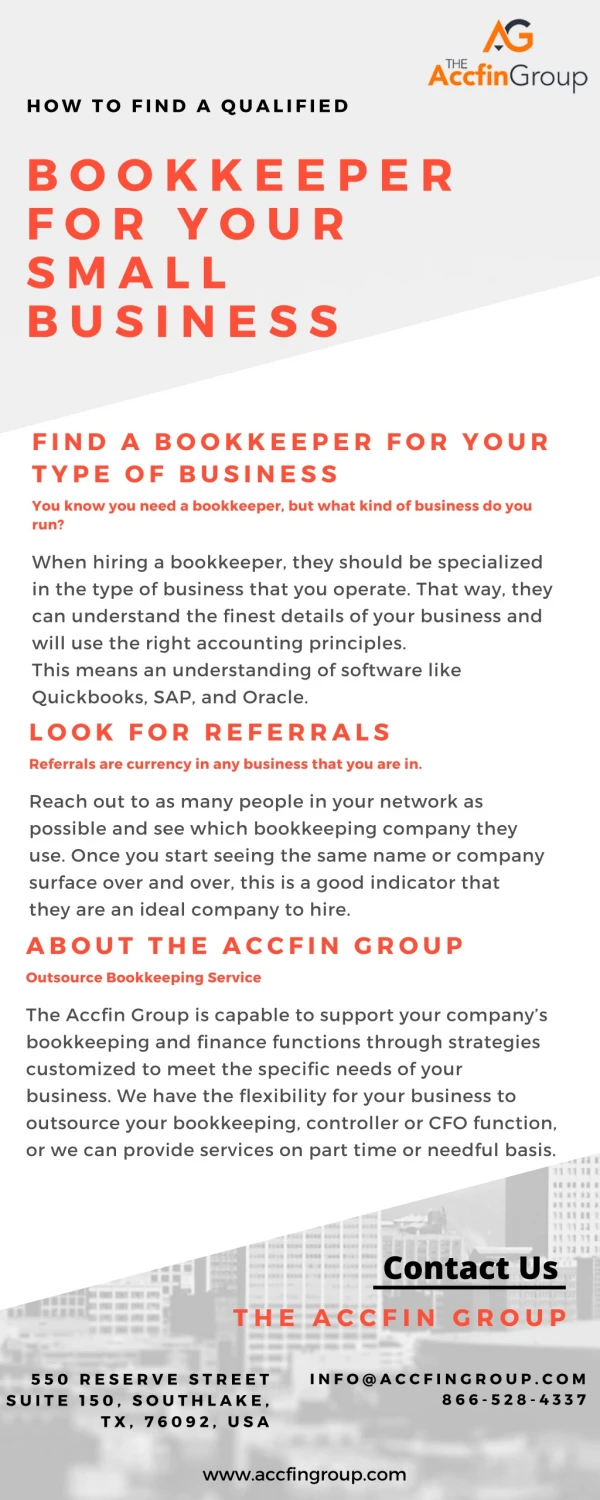

Download

1 / 2

20 likes | 36 Vues

Looking for ways to improve your small business and have found nothing? Fear no more! This article entails 5 tips on bookkeeping practices that will actually improve your small business. Some of these may already be familiar to you like paying your bills accurately and on time, watching unusual changes in sales and expenses, and tracking accounts receivables. <br>

E N D

5 Tips on Bookkeeping Practices That Will Improve Your Small Business Looking for ways to improve your small business and have found nothing? Fear no more! This article entails 5 tips on bookkeeping practices that will actually improve your small business. Some of these may already be familiar to you like paying your bills accurately and on time, watching unusual changes in sales and expenses, and tracking accounts receivables. 1.Set up sales and revenue targets and monitor your progress closely. Businesses who wish to succeed are businesses with a goal. Success only comes to those who know what they want and work for what they want. You should always know what to spend money on and how much you’ll spend. Your budgeting dictates a major part of how good your business will perform. It is also important to compare your performance to the budget spent. This allows you to gauge how efficient the budgeting and the business operations are. Unusual spikes or shifts in sales or expenses should always be monitored. Discovering the sources of such changes may lead to game-changing opportunities for the business. Your gross profit serves as a semi-accurate indicator of the business’s performance. Learn to gauge changes in your gross profit and make all the necessary pricing or purchasing decisions. 2. Watch closely your accounts receivable from customers. Follow up on your customers’ debts and make sure that you record each one. Good businesses know how to manage its accounts receivable. Great businesses monitor them closely like a hound on the hunt. For the purposes of keeping your books tidy and orderly you must pay your bills accurately and on time. Not only does this make you less likely to incur additional expenses but it keeps your books on track and organized.

3. Reconcile your bank account. There may be changes in the business’s bank account which are not recorded in its books. This is why bank reconciliation is important, it ascertains the differences between the business’s bank account and the business’s accounting records, and it makes sure that the business is aware of the changes to its bank account. 4. Set up a chart of accounts that best keeps track of all your bookkeeping information. Worksheets, income statements, balance sheets and everything else that goes into bookkeeping is defined by the chart of accounts. Good ones are ones that track every account that is required for bookkeeping from cash to expenses. To keep organized, balancing and recording daily sales and cash receipts must be done daily. This makes sure that all information is current and reliable. 5. Take care of slow moving inventory. Slow moving inventory may cause trouble for bookkeepers. They can cause confusion during bookkeeping as they might arrive unexpected. Learn to cope with unexpected situations as this will make you a better bookkeeper and a better businessman. Keep track of your inventory by counting them physically then compare them to your accounting records. This will make sure that your accounting records are accurate and up-to-date.