Contract Types

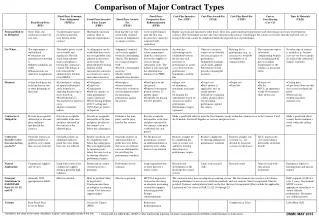

Contract Types. While there appears to be many types of contracts, all can be placed in one of two “families” Fixed-price Cost reimbursement. Contract Types. A few contract types have characteristics of both “families” Fixed-price characteristics

Contract Types

E N D

Presentation Transcript

Contract Types • While there appears to be many types of contracts, all can be placed in one of two “families” • Fixed-price • Cost reimbursement

Contract Types • A few contract types have characteristics of both “families” • Fixed-price characteristics • Detailed specification or other detailed description • Performance regardless of cost • Little contract administration on the part of gov’t • Much contract administration on the part of the contractor • Cost reimbursement characteristics • A less detailed description of the work • Best efforts on the part of the contractor • Greater contract administration on the part of the gov’t

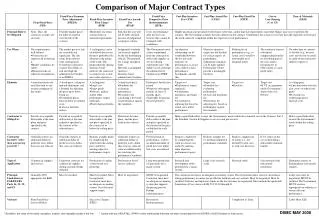

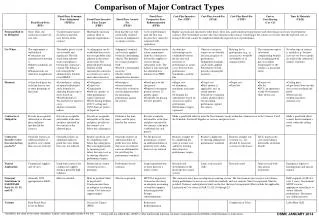

Contract Types The Real Differences Fixed Price Cost Reimbursement Work Requirements Measured exactly to WS Best Efforts Default Termination No Cost/no profit Cost/no fee Convenience Termination All cost/partial profit all cost/partial fee Change Orders Contractor risk ceiling protection Gov’t Property Contractor risk of loss gov’t risk of loss

Contract Types • Firm-Fixed Price • Once price is set it doesn’t change unless there is a contract change • Proposals sometimes identify cost and profit separately • Or in highly competitive situations it may just identify a price • However, even when cost and profit are negotiated separately, the contract just identifies a price • The detailed requirements of the SOW or specifications are used to accept or reject the item or service

Contract Types • Fixed Price – Redeterminable • The contract could be Firm Fixed Price (FFP) except for • One or more areas that could significantly change • Example – labor rates, product components, cost of materials • The contract provides for adjustments, up or down, if certain specified events occur

Contract Types • Fixed Price Incentive • Price is fixed like FFP • But contract shows cost and profit separately • Profit varies upward or downward with cost outcome to specified limits

Contract Types • Cost Reimbursement • Cost Only • Appropriate in circumstances where the contractor has a mutual interest in the work • No fee is provided • Example, contracts with universities, state and local gov’t, non-profits • Cost Sharing • Same circumstances as cost only but the contractor’s level of interest in the work is so high that they will assume part of the cost • Commercial entity has an expectation of receiving substantial benefits • Example, R&D may result in products or processes with broad applicability and significant commercial potential

Contract Types • Cost Plus Fixed Fee • Most common type • Fee is mixed at the beginning but cost may be adjusted up or down • Fee is fixed regardless of the cost outcome • Cost Plus Award Fee • Often used where work is on a gov’t site • The gov’t evaluators are in a position to evaluate contractor performance on a regular basis • There may be a base fee • The award fee is earned based on performance

Contract Types • Cost Plus Percentage of Cost • Prohibited – illegal form of contract • Why illegal – fee is paid as a percent – no incentive to economize

Contract Types • Mixed Contracts • Letter Contract • Used in urgent situations • A “letter” type direction to proceed immediately • But there are often limitations on detail • The FAR encourages negotiations of as many definite provisions as possible before issuance • Requires “definitization” in accordance with a strict schedule

Contract Types • Time and Materials and Labor Hour • Used primarily in a repair situations • Labor is on a Fixed Price Loaded Labor Rate basis • Material is on a cost plus handling charge basis • The contract contains a cap • Labor hour arrangement does not involve materials

