Download

1 / 18

180 likes | 305 Vues

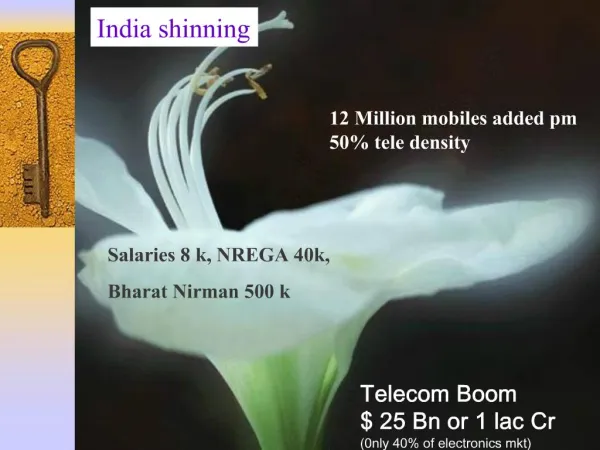

India shinning. 12 Million mobiles added pm 50% tele density. Salaries 8 k, NREGA 40k, Bharat Nirman 500 k. Telecom Boom $ 25 Bn or 1 lac Cr (0nly 40% of electronics mkt). At $ 1.15 Tr we are the third largest consumer on PPP basis. ?. Fastest growing Telecom & second largest.

E N D

India shinning 12 Million mobiles added pm 50% tele density. Salaries 8 k, NREGA 40k, Bharat Nirman 500 k Telecom Boom $ 25 Bn or 1 lac Cr (0nly 40% of electronics mkt)

At $ 1.15 Tr we are the third largest consumer on PPP basis. ? Fastest growing Telecom & second largest

Advantage India • India ranks better than China and Vietnam on the Index of Economic Freedomalthough it is lower than the world average as awarded by The Heritage Foundation and WALL STREET JOURNAL. • India scores higher than China and Vietnam on “World Rankings property rights”,which describes the protection of property and intellectual property rights • India has a score of 38 on “economic measure of income inequality” better than China (47) US (45) Japan(38) but poorer to UK (34).Shows equal distribution of wealth. • The annual supply of science and engineering graduates is higher than China and other developed countries • Over 2.3 million graduates and 0.7 million post-graduates each year • 2nd largest pool of scientists/ engineers in the world • Highest number of qualified engineers, second on trained doctors • 389 universities, 14,169 colleges, 1,500 research institutions

Is the Growth Inclusive for Indian Mfr / IPRs

Story is not Inclusive Neither Long term • Third largest Consumer consumes only .7% of the semi conductors • 25% of India’s trade deficit is bcoz of elctronics. • Not one Electronic hardware Co in the top 50 Scrips

Electronic Production Vs National GDP India has a long way to go

Not for the faint heart Yr 2008 World Electronics : 1500 Billion Dollars India’s share of imports : 3% (50 K Cr) world India’s share of exports : 0.1%. (1.6 K Cr) Ratios are adverse in automatic data processing units Telecom Demand expected : Rs 1 Lac Crore or 25 Bn $ Manufacture maximum : Rs 27000 Cr with 11% value add Royalty Payments : Rs 1650 Cr Software Export is 14000 Cr & Prod 40000 Cr

Chakravuyuh 140000 Cr Software export is important but is it long term view ? It enriches the IPR / Brand Owners Can India survive as Job worker or as sub contractor ? Or as an assembly line ? Will we ever have the Indian Brands ?

Information Highway Extremely dynamic , Vibrant & fast changing. • Mirages • Oases • Road kills Brand owners & IPR holders will survive the test of time.

Sectoral approach ! • Transnational Companies : Appreciate the contribution. they bring in technology, best practices, global experiences, much needed finances & employment. Slow absorption of these elements will lay a foundation. • Domestic Manufacturers :. Require support for stumbling & practice on the domestic turf. Provide market pull to create a level playing field lightweight Indian hardware designer needs to compete with Multinational technological heavyweights with abundant firepower. • Indian IPR creation : Support the talent pools dedicated to R&D so that some day we can boast of Indian brand names in Telecom hardware. IPR owner is at the top of the value chain & ultimate riches flow there hence Indian IPR development efforts deserve special incentives in long term national interest.

