Download

1 / 27

270 likes | 297 Vues

STP/T+1 Value Proposition Survey October 15, 2002. Canadian Capital Markets Association (CCMA). Contents. Executive Summary Survey Approach Survey Results Survey Results Are Conservative Transaction Correction Costs Operational Efficiency Operational Risks and Financing Costs

E N D

STP/T+1 Value Proposition SurveyOctober 15, 2002 Canadian Capital Markets Association (CCMA)

Contents • Executive Summary • Survey Approach • Survey Results • Survey Results Are Conservative • Transaction Correction Costs • Operational Efficiency • Operational Risks and Financing Costs • Other Benefits • Survey & Extrapolation Results • Broker/Dealers • Investment Managers • Custodians • Other Participants • Appendices • Participants – Model Review and Summary • Participant Assumptions and Caveats • Benefits Canada Extract • Assumption Validation • Risk Definitions • Project Process and Timelines • Model Template by Industry Segment • Survey Data Collection Sheets 1

Executive Summary • CCMA’s Value Proposition Survey was commissioned by the CCMA and conducted by Cap Gemini Ernst & Young Canada Inc. (CGEY) between April 26, 2002 and June 24, 2002, with further validation taking place during the summer. The survey represents the first step of the Communications Workstream of the CCMA Industry Plan of February 2002. Participants surveyed represented key stakeholders from the Canadian Securities Industry Value Web. • The survey suggests that straight-through processing(STP)/T+1 initiatives can realize significant benefits to the Canadian capital markets. Of the annual expected benefit conservatively estimated at CDN $190.3 million, 72% or CDN $137.3 million can be attributable to STP. The survey focused on domestic institutional trades and excluded retail and cross-border trades where additional benefits may be realized. Also, as the analysis is based on current trade volumes, benefits could be higher if volumes rise. The survey focused on benefits and no analysis of related costs is provided. • Transaction Correction Cost Reductions (surveyed) CDN $35.0 million 18% • Operational Efficiency Gains CDN $42.3 million 22% • Operational Risks and Financing Cost Savings CDN $45.0 million 24% • Infrastructure Savings and Opportunities CDN $5.0 million 3% • New Revenue Sources CDN $10.0 million 5% • Annual Benefits from STP CDN $137.3 million 72% • Reduction in Default Risk from Moving to T+1 CDN $53.0 million 28% • Total Benefits from STP and T+1 CDN $190.3 million 100% • The survey also suggests that efficiency resulting from STP may be a better motivator to continue with current industry initiatives. In addition, with the revision to the Basle Capital Accord, operational risk represents an area of opportunity for bank-owned operations to reduce risk-based capital allocation requirements. In addition to participant responses, the survey collated information from reports published by the Securities Industry Association (U.S.), The TowerGroup and The Forrester Group. Where U.S. industry numbers were used as the basis, benefits were estimated conservatively to factor in market and data differences. 2

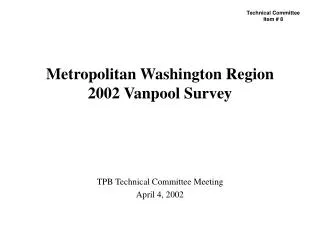

Canadian Securities Industry Value Web Stakeholders Participants Surveyed 3

Industry segments develop and validate the model to quantify benefits. Model is distributed to survey participants. Participants confidentially populate model. CGEY aggregates and extrapolates for industry segments; participants and associations review and validate the results. Survey Approach • The Canadian Capital Markets Association launched a survey to quantify the benefits of STP/T+1 for the Canadian Securities Industry. The CCMA intends to use this information as a part of its continuing communication process to the industry and stakeholder groups. • Custodians, Broker/Dealers, Investment Managers, Infrastructure Providers (Exchanges and Depositories), and Transfer Agents were contacted to develop and validate the model designed to quantify benefits arising from the lowering of transaction costs attributed to improved STP, reduced errors and manual intervention. The model was then distributed to a number of industry participants and their Associations. • Working with the CCMA, CGEY developed a four-step approach to collect and collate the information: • Participants used readily available data to populate the model. Survey responses were collated and extrapolated for each industry segment where appropriate. Participants’ assumptions and caveats were also captured and reported. • Participants validated the extrapolated results and this report. 4