Contract Types • Indefinite Delivery/Indefinite Quantity • Contains all the provisions of a contract except the details on specific orders • Contains a minimum guarantee which is usually a few thousand dollars to 5% to 10% of the estimated annual work • Sometimes are awarded to multiple contractors and their orders are competed among those contractors • The “type” of orders may vary – some may be FFP, labor hour/time and materials or Cost Plus Fixed Fee • If varying type orders are allowed, the contract should contain clauses covering the different types

Contract Types • Requirement Type Contracts • Could be the same as IDIQ but there is no money guarantee • The guarantee is that there will only be one contract awarded for the covered commodity or service by the agency – if there are any orders they will go to the contractor awarded the requirements contract

Financial • Basic Financial Goals of All types of Business • Make or offer a saleable product or service • Control costs to be price competitive • Keep cask flowing to assist in controlling costs • Make as much profit as possible

Financial • Financial Team Players • Financial Manager – sometimes known as the CFO • Comptroller – could be same as CFO in small companies • Treasurer • Auditors – internal and external • Government Players • The Procurement Contracting Officer – negotiates original contract and primary changes • Administrative CO – conducts systems reviews including finance, sets billing and overhead rates and approves invoices • Program Manager – agrees on quantities and changes and approves invoices • Auditor – conducts financial reviews for the CO

Financial • CAS – Cost Accounting Standards Board • 1970 Congress created – to implement standards that would achieve uniformity and consistency in the cost accounting practices and reporting of costs under negotiated different prime and sub contracts • CAS applies to contracts over $500,000 • Exceptions to CAS • Contracts under 500K • Sealed bid contracts • Contracts w/ small business and foreign gov't • Contracts where price is set by law • Contracts and subcontracts performed entirely outside the US • FFP contract award on basis of adequate price competition

Financial • Also, may be waived for a particular prime contract (or sub contract) under $15 million if the head of the contracting agency determines, in writing, that the performing business is • Engaged in the sale of commercial items and • Would not be subject to CAS other than size of contract

Financial • Contractor Obligations under CAS • Disclose in writing the cost accounting practices by completing a disclosure statement • Follow the disclosed practices consistently in estimating and reporting costs • Comply with CAS in effect at the time of award • Agree to price adjustment in the event gov’t shows contractor failed to comply w/ existing CAS or its own approved practices

Financial • Costing Principals • Are used when cost analysis is required • When negotiating a fixed price contract – used a guide in both the pricing and any subsequent changes • They apply to proposals and cost incurred after award for cost reimbursement arrangements • For post award incurred cost, they only apply to Cost Reimbursement situations • Cost reimbursement does not mean that a contractor will be reimbursed all of their costs • Do be reimbursed a cost must be “allowable”

Financial • Costing Principles • To be allowable - FAR 31.201-2 requires that a cost must be • Reasonable – (vague) prudent person in the conduct of competitive business • Allocable – if it chargeable, and if it is incurred specifically for the K or benefits K and other work (make a pro-rata distribution) • Meet accounting standards or generally accepted accounting principles • Meet terms of contract • Meet FAR principles

Financial • Reasonable means • In nature and amount it’s reasonable • It is the type cost that a prudent person would have incurred in the conduct of competitive business • Allocable means • The cost was incurred specifically for the contract (direct), or • That the cost benefits both the contract and other work and can be reasonably • That the cost is necessary for overall business operation (G&A) • Meets accounting standards means • It meets established CAS, or • It meets generally acceptable principles recognized in the industry

Financial • Meets the terms of the contract means • It meets any special provisions on the contract • These provisions cannot violate cost principles • Examples of some provisions: • Special treatment for the project • Pre-contract costs included • Meets FAR Principles means • It does not violate FAR part 31 • FAR part 31 identifies 53 types of costs and provides guidelines for their acceptability (outlined in the text) • Unallowables • Contractors must account for • Fee or profit pays for unallowables

Financial • Some Selected Costs • Many public relation and most advertising – generally non-allowable but selling costs are allowable • Allowable PR costs – trade shows, public communication, stockholder communication, general news/media liaison, community event support • Interest – non-allowable • Bad debts – non-allowable • Compensation for personal services • CAS has guidance for all types of compensation • Executive compensation is a ‘hot’ issue • Severance pay is also an issue covered • Salary surveys are conducted within the commercial sector to determine reasonableness

