HOME GUARANTY CORPORATION

430 likes | 760 Vues

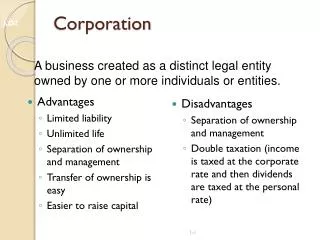

HOME GUARANTY CORPORATION. Historical Background. 1978. 1986. 2000. 1950. E.O. No. 535 Became Corporation & placed under the Ministry of Human Settlements. R.A. No. 8763 Renamed Home Guaranty Corporation. R.A. No. 580 Home Financing Commission. E.O. No. 90

HOME GUARANTY CORPORATION

E N D

Presentation Transcript

Historical Background 1978 1986 2000 1950 E.O. No. 535 Became Corporation & placed under the Ministry of Human Settlements R.A. No. 8763 Renamed Home Guaranty Corporation R.A. No. 580 Home Financing Commission E.O. No. 90 Renamed Home Insurance and Guaranty Corporation

Members of the Board SECRETARY OF FINANCE Ex-officio Chairman Secretary Cesar Purisima HUDCC CHAIRMAN Ex-officio Vice-chairman Vice President Jejomar Binay NEDA DIRECTOR GENERAL Ex-officio Member Dr. Arsenio Balisacan HGC PRESIDENT Ex-officio Member Atty. Manuel R. Sanchez Three (3) other members appointed by the President of the Philippines

MANDATES • Promote homebuilding and land ownership through self-help and cooperativism • To mobilize private funds for home lending

Guaranty Homebuyers Developers Financing Institution Guaranty Concept Developmental Loans Home Loans Home Acquisition Subdivision Development

Benefits of the HGC Guaranty Risk Cover 100%on outstanding principal obligation + interest and yields up to 11%

Benefits of the HGC Guaranty Exemption from BSP Capital Reserve Requirement for Credit Risk Guaranteed Loans are Zero-Risk (BSP Circular 280 s.2001)

Benefits of the HGC Guaranty Exemption from BSP Requirements on Real Estate Loans • Limit on REL (Sec. 1. c. BSP Circular 600 s. 2008) • Loanable amount may be increased up to 90% of appraised value of collateral (BSP Circular 343 s. 2002) • SBL (Sec. 1.E BSP Circular 425 s. 2004)

Benefits of the HGC Guaranty Tax exemption on interests and yields earned on guaranteed loans Up to 11%

Benefits of the HGC Guaranty Easing of Administrative Burden (in the event of call on the guaranty) Collection, Foreclosure & TCT Transfer are shifted to HGC

Benefits of the HGC Guaranty Sovereign Guaranty Confers classification and other advantages

Guaranty Programs • Retail Guaranty Program – covers individual housing loans secured by: • Real Estate Mortgage • Contracts-to-Sell • Developmental Guaranty Program – covers developer’s loan for: • Development of Residential Subdivision, Condos, Apartment • Working Capital • Guaranty for Securitization Program – ensures financial instruments issued for housing-related purposes, such as: • Bonds, Commercial Papers, A/MBS • Guaranty for Small Loans for Housing – ensures unsecured housing-related loan transactions, such as: • Microfinance Housing Loans • Salary Loans, Multi-purpose loans to be used for housing

Retail Loans Eligible for Guaranty • Purchase of house & lot, townhouse, condominium unit and any other single family dwelling; • Purchase of lot and construction of house; • Purchase of lot only; • Purchase of lot on which the house of the Borrower/Mortgagor presently stands; • Major repair, improvement or expansion of an existing house or dwelling unit; • Refinancing of an existing loan, which was principally used for any of the above-mentioned purposes; • Financing of Contracts-to-Sell executed by Developers in favor of its buyers covering purchase of residential units in a developed subdivision or condominium; and • Purchase of residential farm lot

Types of Guarantee Coverage (Form of Guaranty Call Payment) • STANDARD COVERAGE • Call Payment is in the form of HGC Debenture Bond if default occurs within the 1st five (5) years of guarantee coverage • Call Payment is Cash if default occurs after five (5) years of guarantee coverage • BOND COVERAGE • Call Payment is in the form of HGC Debenture Bond regardless of the period or timing of the default. • MODIFIED CASH PAYMENT • Call payment is in cash based on a scheduled monthly amortization. • Payment shall commence on the first month that the loan becomes delinquent until the loan maturity.

