Download

1 / 2

20 likes | 31 Vues

<br><br>The Union Budget 2017 definitely has taken some steps to encourage individuals, businessmen and SMSE companies to be more tax compliant in the coming years. Government's intent is not matched by action as too many and small- small tinkering of the various sections.For more details, Visit at - http://www.huconsultancy.com/blog/budget-2017-impact-mergers-and-acquisitions/

E N D

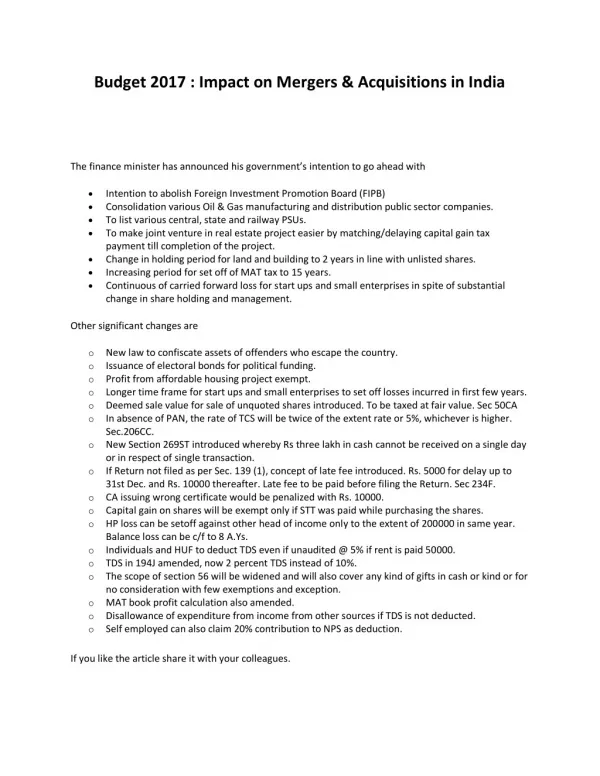

Budget 2017 : Impact on Mergers & Acquisitions in India The finance minister has announced his government’s intention to go ahead with Intention to abolish Foreign Investment Promotion Board (FIPB) Consolidation various Oil & Gas manufacturing and distribution public sector companies. To list various central, state and railway PSUs. To make joint venture in real estate project easier by matching/delaying capital gain tax payment till completion of the project. Change in holding period for land and building to 2 years in line with unlisted shares. Increasing period for set off of MAT tax to 15 years. Continuous of carried forward loss for start ups and small enterprises in spite of substantial change in share holding and management. Other significant changes are oNew law to confiscate assets of offenders who escape the country. oIssuance of electoral bonds for political funding. oProfit from affordable housing project exempt. oLonger time frame for start ups and small enterprises to set off losses incurred in first few years. oDeemed sale value for sale of unquoted shares introduced. To be taxed at fair value. Sec 50CA oIn absence of PAN, the rate of TCS will be twice of the extent rate or 5%, whichever is higher. Sec.206CC. oNew Section 269ST introduced whereby Rs three lakh in cash cannot be received on a single day or in respect of single transaction. oIf Return not filed as per Sec. 139 (1), concept of late fee introduced. Rs. 5000 for delay up to 31st Dec. and Rs. 10000 thereafter. Late fee to be paid before filing the Return. Sec 234F. oCA issuing wrong certificate would be penalized with Rs. 10000. oCapital gain on shares will be exempt only if STT was paid while purchasing the shares. oHP loss can be setoff against other head of income only to the extent of 200000 in same year. Balance loss can be c/f to 8 A.Ys. oIndividuals and HUF to deduct TDS even if unaudited @ 5% if rent is paid 50000. oTDS in 194J amended, now 2 percent TDS instead of 10%. oThe scope of section 56 will be widened and will also cover any kind of gifts in cash or kind or for no consideration with few exemptions and exception. oMAT book profit calculation also amended. oDisallowance of expenditure from income from other sources if TDS is not deducted. oSelf employed can also claim 20% contribution to NPS as deduction. If you like the article share it with your colleagues.

For more details, Visit at : - http://www.huconsultancy.com/blog/budget-2017-impact-mergers-and- acquisitions/