Download

1 / 20

200 likes | 366 Vues

Canadian Bond Market Presentation. January 18, 2011. John Braive, Vice-Chairman. CONFIDENTIAL. Market Review. Key Developments (Q4’10).

E N D

Canadian Bond Market Presentation January 18, 2011 John Braive, Vice-Chairman CONFIDENTIAL

Market Review • Key Developments (Q4’10) • BoC on hold at 1.00%, but the market’s priced for hikes to resume in May 2011. We expect no further action until H2’11. No Fed Funds hike expected until 2012. • Longer-term yields rose in response to evidence that the economy had avoided a double-dip recession and due to rising concerns that the Fed’s second round of quantitative easing would lead to higher inflation. • Yield curve has flattened modestly since end of Q3, as 2-year yields rose 30 bps, while 30-year yields rose 18 bps, reflecting rising inflation fears and a resumption of the “risk on” trade. • Corporate bonds outperformed GoC and Provincial bonds, given their shorter duration and stable spreads. However, all had negative returns for the quarter. • DEX Corporate Spread narrowed 2 bps, to 138 bps; up 3 bps YoY. DEX Provincial spread narrowed 2 bps, to 118 bps; down 10 bps YoY. Investors remain hungry for yield. • New issue activity remained strong with total issuance during the quarter at $20.9 BN, with YTD at $82.9 BN vs $60.7 BN for same period in ’09. Issuance was higher that seen in 2009 and 2008. Source: CIBC Global Asset Management Inc. CONFIDENTIAL

markopou: Pat responsible for comments quarterly. Market Review • Yields – short-term rates up, long-term yields stable March 2010 June 2010 December 2010 September 2010 • Yields rose in Q4 as QE2 started, increasing inflation fears and encouraging the “risk on” (sell bonds / buy stocks) trade. Source: CIBC Global Asset Management Inc. CONFIDENTIAL

markopou: Pat responsible for comments quarterly. Market Review • Yield Curve – Still steep, but flattening trend started • The yield curve flattened further in the quarter as longer-term yields rose less than shorter-term yields rose as QE2 began. • The steep curve anticipates tightening by the Bank of Canada in 2011. • Current steepness of the yield curve provides resistance to long rates rising significantly. Source: PC Bond, a business unit of TSX Inc. CONFIDENTIAL

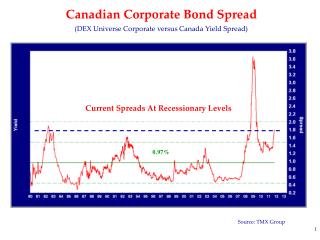

markopou: Pat responsible for comments quarterly. Market Review • Credit - Corporate Yield Spread Dec 31 ’10 +138 bps Low: Jan 31, ’86 +28 bps High: Dec 29 ’08 +366 bps Avg: +95 bps • Spreads are still near prior credit crisis levels, and were largely unchanged for the year. • We expect continued volatility, but remain overweight given expectations that corporate bonds will outperform government bonds over the next year. Source: PC Bond, a business unit of TSX Inc. CONFIDENTIAL

markopou: Pat responsible for comments quarterly. Market Review • Credit – Corporate Bond Issuance • Q4 supply was robust at $20.9, and was $82.9 BN in ‘10 vs $60.7 in ’09. • Maple bond issuance returned, with $4.4 BN in ‘10 issuance surpassing 2009 levels, but well below the ~$25BN level seen in each of ’06 and ‘07. • Canadian banks were busy issuing in Canada and the U.S.; $26.8 BN issued domestically in ‘10. • The calendar was well managed, helping to keep spreads stable. Source: PC Bond, a business unit of TSX Inc. CONFIDENTIAL

markopou: Pat responsible for comments quarterly. Market Review • Credit – Tier 1 • Basel III will likely result in the early call of only those Tier 1 bonds with maturity dates after 2023. We don’t hold them in the Model Accounts. • Outstanding Tier 1 and older subordinated debt will likely lose capital treatment on a straight-line basis from 2013 – 2023. But they are not expected to be called. • Basel III subordinated debt issuance will likely resume. Source: PC Bond, a business unit of TSX Inc. CONFIDENTIAL

markopou: Pat responsible for comments quarterly. Market Review • Credit - Long Provincial Yield Spread Dec 31 ’10 +81 bps Low: May 22 ’07 +38 bps High: Mar 6 ’09 +153 bps Avg: +67 bps • Long-term provincial spreads tightened (-6 bps to 81 bps in Q4) in the search for yield and longer-duration assets. • Overall, provincial spreads tightened 2 bps in the quarter to 118 bps; down 10 year/year. • Long-term provincial spreads look expensive as compared to corporates. Source: PC Bond, a business unit of TSX Inc. CONFIDENTIAL