Survey Results Based on survey feedback, there are six areas where STP/T+1 can benefit the Canadian Securities Market: Potential Benefit % Reduction in Transaction Correction Cost Reductions CDN $35.0 million 18% Improvement in Operational Efficiency Gains CDN $42.3 million 22% Reduction in Operational Risks and Financing Cost Savings CDN $45.0 million 24% Infrastructure Savings and Opportunities CDN $5.0 million 3% New Revenue Sources CDN $10.0 million 5% Annual benefit from STP CDN $137.3 million 72% Reduction in Default Risk from Moving to T+1 CDN $53.0 million 28% Annual benefit from STP and T+1 CDN $190.3 million 100% STP T+1 72% of the benefits identified by the participants were STP-related. 5

Survey Results Are Conservative • The analysis of benefits in each of the areas on the preceding page is provided on the attached sheets. The results should be read in conjunction with the assumptions and caveats identified by survey participants (see page 18) and with regard to the following limitations (with others noted in this report) that suggest that the survey results are conservative: • The analysis is based on current annual trade volumes. If trade volumes increase in future years, the benefits could potentially be much higher. • The survey focused on domestic institutional trades. The Canadian Depository for Securities Limited (CDS) reported the volume at 5.77 million trades annually. Cross-border trades of 12 million and retail activity of 28.1 million that settle through CDS were not included in the survey, however, they have been identified as areas where additional benefits to the industry may be realized. • SWIFT estimates that cross-border trade repair costs are in the region of USD $6 to $16 per trade (source: The Forrester Group, The Real Benefits of T+1, September 2001). Considering that there are 12 million cross-border trades a year (source: CDS), the error correction costs associated with these trades could be significant. • The survey did not cover other stakeholders in the Canadian Security Industry Value Web for whom STP/T+1 could realise some benefits: • Institutional Clients • High Net Worth Retail Clients • Retail Clients • Financial Planners • Retail Broker Front Office • Issuers • Potential Basle Operational Risk capital savings are excluded as they cannot be quantified. 6

Transaction Correction Costs • The initial focus of the CCMA survey was transaction correction costs. STP/T+1 is expected to lower the percentage of transactions requiring correction and, hence, the transaction correction costs. • Without considering growth in volumes, survey participants expect a reduction in transaction correction costs: • Broker/Dealers surveyed expect the percentage of transactions that require intervention to be reduced by 84%. Applying the incremental cost per transaction requiring intervention, and extrapolating over the annual institutional trade volumes of 5.77 million (source: CDS), this represents a benefit of $24 million. Over 85% of the savings come from receiving trades electronically and on a timely basis in an STP environment. • Investment Managers surveyed expect the percentage of transactions that require intervention to be reduced by 84%. As a result, the transaction correction cost is expected to be lower, resulting in savings of CDN $320,000. Based on data from Benefits Canada (Nov. 2001 edition) the total assets under management for participants surveyed was CDN $144 billion, representing 12.5% of the industry. When extrapolated over the industry of about CDN $1.15 trillion (Benefits Canada), this represents a potential savings of CDN $2.5 million for the Investment Manager industry. • Custodians surveyed expect the percentage of transactions that require intervention to be reduced by 70%. As a result, per-transaction correction cost is expected to be lower by CDN $ 1.47. When extrapolated over annual institutional trade volumes of 5.77 million (source: CDS), this represents a benefit of CDN $8.5 million. • Infrastructure Providers (Exchanges, Depositories) and Transfer Agents expect minimal reductions (if any) in the percentage of transactions that require intervention and hence, the benefit is not expected to be significant. However, participants identified some related benefits such as CDS’s System X/CDSX and potential revenue opportunities that have been captured on the attached sheets. • Taken together, the reduction in transaction correction costs can realize benefits to the industry in the region of CDN $35 million annually. 7