Features of the HGC Debenture Bond Classification : Government Securities Term : 3 to 5 years Face Value : OB + accrued interest (Max of nine months) Coupon rate : The lowest of Market Rate, Mortgage/CTS Rate, or 8.5% p.a. Tax exemption : Up to the coupon rate of the bond Interest Servicing: Semi-annual Bond Redemption: Principal payable at maturity Tradability: Traded in the market

Annual Guaranty Fee (Retail Housing Loan)

Annual Guaranty Fee (Developmental Housing Loan)

Guaranty for Small Loans for Housing Guaranty Financing Institution Lends to individual borrowers Borrowers for home improvement and repairs

Terms and Conditions of the Guaranty • Eligibility of FIs: • Track record of at least three (3) years in implementing sustainable microfinance programs; • Capital Adequacy Ratio (CAR) of not lower than 12% for BSP-supervised FIs; • Latest CAMELS rating of at least “3” for BSP-supervised FIs; • With collection efficiency of at least 95%; • Capacity and technical capability to offer small loans for housing; and • No arrearages in borrowings from wholesale lenders. • Loan Value Eligible for Guaranty: • Maximum of P400,000.00[1] per borrower [1] Loan amount may be adjusted/increased upon the approval of the HUDCC and the BSP

Terms and Conditions of the Guaranty (cont.) • Purpose/s of the Loan: • House and/or lot acquisition for housing; • House construction; and • Home improvement/repairs. • Eligible Borrowers: • Existing depositor/client/member; • Borrowers who are determined by the FI to be eligible for small loan for housing, provided that: (a) they do not have an existing small loan for housing; and (b) loan payments should not exceed 60% of their income as determined by the FI’scash flow analysis; • With verifiable source of income; and • With good track record of loan repayment for the last three (3) loan cycles of any loan type from the FI. 27

Terms and Conditions of the Guaranty (cont.) • Payment: • Frequent amortization (daily, weekly, monthly); and • Loan payments should not exceed 60% of client’s net disposable income as determined by the FI’scash flow analysis. • Loan Term: • Up to 15 years for loans above P150,000 and/or for lot acquisition and house construction; and • Up to 5 years for loans not exceeding P150,000 availed for home improvement and repairs. 28

Terms and Conditions of the Guaranty (cont.) • Event of Default: • Consecutive non-payment of loan amortization by the borrower depending on the payment schedule as follows: • Premium Structure: • The guaranty premium is two percent (2%) per annum of the outstanding loan balance. 29

Terms and Conditions of the Guaranty (cont.) • Maximum Allowable Guaranty Call: • The FIsmay call on the HGC guaranty to the extent of 1.2% of the total enrolled account. • Premium Refund: • In case there is no call on the guaranty at the end of the guaranty period, the FI shall be entitled to a premium refund of up to 1% of the guaranteed loans. • Other conditions: • Within one (1) month from release of the loan, the FI shall submit to HGC a proof of the borrower’s utilization of the proceeds as specified in the loan application; 30

Applies for guaranty line • Submits: • Application letter • Company Profile • Profile of Stockholders & Key Officers • Audited F/S (for the last 3 years) • Credit Policies & Guidelines • Prospective Enrollments • CAMELS Rating (Banks)/PESO Rating (Coop) • Application Fee (P10,000) 2 3 4 5 1 Guaranty Line Application HGC Evaluates application Elevates to HGC Board for approval Sends notice of approval/disapproval Guaranty Contract Financial Institution Executes Contract of Guaranty

COG Enrollment Procedure Enroll accounts for guaranty coverage, submits: Enrollment Letter containing warranties that: 1.Bank has undertaken credit evaluation of account 2. Loan documents are valid 3. TCT is clean, free from lien 4. All loans are within LTV limits Batch List 1. At least P 1.0 M or 10 accounts 2. Information about the borrower, the loan, and collateral Premium Payment Processes Certificate of Guaranty Issues Certificate of Guaranty (signed by HGC President) Financial Institution

Post Audit of Guaranteed Loans HGC validates sufficiency and orderliness of loan documentation with the FI HGC inspects housing unit of the borrower Financial Institution

1 2 BORROWER Call Procedure Option Notice of call Borrower defaults (6 mos. Non-payment of monthly amortization) 30 calendar days from date of default Pays Call Evaluates Call 30 calendar days from conveyance of original loan documents 30 calendar days from receipt of notice of call IF VALID Option FORECLOSURE Financial Institution Loan documents

Call Documents • Documents to be submitted upon call on the guaranty within 30 calendar days from default date: • - Notice of claim • - Demand letter of bank to borrower • Statement of account and ledger • Copies of TCT, Tax Declaration, • vicinity map, lot plan and house plan • - Bank appraisal report • Audit evaluation sheet • Documents to be submitted after receipt of Notice of Claim Approval within 30 to 180 calendar days from receipt of notice of approval : • - Registered Deed of Assignment and Conveyance • - TCTs, tax declaration, tax receipts • - PNs, Loan Mortgage Agreement, REM • Fire Insurance Policy duly assigned to HGC • Bank Certification that all taxes and Homeowners Association dues are updated

Performance Indicators Guaranty Capacity as of Dec. 2012P 145.39B Outstanding Guaranty as of Dec. 2012 P 82.40B Net Income from Operations as of Dec. 2012 P 457.59M

Visit us at: Home Guaranty Corporation 335 Sen. Gil Puyat Avenue, Makati City Tel. No. +63 2 8964116 www.hgc.gov.ph