Financial • Some Selected Costs • Employee morale – health and welfare – allowable • Examples • Employer/employee relations • Crisis consultation • Health clinics • Employee publication • Dining rooms • Recreation facilities • Picnics/parties • Awards\ • Entertainment costs – unallowable

Financial • Some Selected Costs • Pre-contract costs • Costs incurred before effective date of contract • Allowable to extent they would have been allowable after award • If necessary to meet delivery schedule • Good idea to get letter of agreement • Costs of fines, penalties and mischarging – generally unallowable • Losses on other contracts – generally unallowable • Training, education, trade, business, technical and professional activity costs - generally allowable

Financial • Payment Withholding • Payments on CR contracts may be withheld for many reasons • Failure to make progress on contract • Labor standards violation • Contract violation • Payments withheld for unallowable costs • Withholding payment can either involve suspension or disallowance • Suspension = temporary withholding pending a final determination • The ACO, PCO or in some cases, auditor can suspend payments or disallow costs • If auditor, then ACO makes a final decision on disputed issues

Financial • Important Contract Administration Functions • Establishes labor rates and material estimates to be used in proposals • Establishes company overhead (OH) and general and administrative (G&A) rates • Develops cost reports for project managers • Assures cash flow • Obtains money to run projects

Financial • Cash Flow Analyses • When are payments of bills due and how much • Labor • Materials • Rent • Utilities • Installment/loan payments • When is income scheduled to come in • How will income be used to pay bills • Financing necessary?

Financial • Labor Rate Composites • Example – the contract may have 3 fixed price labor categories Engineer $75 p/h 5000 max. hours Technician $45 8000 Analyst $60 10000 How does the Finance Manager calculate – justify the calculations

Financial • Overhead Rate Development • Direct cost of unit • Sales of unit • Overhead pool expenses • Example • Product direct cost per unit $1.00 • Estimated annual sales (units) 100,000 • Direct cost of product $100,000 • Estimated annual overhead cost $100,000 • Overhead to be applied to each unit 100% • Total cost of each unit $2.00 • Add profit (assume 10%) .20 • Unit selling price $2.20

Financial • How much money is needed? • Fixed –Price Contracts • Payment upon acceptable delivery is normal rule • But progress payments are possible • Delivery may be broken into segments with payment schedule • May be able to get advance on contract (rare) • Cost Reimbursement Contracts • Periodic payments every 2 weeks or once a month possible • But payment delays may occur after approval of invoices • Advance available

Financial • Truth in Negotiation Act (TINA) 1962 • Applies to negotiated contracts or modifications with a value of $550,000 or more. • Exempted from TINA if there is adequate price competition, procurement of commercial items or service, or price set by law or waiver from requirements • Requires certification of cost or pricing data (by prime contractors and sub-contractors) • Cost or pricing data is defined as • All facts • Existing at the date of the agreement of price • That are significant to price negotiations

Financial • TINA • Certification requires that data must be • Accurate • Current • Complete • Use standard forms 1411 and 1448 • Data is information that is • Factual, historical – not estimates • FASA amended TINA – • raised the threshold from $500K to $550K • Made exceptions to TINA mandatory • Broadened exemption categories • Created commercial item exception

Financial • TINA • Certification is as of the date of the agreement • All info to be submitted before award is made • Contract clause provides for defective price audit – FP or CR (both) • If defective pricing is found – remedies • Repayment of excess • Interest on excess • Penalty • Criminal prosecution if fraud (disbarment/suspension) • Subcontractor • Sub should certify to prime • Prime certifies to government • No privity of contract between sub and gov’t • Always in a prime contract with a sub – have provision that sub will make prime whole in the case of defective pricing