Operational Efficiency • The SIA T+1 Business Case almost entirely attributed benefits from T+1 to result from operational efficiency due to STP. While the survey focused on transaction correction costs, participants identified other areas of operations where STP will yield benefits. As the survey did not include all aspects of operations, participants indicated the need to highlight any related benefit. • The SIA T+1 Business Case Study (July 2000) estimated the annual net benefits from STP/T+1 to be in the region of US $2.7 billion, mainly relating to the following participants: • Investment Managers in the Trade Agreement Phase resulting from reduced reconciliation and resolution activities due to (i) matching of NOEs to allocations by utilities, (ii) reduced effort to create allocation sets at the investment manager, and (iii) improved error resolution processes for broker/dealer and investment manager; • Broker/Dealer in the Settlement Agreement Phase resulting from reduction in time and effort associated with reconciliation and error processing with the use of (i) match reports, (ii) automation in figuration process, and (iii) standing settlement instructions. • Custodians in the Settlement Phase resulting from (i) early notification of trades that will expedite credit and risk issues, (ii) use of alternative payment systems that eliminate physical cheque processing, and (iii) immobilization of shares eliminating physical processing of certificates. • The SIA is updating the T+1 Business Case and is expected to provide a more current analysis of the potential impact of STP/T+1 on operational costs. While we await the results of this update, if we conservatively expect that one-half of the net benefits from the original study will be realized, this translates to U.S. $1.35 billion in annual cost savings to the U.S. industry. • If we consider that the Canadian marketplace is roughly five per cent* of the size of the US, given similar assumptions, operational efficiency that the Canadian industry can conservatively realize is CDN $ 101.3 million (computed as US $1.35 billion * 5% *1.5). After excluding the benefit from a reduction in transaction correction costs of CDN $59 million (survey), the net benefit could be in the region of CDN $42.3 million. * See page 20 for assumption validation 8

Operational Risk and Financing Costs • During the survey, participants identified Operational Risk (see definition on page 20) and Financing Costs as areas where STP/T+1 will realize benefits to the Canadian industry. The survey had a short life cycle and did not include Operational Risk or Financing Costs within its scope. However, participants indicated the need to highlight these areas of benefit. • The Forrester Group, in its report The Real Benefits of T+1 (September 2001), estimated that STP/T+1 will reduce operations risk and financing cost in the U.S. marketplace by $2.4 million daily. Assumptions include: • Daily percentage of incorrect stock and bond trades of 1.0% and 2.5% respectively; • Daily U.S. stock and bond market volatility of 1.0% and 0.6% respectively (based on standard deviations of actual daily returns on the S&P 500 and 10-year Treasury from August 2000 to August 2001); • Daily stock and bond trade volumes of 20,000 and 1,000 respectively, with average stock trade to be 5,000 shares at $25 and the average bond trade $10 million; • Up to 0.25% of deliveries are delayed by one day and the financing rate is 4%. • If we assume the Canadian marketplace to be five pe cent* of the size of the U.S., and with similar assumptions, one conservative estimate of reduction in Operational Risk and Financing Cost in the Canadian industry is CDN $180,000 daily (computed as U.S. $2.4 million * 5% * 1.5). Extrapolated over 251 trading days (source: CDS), this translates to CDN $45 million. • Participants have indicated that Operational Risk requires attention since the Canadian market is relatively more volatile than the U.S. due to differences in industry composition. Also, with the revised Basle II Capital Accord, bank-owned operations, such as dealers, have an opportunity to reduce risk-based capital allocation requirements if operational risk reductions can be demonstrated. * See page 20 for assumption validation 9

Other Benefits • In addition to identified savings relating to transaction correction costs, participants identified the following additional areas where benefits may be realized: • Infrastructure Savings and Opportunities. • CDS expects the industry to benefit from the implementation of System X/CDSX, which will allow T+1 settlement . An initial estimate of the annual savings is in the region of CDN $5 million. This excludes any savings that could result within participant offices. • New Revenue Sources. • The Toronto Stock Exchange forecast approximately 20% of its data services growth or CDN $10 million in the next five years to come from more real-time data demand in an STP securities processing environment. • Generic Certificates. • Transfer agents identified the possible move to generic certificates to be an area where some benefit may be realized. Similarly, savings will also be realized by issuers. However, these benefits were not quantified. • Reduction in Default Risk. • While the survey did not include default risk (see definition on page 20) within its scope, participants indicated the need to highlight this area. Today, only 22% of the daily institutional trades of CDN $137 billion are reported to CDS by T+1 (Source: CDS). Even though principal risk may be minimal as settlement infrastructures insulate market participants from one another, the balance, 78% or CDN $106.9 billion, is exposed to some replacement cost risk. • TowerGroup estimates that about 4% to 5% of trades (in the U.S.) fail to settle on time. Reasons include: (i) Counterparty has no instructions; (ii) Counterparty has returned shares; (iii) Counterparty has not delivered shares; (iv) Clearing/principal broker incorrect; and (v) Counterparty short of shares. • With STP/T+1 initiatives (matching utilities, standards, etc.), the number of trades that fail due to the above reasons should substantially reduce. Even a 0.05 percentage point reduction in fail rates can reduce the replacement cost risk (default risk) by CDN $53 million (0.05% of CDN $106.9 billion), presenting the Canadian industry with some benefits. 10

