Download

1 / 13

130 likes | 312 Vues

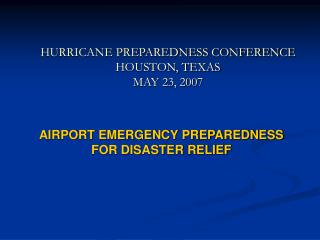

American Geological Institute Academic - Industry Associates Conference Houston, Texas 1999. Petroleum Sector Remarks Dodd DeCamp. Recent Oil Price Cycles Monthly 1987 - 98. 40. Persian Gulf War . 35. Asia Boom 2 Cold Winters Iraq Out Stocks Very Low. 30. Iran-Iraq Quota Battle

E N D

American Geological InstituteAcademic - Industry Associates ConferenceHouston, Texas1999 Petroleum Sector Remarks Dodd DeCamp

Recent Oil Price CyclesMonthly 1987 - 98 40 Persian Gulf War 35 Asia Boom 2 Cold Winters Iraq Out Stocks Very Low 30 Iran-Iraq Quota Battle Following War $/Barrel Nominal 25 20 Asia Crisis 2 Warm Winters Big Stock Build 15 Metallgesellschaft Contracts Sell-off 10 Jan 87 Jan 88 Jan 89 Jan 90 Jan 91 Jan 92 Jan 93 Jan 94 Jan 95 Jan 96 Jan 97 Jan 98

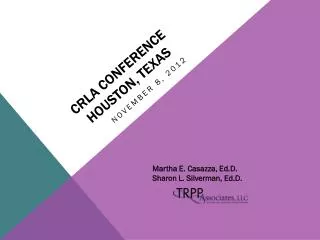

45 2000 1800 1600 Non-OPEC Oil Prodoction 40 Non-OPEC Rigs 1400 Production Rigs 1200 35 1000 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 Non-OPEC Supply Response All-Time Low Baker Hughes

Cause Short-term Drivers Effect Petroleum Industry Cycles Reduced New Opportunity Set Lower Quality Opportunity Sets (Long Term) Increased Economic Hurdles (Risk) in Industry Portfolios Emphasis on Near-Term Production Deterioration in Upstream Margins Bottom of Cycle Cost Structures Lower Service Sector Rates Reduced Availability of Investment Capital Ultimate Decline in Production Capacity Lower Activity Levels Modified from A.D. Little

Through-Cycle Strategic Management is Critical Petroleum Commodity Cycle - Asymmetric Tendency “Through-Cycle Strategic Management Reactive Near-term Focus E&P “Opportunity Capture” Below Critical Mass = Crash & Burn Time 3-5 Years

Portfolio Objectives Are Impacted Prioritize Focus Resources Performance Exposure to maximum potential value additions and ability to access emerging phase Maximum rate of value addition Smaller value increments with high investment efficiency Cumulative Value Idea Probe Focus Core Harvest / Exit Effectiveness Efficiency

Gas Deepwater Conventional Oil Petroleum Industry Upstream Focus NW Europe Atlantic Margin Alaska N. Slope FSU Caspian Sea Gulf of Mexico N. Africa Middle East Asia Gas/LNG N. Latin America W. Africa Brazil

Worldwide Exploration Finding Cost (3-Year Moving Average) $/boe $/boe Focus on the proven petroleum basins and systematic use of technology are narrowing the field Industry Average* Worst Performers Best Performers ** Notes: * Average (unweighted) for following peer companies: Amoco, ARCO, BP, Chevron, Elf, Exxon, Mobil, Phillips, Shell, Texaco and Unocal

Skills and Capability Needs Are Evolving Portfolio Functions Skills Extrapolation • Petroleum System Focus: • Basin analysis • Regional synthesis • Leads and prospecting • Formation evaluation • Drilling and seismic operations • 2-D & 3-D seismic mapping • Seismic attribute analysis Opportunity Generators / Play Makers New Ventures Play Makers / Prospect Generators “Focus” New-Field Increasing Integration Engineering – Commercial – Financial Intense Data Density Sparse Prospect Generators / Reservoir Geoscience “Core” Exploration • Exploitation / Development Focus: • Reservoir scale description, visualization and modeling • High res 3-D mapping and attribute analysis • Integration of geology, geophysics and engineering Reservoir Geoscience / Reservoir Mgmt Reservoir Exploitation Interpolation

Integrated Field-Scale Exploitation & Reservoir Management l

Immersive Visualization Environment Work Processes Are Evolving . . . .

AAPG Demographics AAPG Membership Mean Age Year Year US Non-US

Relentless Change Industry consolidation Through-cycle strategic management International Complexion Scope Staffing Fundamental skills still a priority Dynamic learning organizations Increasing intensity of inter-disciplinary teaming and specialization Summary - What to Expect