Canadian Fixed Income • Sector Returns – DEX Universe Bond Index 1 year – As at December 31, 2010 Quarter – As at December 31, 2010 Source: PC Bond DEX Universe Bond Index is a trademark of TSX Inc. CONFIDENTIAL

Portfolio Returns • Periods ending December 31, 2010 * Returns are before fees In Canadian dollars Source: CIBC Global Asset Management Inc. Performance is shown before management and custodial fees CONFIDENTIAL

Canadian Fixed Income – Active Management • Attribution – 12 months ending December 31, 2010 Represent characteristics of CIBC Pooled Fixed Income Fund – 80020 Source: PC Bond and CIBC Global Asset Management Inc. CONFIDENTIAL

Economy – National Bureau of Economic Indicators • Both income growth and employment are tracking well below prior recoveries. • Lack of income growth is a serious headwind. • In spite of massive fiscal and monetary stimulus, the economy is expanding well below historic trends. U.S. Personal Income Less Transfers Current vs. Average Expansions U.S. Nonfarm Payroll Current vs. Average Expansions Source: Datastream and CIBC Global Asset Management Inc. CONFIDENTIAL

Economy – Housing • An unprecedented run-up in prices has led to an unprecedented supply of homes. • The GoC just introduced measures to restrict the supply of credit to the housing sector. • Our valuation model for Canada suggests an extended period of flat prices, like the early 1990’s. • Weak housing impacts consumers’ spending attitudes. U.S. Months’ Supply of Existing Homes Canadian Housing Valuation: home prices vs. fair value & deviations from fair value (%) Source: Datastream and CIBC Global Asset Management Inc. CONFIDENTIAL

Economy - Debt • Households have become over extended with record amounts of debt • Debt has to be paid back … or written-off. • Loan demand will remain soft as attitudes toward debt become more conservative. Canadian Household Credit as % of GDP U.S. Household Credit as % of GDP Source: Datastream and CIBC Global Asset Management Inc. CONFIDENTIAL

Economy - Savings • The consumer can’t do the heavy lifting in this recovery. • Lowered return expectations should lead to higher savings. • An aging population is increasing savings to meet their retirement needs. • Demand for safe income is rising. • Bonds should benefit. U.S. & Canada Savings Rate Source: Datastream and CIBC Global Asset Management Inc. CONFIDENTIAL

Inflation – Wages • Wage costs are the best predictor of future inflation. • U.S. Unit labour costs – the combination of productivity, output and wages – will remain low. • The excess slack in labour markets and in industrial capacity should persist. Canada Average Hourly Earnings vs. Unit Labor Cost Source: Datastream and CIBC Global Asset Management Inc. CONFIDENTIAL

Interest Rates – Trend The Secular Rally is Intact • Interest rates remain in their downward channel. • There is a strong correlation between short-term and long-term interest rates. • The Federal Reserve and the Bank of Canada will keep administered rates low for an extended period. • CIBC GAM forecasts a range of 3.25% to 4.25% for long-term yields. Government of Canada – 30-year Yield Source: PC Bond, a business unit of TSX Inc. and CIBC Global Asset Management Inc. CONFIDENTIAL

Outlook • Forecast Yield Range • The Bank of Canada will resume raising short-term rates later this year. CGAM expects another 0.50% increase under the base case scenario (Sluggish Recovery). • We expect no action from the U.S. Federal Reserve this year. • Longer-term bonds should remain in a trading range given the headwinds of fiscal policy, continued deleveraging, and Basel III’s impact. 1 YEAR FORECAST Source: CIBC Global Asset Management Inc. CONFIDENTIAL

markopou: Pat responsible for comments quarterly. Strategy • Current • Duration neutral vs. index. • Overweight mid-term bonds, given expectations that the curve will remain steep. • Portfolio yield still higher than benchmark (+75 bps at year-end 2010). • Selectively adding corporate positions – both investment grade and high yield. Source: CIBC Global Asset Management Inc. CONFIDENTIAL

Strategy markopou: Pat to update quarterly. • Risks to Outlook • Credit spreads widen – risk of European sovereign issues • Yields rise markedly – due to higher than forecasted inflation • Yield curve flattens – greater tightening than anticipated Source: CIBC Global Asset Management Inc. CONFIDENTIAL