Download

1 / 2

20 likes | 91 Vues

<br><br><br>There are number of companies going for restructuring way, to gain more benefits from its core competencies. Know the difference between Slump Sale and Demerger procedure to be followed, companies act 2013, business transfer agreement, income tax. For the consultation, contact Huconsultancy (joint venture consulting services).For more details, Visit at - http://huconsultancy.com/slump-sale-vs-demerger/

E N D

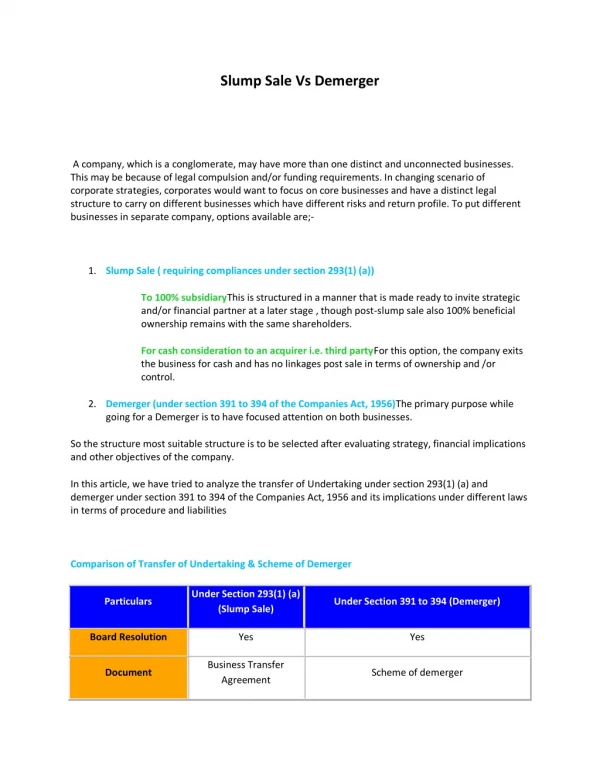

Slump Sale Vs Demerger A company, which is a conglomerate, may have more than one distinct and unconnected businesses. This may be because of legal compulsion and/or funding requirements. In changing scenario of corporate strategies, corporates would want to focus on core businesses and have a distinct legal structure to carry on different businesses which have different risks and return profile. To put different businesses in separate company, options available are;- 1.Slump Sale ( requiring compliances under section 293(1) (a)) To 100% subsidiaryThis is structured in a manner that is made ready to invite strategic and/or financial partner at a later stage , though post-slump sale also 100% beneficial ownership remains with the same shareholders. For cash consideration to an acquirer i.e. third partyFor this option, the company exits the business for cash and has no linkages post sale in terms of ownership and /or control. 2.Demerger (under section 391 to 394 of the Companies Act, 1956)The primary purpose while going for a Demerger is to have focused attention on both businesses. So the structure most suitable structure is to be selected after evaluating strategy, financial implications and other objectives of the company. In this article, we have tried to analyze the transfer of Undertaking under section 293(1) (a) and demerger under section 391 to 394 of the Companies Act, 1956 and its implications under different laws in terms of procedure and liabilities Comparison of Transfer of Undertaking & Scheme of Demerger Under Section 293(1) (a) (Slump Sale) Particulars Under Section 391 to 394 (Demerger) Board Resolution Yes Yes Business Transfer Agreement Document Scheme of demerger

Court Approval No Yes Yes By Postal Ballot Method Consent of Shareholders Yes, voting by ballot at court convened meeting Prior Intimation and NOC from office of Regional Director etc Required both to Regional Director as well as to Registrar of Companies No Requirement Mode of consideration Generally cash. Generally of shares. Receiver of consideration The Company The shareholders of the Company No specific Accounting Standard prescribed. Purchase method. to be recorded at book values to avoid violation of Section 2(19AA) of the Income Tax Act, 1961. No specific Accounting Standard prescribed. Purchase method Accounting Treatment Normal Stamp Duty as in the case of sale of property Stamp Duty Lower Stamp Duty or no stamp duty Time Generally 3months Generally 4 months. attracts long term or short term capital gains tax No tax if it is in compliance with section 2(19AA) of the Income Tax Act, 1961. Capital Gains 1.If a Company wants to raise funds and/or invite strategic /technology partner for a particular business but does not want to dilute its stake in the flagship/holding Company then it can go for transfer of undertaking u/s 293(1) (a) to a subsidiary Company. The transfer can be by way of exchange of shares. This way the Company is able to raise funds without diluting stake in the main company. 2.When a company which wants to completely exit particularly it could go for transfer of undertaking u/s 293(1) (a). 3.A Company having brought forward capital losses can go for transfer under this method. The Company can sell the undertaking at market value and can claim set off of capital gains for brought forward capital losses. For more details, Visit at - http://huconsultancy.com/slump-sale-vs-demerger/