Survey & Extrapolation Results: Broker/Dealers • Broker/dealers provided data on the following transaction correction elements: • Trade data not received electronically; • Trade data not received on a timely basis; • Trade data does not match with custodian; • Invalid trade. • Broker/dealers surveyed reported current annual trade volumes in the region of 0.88 million. To obtain results for the participant segment as a whole, the benefits were extrapolated using institutional trade statistics from CDS (5.77 million annual trades). This survey did not measure the benefit from the 28.1 million retail trades processed through CDS annually. Expected Percentage Reduction in Transactions that Require Intervention…. 12

Survey & Extrapolation Results: Investment Managers • Investment Managers provided data on the following transaction correction elements: • Cost of faxing data to the custodian; • Revisions to/cancellations of trade; • NOE/Confirms/Affirms not received electronically; • Missing or late NOE from broker; • Trade does not match with custodian; • Allocation instruction not sent electronically; • Allocation instruction do not match with broker; • Other issues. • Investment managers surveyed had CDN $144 billion under management. This represented 12.5% of the industry group as reported by Benefits Canada (Nov. 2001 edition). Expected Percentage Reduction in Transactions that Require Intervention…. 13

Survey & Extrapolation Results: Custodians • Custodians provided data on the following transaction correction elements: • Trade data not received electronically • Invalid trade • Trade data does not match with broker • Trade data not received on a timely basis. • Custodians surveyed reported current annual trade volumes in the region of 4.4 million, corresponding to 77% of the market. The results were extrapolated across 5.77 million trades (based on institutional trade statistics from CDS). CDS settled cross-border trades of 12 million and retail activity of 28.1 million were not included in the survey. Expected Percentage Reduction in Transactions that Require Intervention…. 14

Survey & Extrapolation Results: Other Participants Infrastructure Providers (Exchanges and Depositories) • The surveyed results were based on discussions held with representatives at the Toronto Stock Exchange, Bourse de Montréal and CDS. They excluded the impact of potential savings in the offices of the participants/clients of these organizations. Transfer Agents • Transfer agents provided data on the following elements: • Storage space for blank certificate inventory; • Cost of blank certificate inventory audit and control; • Cost of certificate issuance; • Participant deposits/withdrawals through System X; • Bank note certificate printing charges. • Infrastructure Providers and Transfer Agents expect minimal reductions (if any) in the percentage of transactions that require intervention and hence, the benefit to Transfer Agents is not expected to be significant. As noted, issuers are expected to benefit from the reduction in certificate holdings in favour of electronic and this is not reflected in the survey. 15

AppendicesParticipantsParticipant Assumptions and CaveatsBenefits Canada ExtractAssumption ValidationRisk Definitions Project Process and TimelinesModel Template by Industry SegmentSurvey Data Collection Sheets 16

Participants – Model Review and Summary • Transfer Agents • CIBC Mellon • Computershare • Pacific Corporate Trust • Exchanges and Depository • Toronto Stock Exchange • Montreal Exchange • CDS • Others • Investment Funds Institute of Canadfa (IFIC) • Investment Dealers Association of Canada (IDA) • FundSERV Inc • Security Transfer Association of Canada (STAC) • Custodian • CIBC Mellon Global Securities Services Co • RBC Global Services • State Street Trust Company Canada • Citibank Global Security Services • Northern Trust Company • Broker/Dealers • CIBC World Markets • Credit Suisse First Boston • BMO Nesbitt Burns • RBC DS • Investment Managers • Elliott & Page Ltd. • Ontario Teachers Pension Plan • Jones Heward Investment Counsel Inc. • AIM Funds Management Inc. • CDP Capital • Cundhill • OMERS 17

