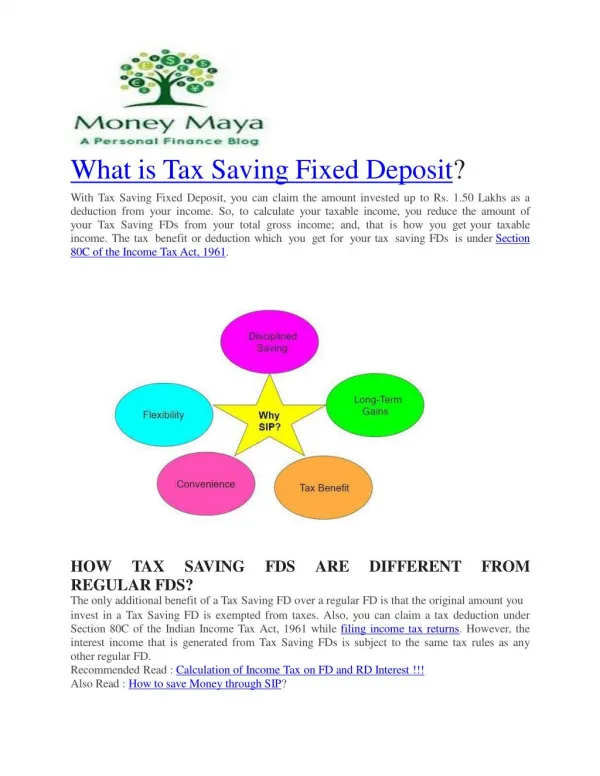

Tax Saving Structures

Explore the benefits of setting up various international company structures, such as Malta, Luxembourg, and Dutch holding companies. These structures offer significant tax advantages, including no withholding tax on outbound dividends, income tax exemptions, and capital gains tax protection through Double Tax Treaties (DTT) with several countries. Gain insights on effective tax rates ranging from 0% to 6.25% and understand the implications for interest and royalty payments, ensuring compliance and maximization of profits in your investment strategies.

Tax Saving Structures

E N D

Presentation Transcript

No withholding tax on outbound dividends MALTA COMPANY • Tax exemption on income • 0% withholding tax based on the PSD EU COMPANY • Capital gains tax protection based on several DTT’s including Denmark, Italy, Sweden, Germany, Czech Republic, Poland, Slovenia, Spain, Portugal, United Kingdom

No withholding tax on outbound dividends MALTA COMPANY • Tax exemption on income • 0% withholding tax based on the broad implementation of PSD LUXEMBOURG HOLDING COMPANY • Capital gains tax protection based on DTT

No withholding tax on outbound dividends MALTA COMPANY • Tax exemption on income • 0% withholding tax based on the broad implementation of PSD DUTCH HOLDING COMPANY • Capital gains tax protection based on DTT

No withholding tax on outbound dividends MALTA COMPANY • Licensing or financing activities • Profits subject to 0-6.25% effective tax GERMAN COMPANY • 0% withholding tax on interest and royalty payments based on DTT

MALTA COMPANY Interest Payment • 0-6.25% effective tax on passive interest income • No transfer pricing documentation Loan TREATY COUNTRY/ EU COUNTRY AFFILIATED DEBTOR • Reduction of WHT based on treaty • Exemption from WHT based on EU interest and royalty directive

MALTA COMPANY Royalty Payment • 0-6.25% effective tax on passive licensing income • No amortisation – IP contributed at nominal value License TREATY COUNTRY/ EU COUNTRY AFFILIATED DEBTOR • Reduction of WHT based on treaty • Exemption from WHT based on EU interest and royalty directive

No withholding tax on outbound dividends MALTA COMPANY • 0-5% net effective tax on trading profits Country A High tax country

FOREIGN SHAREHOLDER • No withholding tax on outbound dividends MALTA COMPANY • Refund on dividend distribution • Profits subject to net effective tax of 5% plus gaming tax based on turnover MALTA LICENSED GAMING COMPANY

SHAREHOLDER • No withholding tax on outbound dividends MALTA COMPANY • Refund on dividend distribution • Profits subject to net effective tax of 5% MALTA E-COMMERCE COMPANY

No withholding tax on outbound dividends CYPRUS COMPANY EFFECTIVELY MANAGED & CONTROLLED IN MALTA • Effective management and control in Malta • Company subject to tax on income arising and on income remitted to Malta only • Income not subject to tax in Cyprus

OFFSHORE COMPANY Loan Interest Payment MALTA COMPANY • 0-6.25% effective tax • No transfer pricing documentation • No withholding tax on interest payments Loan Interest Payment TREATY COUNTRY/ EU COUNTRY AFFILIATED DEBTOR • Reduction of withholding tax based on treaty • Exemption from WHT based on EU interest and royalty directive

OFFSHORE COMPANY License • Owner of IP Royalty Payment MALTA COMPANY • 0-6.25% effective tax • No transfer pricing documentation • No withholding tax on royalty payments Sub- License Royalty Payment TREATY COUNTRY/ EU COUNTRY AFFILIATED DEBTOR • Reduction of withholding tax based on treaty • Exemption from WHT based on EU interest and royalty directive

Tax transparent • Income attributable to the trust is not subject to tax in Malta • Look-through approach – income directly received by the beneficiary • Non-residents not subject to tax other than on income arising in Malta or the transfer of immovable property in Malta MALTA TRUST