Maridive & Oil Services - Underweight Recommendation Analysis

Maridive & Oil Services (MOS) is a leading offshore oil services company with a diverse international presence. Despite positive factors like revenue diversification and fleet expansion plans, risks such as lack of contract visibility and market challenges exist. Key shareholder structure and performance indicators also play a crucial role in evaluating the company.

Maridive & Oil Services - Underweight Recommendation Analysis

E N D

Presentation Transcript

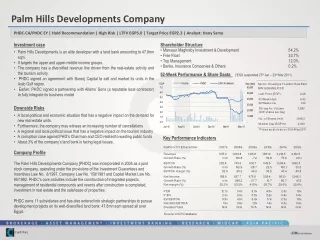

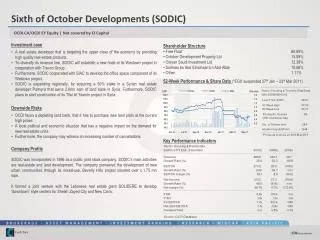

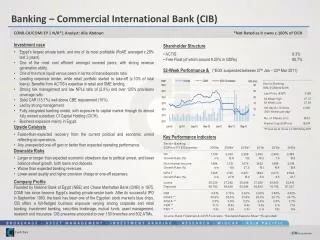

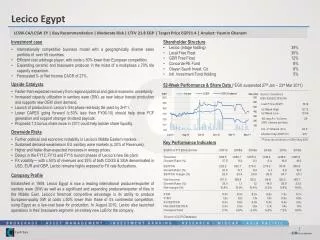

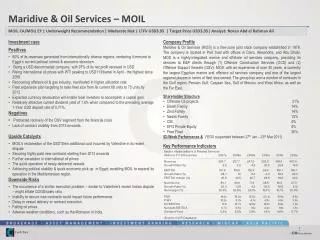

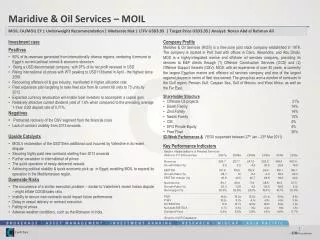

Maridive & Oil Services – MOIL MOIL.CA/MOIL EY | Underweight Recommendation | Moderate Risk | LTFV USD3.95 | Target Price USD3.95| Analyst: NoranAbd el Rahman Ali Company Profile Maridive & Oil Services (MOS) is a free-zone joint stock company established in 1978. The company is located in Port Said with offices in Cairo, Alexandria, and Abu Dhabi. MOS is a highly-integrated marine and offshore oil services company, providing its services to E&P clients through (1) Offshore Construction Services (OCS) and (2) Offshore Support Vessels (OSV). MOS, with an experience of over 30 years, is currently the largest Egyptian marine and offshore oil services company and one of the largest regional players in terms of fleet size owned. The group has won a number of contracts in the Gulf region, Persian Gulf, Caspian Sea, Gulf of Mexico, and West Africa, as well as the Far East. Investment case • Positives • 90% of its revenues generated from internationally diverse regions, rendering it immune to Egypt’s current political turmoil & economic downturn. • Being a USD denominated company, with 97% of its net profit received in USD • Rising international oil prices with WTI peaking to USD113/barrel in April - the highest since 2008. • Recovering offshore oil & gas industry, manifested in higher utilization rate. • Fleet expansion plan targeting to raise fleet size from its current 68 units to 75 units by 2012. • Expected currency devaluation will enable local investors to accomplish a capital gain. • Relatively attractive current dividend yield of 1.6% when compared to the prevailing average 1-Year USD deposit rate of 0.71%. • Negatives • Protracted recovery of the OSV segment from the financial crisis . • Lack of contract visibility from 2013-onwards. Upside Catalysts • MOIL's reclamation of the USD10mn additional cost incurred by Valentine in its recent dispute • Securing highly-paid new contracts starting from 2013 onwards • Further escalation in international oil prices • The quick operation of newly-delivered vessels • Achieving political stability & quick economic pick up in Egypt; enabling MOIL to expand its operation in the Mediterranean region. Downside Risks • The occurrence of a similar execution problem – similar to Valentine’s recent Indian dispute – might inflate COGS/sales ratio. • Inability to secure new contracts could impact future performance. • Delay in vessel delivery or contract execution. • Falling oil prices • Adverse weather conditions, such as the Monsoon in India. • Shareholder Structure • Offshore Oil projects 21% • Eleish Family 14% • Zeid Family 14% • Nadim Family 13% • CIB 4% • EFG Private Equity 4% • Free Float 30% • 52-Week Performance &(*EGX suspended between 27th Jan – 23rd Mar 2011) Key Performance Indicators