Participant Assumptions and Caveats • Survey participants and the CCMA have made the fundamental assumption that trade matching on T+1 or STP will be mandated and certain requirements will be enforced on the industry. (Canadian Securities Administrators to mandate STP/T+1 compliance). • To estimate potential future benefits, participants have assumed that the industry will have key infrastructure components in place. These include the Virtual Matching Utility, consistent reference data, the Canadian Depository for Securities Ltd. System X/CDSX for settlement (March 2003) and accepted industry standards and practices for securities processing. • Virtual Matching Utility connectivity will be mandated directly or indirectly (e.g., though mandating matching on trade date) and there will be enforced compliance. • The survey submission by individual survey participants will be kept confidential and only summarized results will be included in the final report. • As estimates were done on a best-efforts basis, actual benefits may vary. • Where no surveyed data or sufficiently strong assumptions could be made, estimates of savings should not be developed (although the potential for savings could be mentioned) to ensure that savings identified are conservative on an overall basis. 18

Assumption Validation Assumption 1: The Canadian market is roughly five per cent of the size of the US. • Market Capitalization. Based on 2001 statistics provided by The World Federation of Exchanges (www.world-exchanges.org), the market capitalization of NYSE, AMEX and NASDAQ was roughly USD 13.826 trillion and of the TSX was CDN 976 billion (USD 644 billion). The Canadian market capitalization as a percentage of the U.S. is roughly 5% (computed as USD 644 billion/USD 13,826 billion). • Securities on Deposit. Based on 2001 statistics provided by the U.S. Depository Trust and Clearing Corporation (DTCC) and CDS, the dollar value of securities on deposit at the depositories was USD 23.3 trillion and CDN 1.7 trillion (USD 1.1 trillion) respectively. Using this statistic, the Canadian market size as a percentage of the U.S. is roughly 5% (computed as USD 1.1/USD 23.3 trillion). Assumption 2: Retail trade volumes in Canada are in the region of 28.1 million annually. • As per statistics provided by CDS, total trading volume for 2001 was 45.8 million. • Of these, 33.8 million represented domestic trades and the balance, 12 million international (cross-border). • CDS also reported that domestic institutional trades were in the region of 5.77 million. • As a result, domestic retail trades are assumed to be 28.1 million (computed as 33.8 less 5.77 million). 20

Risk Definitions • Operational Risk: Potential loss resulting from incorrect trade entry due to inadequate or failed internal processes, systems, or human error or from external events. • Credit Risk: Cost of replacing trade when counterparty fails to deliver cash or securities according to the original contract terms of the transaction. • Principal Risk: Loss of principal when counterparty defaults after receiving irrevocable delivery of one side of the trade. • Default Risk: For the purposes of this document, defined as the risk of an insolvent counterparty being unable to complete the transaction, and the related cost to replace the transaction at prevailing market price. Also know as “replacement cost risk”. • Settlement Risk: Principal and replacement cost risk plus liquidity risk; the risk that an obligation will not settle when due. 21

Project Process and Timelines April 26 April 27 May 2 June 5 June 7 June14 Custodians Identify Value Proposition with participants Create spreadsheet and validate Participants met to revalidate model Participant’s populate model Compile data from participants Validate completed data with stakeholders Analyze and extrapolate May 6 May 7 May 13 June 19 June 21 June 24 Identify Value Proposition with participants Create spreadsheet and validate Participant’s populate model Compile data from participants Validate completed data with stakeholders Analyze and extrapolate Participants met to revalidate model Broker/dealer May 13 May 14 May 21 June 14 June 18 June21 Identify Value Proposition with participants Validate completed data with stakeholders Investment Managers Create spreadsheet and validate Participant’s populate model Compile data from participants Analyze and extrapolate Participants will meet to revalidate model June 7 May31 June 6 June 14 May 31 Participant’s populate model Compile data from participants Validate completed data with stakeholders Analyze and extrapolate Exchanges Create spreadsheet and validate Identify Value Proposition with participants May 17 May 17 May 31 June 3 June 14 Identify Value Proposition with participants Create spreadsheet and validate Participant’s populate model Compile data from participants Validate completed data with stakeholders Analyze and extrapolate Transfer Agents May 23 June 13 June 14 June 24 June 21 June 13 June 28 Add Custodian Section Present draft to CCMA and decide next steps Add Investment Managers Section Industry Summary Interim Report Add Broker/Dealer Section Add Exchanges and Transfer Agents Brain storm final deliverable format 22