Cash Flow StatementsIPSAS 3 - Net Surplus or Deficit for the Period, Fundamental Errors and Changes in Accounting PoliciesIPSAS 4 - The Effects of Changes in Foreign Exchange RatesIPSAS 5 - Borrowing CostsIPSAS 6 - Consolidated Financial Statements and Accounting for Controlled EntitiesIPSAS 7 - Accounting for Investments in AssociatesIPSAS 8 - Financial Reporting of Interests in Joint Ventures

IPSASs • IPSAS 9 - Revenue from Exchange Transactions • IPSAS 10 - Financial Reporting in Hyperinflationary Economies • IPSAS 11 - Construction Contracts • IPSAS 12 - Inventories • IPSAS 13 - Leases • IPSAS 14 - Events After the Reporting Date • IPSAS 15 - Financial Instruments: Disclosure and Presentation • IPSAS 16 - Investment Property • IPSAS 17 - Property, Plant and Equipment • IPSAS 18, Segment Reporting • Glossary of Defined Terms, IPSASs 1-18 • IPSAS 19 - Provisions, Contingent Liabilities and Contingent Assets • IPSAS 20 - Related Party Disclosures