Fraud & Ethics • Civil Fraud • False Claims Act – allows recover of damages/penalties from anyone who submits a false claim to a federal agency • Knowingly presents or causes to be presented to the gov’t a false/fraudulent claim for payment or approval • Uses a false record or statement to get claim paid/approved • Conspires to defraud gov’t by getting a false claim paid/approved • Knowingly uses a false record/statement to conceal; avoid or decrease an obligation to pay or transmit money or property to gov’t

Fraud & Ethics • False Claims Act • Burden of Proof – on gov’t by a preponderance of the evidence • Knowledge = actual knowledge or “deliberate ignorance” • Innocent mistakes/negligence (even gross negligence) not enough for a conviction • “Qui Tam” whistleblower provision of law – fixed by 1986 amendment to False Claims Act • Made it more attractive • Especially in areas of Medicare/Medicaid – • Syracuse example

Fraud & Ethics • “Qui Tam” • Exceptions • Suits between members of military and gov’t • Suits based on info known to gov’t • Suits based on allegations that are subject of a civil suit to which gov’t is a party

Fraud & Ethics • False Statements Act • Widely used in prosecuting criminal fraud cases • Supreme Court – has repeatedly stated that statute should be “broadly and liberally” interpreted • Practical effect – gov’t may use this statute, even where a more narrowly defined and more specific statute could be applied. • Conviction requires a showing of • A statement was made • The statement made was false • The person making the statement knew it to be false when the statement was made • Statement was material • Statement concerned a matter w/in federal jurisdiction

Fraud & Ethics • Major Fraud Act of 1988 • Covers Gov’t prime contracts over $1,000,000 • Subcontractors are also subject to statute • Contains whistleblower protection and rewards

Fraud & Ethics Government Corruption • Anti-Kick Back Act – 1986 • Covers prohibited conduct – forbids any individual or business from • Providing/attempting to provide any kickbacks • Soliciting or accepting (or attempting to accept) a kickback • Includes the amount of any kickback that may be in the price charged by a subcontractor to a prime contractor (or a higher tier subcontractor) in the price charged by the prime to the Gov’t • Kick-back is defined as: money/fee/commission/credit/gift/gratuity/thing of value or compensation of any kind (directly or indirectly) for the purpose of improperly obtaining or rewarding favorable treatment in connection w/ a government contract • Applies to all government contracts

Fraud & Ethics • Procurement Integrity Act – 1996 (as amended) • Conflicts of interest • Improper disclosures and • Receipt of procurement information • Restricts acceptance of employment by former agency officials with gov’t contractors and employment contracts/consultants for procurements over $10 million for one year • Loophole – no restriction on working for another division or affiliate of the contractor • “designed to restore public confidence in gov’t procurement process”

Fraud & Ethics Procurement Integrity Act • Also prohibits current and former federal official from “knowingly disclosing or knowingly obtaining” contractor bid or proposal information before the award of a contract, to which info relates to, is awarded • Example – cost/pricing data, indirect costs, labor costs, trade secrets, other proprietary information

Fraud & Ethics Lobbying Restrictions • Byrd Amendment – gov’t-wide restrictions on contractors use of federally appropriated funds for legislative and executive branch lobbying (looking to deal with improper influence peddling?!) • Lobbying Disclosure Act – 1995 • Created more gov’t employees by creating a comprehensive scheme for reporting and registering lobbyists

Fraud & Ethics Suspension & Debarment • May preclude contractor from getting contracts for up to 3 years • FAR procedure - suspension • Notice to contractor – stating when suspension will take effect/cause • Contractor has 30 days to submit information in opposition but no right to a pre-suspension hearing • May obtain a post-suspension fact-finding hearing based on the strength of submission • Debarment • Right to a detailed statement of reasons for proposed debarment • 30 days to respond

Fraud & Ethics • Protests – contents • Must be signed by the protestor or legally authorized agent and addressed to GAO • Protestor’s – name/address/phone and fax numbers • Name of contracting agency and solicitation # • A detailed statement of the legal factual grounds of protest • Copies of relevant documents • All info establishing that protestor is an interested party and protest is timely • Request for a ruling by GAO • Statement of relief requested • Example – protective order, hearing, specific documents • GAO – decision issued w/in 100 days