Invite FDI / Multinationals : The dream pipes today • Non availability of working capital at international cost • Encourage Mobile handset manufacturing • Robotics & futuristic technologies • Non availability of basic infrastructure to support large scale manufacturing • Eco system & Infrastructure for roads & ports. • Uniformity of Government policies & compliances

Domestic manufacturers – Prepare the Ground • Availability of working capital at international cost • Permit use of ECBs for working capital and for long term customer credit. .Most operators import their infrastructure due to attractive financing terms offered by global vendors – particularly the Chinese • Interest subsidy scheme for Small & Medium Enterprises dealing in ITA 1 items.. • Deemed export status: • The goods provided to the domestic Operators by the manufacturers to be deemed as Exports. • Encourage domestic manufacturing create a market pull: • Incentivse TELCOs to buy from domestic manufacturers . Higher the local value add higher the incentive to TELCO. This market pull will create an automated incentive for TELCOs to help domestic manufacturers improve quality of local manufacture & IPR, • There should be preference to local manufacturing in every large tender. • For telecom applications of national security, preference should be given to Indian products to ensure long-term support and national security of strategic assets. Revenue neutral reimbursements or concessions • Indian manufacturer pays taxes on end customer pricing. • Cascading effect of local state levies. Contributes by greater corporate Income tax & tax paid by staff. • It could be 15 to 20% if the “Value add” is over 40%.

Indian IPR – Prepare & Pray • Israel Experimentcover up to 50% of the R&D expenses, of Indian private sector companies that develop technology for defense & national security. This will create R&D-driven companies export Co’s. • Create dedicated fund for R&D: Initial corpus for R&D and product development out of USO fund. The initial corpus of Rs 100 crores can be created & further enhanced by allocating 10% of USO funds generated every year. These grants could be given as a conditional loan (at 0% interest) to cover R&D expenses, • No MAT for telecom R&D companies for 5 years:MAT should be waived off for the next 5 years for Indian R&D/product development companies, as an incentive to invest more and become world-class. • Enhance Tax credit on telecom R&D:Currently 125% expenditure on R&D is allowed to be deducted from taxable income. It is recommended it is made three times. • Reimbursement of excise duty: For products developed through recognized R&D in India, the company may be reimbursed the excise duty paid for sales of that product in India. This will enable them to be more competitive against global companies, who have already have a large volume base, before entering India.

Boost Exports – Gaytri dhyaan • Focus on Electronics exports and promotion of a key agenda for foreign trade missionsTelecom now & robotics soon will be the areas of growth for Indian companies. • Credit line of US $1 Billionspecifically dedicated for electronics exports by Indian companies for providing long-term finance to their customers. • Telecom & Electronics should be part of bi-lateral trade programs:Telecom exports from India should be included for all aid-in-grant programs. This will allow the world to experience Indian telecom hardware & help build a credibility of India as a destination for hardware. • Compensating exports for high transaction costs & appreciating Rupee. DEBP rates must be enhanced to make Indian hardware competitive. DEPB must also include reimbursement of local taxes, octroi, etc. as is allowed under WTO.

Lessons from China Experiment • China mandated technology transfer as a pre requisite to market access. • 100% export obligations for labor intensive manufacturing in China. • Specifications & technology requirements for China market so as to ensure technology absorption. • FDI norms & local participation followed meticulously.

Win Win Stategy • 5 Mn jobs that can triple by 2015. • $ 10 Bn exports by 2015. Balance of payment improve. • Self reliance on technology for tactical defense projects of national security. • Enhance national Image with Indian brand names in high technology areas. • Prepare ground for robotics the next sunrise industry.

Create Value Tweak the specifications in India & Indian manufacturers will have an advantage

Final punch Is there a reason for me to manufacture in India, Today ?? Thank you