Download

1 / 29

290 likes | 301 Vues

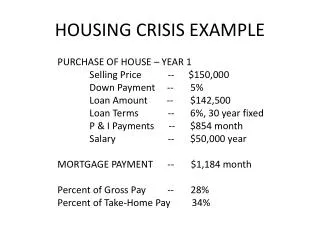

Housing Markets in Italy after the crisis Uberto Visconti di Massino ERES 2010, June the 25 th , 2010. Agenda. the Real Cycle and residential values The PAST The PRESENT The FUTURE The FUTURE 2: a great potential. the Real Cycle and residential values. Theory & practice. The PAST.

E N D

Housing Markets in Italy after the crisis Uberto Visconti di Massino ERES 2010, June the 25th, 2010

Agenda the Real Cycle and residential values The PAST The PRESENT The FUTURE The FUTURE 2: a great potential

Past cycles in Italy III VI II I Source Scenari Immobiliari - Italy

(residential) Overview of the past (repeating itself?)

A market going crazy…. The Honeycomb cycle (Residential property in Lombardy) Source: data processing by Reddy’s Group spa on dataCensis, Agenzia del Territorio - Servizio Statistiche Giudiziarie

..... after 3 years Overview of some current indicators • N° sales • from 200 to 2007 province 67 to 72% / capitals 33 to 28%) • The shift towards deurbanization was due to • Moving out to buy a better, cheaper home • New stock available outside, + gardens! • 2009: there had been 600k sales: - 15,6% national level (I sem 2009 on I sem 2008) • … of which – 12% on capital cities / -17% in province • The “back to town” shift province to capitals due to • Difficulties in commuting • Lower periphery prices Vs province prices

..... after 3 years Overview of some current indicators • € - prices • from 2000 to 2007 prices increasing, then decreasing: • National level: – 6,3% (2009/2008) • End 2008 on I sem 2008: -3,6% • I sem 2009 on II sem 2008: -2,7% (decline reducing?) • Focus on cities: • Milan and Florence better than average • lower prices in cities due to inelasticity of new built (province) • Peripheries versus city centers • peripheries loosing more in value: lower quality homes • Less immigrants demand for old homes (in peripher.)

Overlook, a correlation Italian GDP and constructons. Euroconstruct onCresme et Al. - Dec 2008

The Italian market (residential) Overview • In general, Demand wise we can have three scenarios. The refer to the economic forecasts : • if UPSIDE, then ALL TARGETS (residential) will recover in 2010 • if BASE scenario: in 2010 we will have only the “NEED TO BUY” “NEED TO RENT” ones active in the market, and in 2011 ALL TARGETS • if DOWNTURN, we will have NEED TO BUY in 2011 and ALL TARGETS active in 2012. (NEED TO BUY= have savings and need more space, more rooms (consolidated families whose children are growing) NO BUY: those who can only rent (young couples, no children), professionals singles, senior couples (still using their old home, empty nesters)

The market cycle in the current setting : forecasts Fonte: nostra elaborazione su fonti varie tra cui Scenari Immobiliari, Banca d’Italia.

Whare are we now? Table 1, Rents : popular (ERP, 1 e 2), sustainable (ERS, in the box, 3 -4), and “free” market Source: our calculatios on : ACER, Fondazione Cariplo, Co-Housing Venture, Scenari Immobiliari

THE FUTURE 2 What next? “Sustainable” homes (social housing – Edilizia Privata Sociale) in Italy

A shift in the residential mindset • From 100 B.C. to 1800 • Brick and mortars (the roman “insula” to the condo.) • In 1900 the first revolution • Electricity – hydraulics • 2006 – 2020 the second revolution • Energy saving and sustainability • In 2011 the third revolution • The ethic side, management and common services. • Institutional investors

S.H.- What is it? Some cases Social Housing 360° - arch. LAURA ROCCA Fonte: RoccAtelier (www.roccatelier.it) E.R.S. a Crema, Fondazione Cariplo, Fondo Abitare Sociale - architetti D2U Fonte: Jacopo della Fontana (www.d2u.it)

S.H.- What is it? Some cases Social Main Street – Bicocca, Milano- arch. DANTE BENINI Fonte: studio Urbam – C.d.O. Concorso Figino (Fond Cariplo) arch. CINO ZUCCHI e Avventura Urbana Fonte: www.avventuraurbana.it

Some models to learn from : Social Housing in the Netherlands

GRAZIE - THANK YOU ! Uberto Visconti di Massino Milano Corso Italia, 17 20122 Milano Tel. 02 00621170 Fax. 02 00621189 Roma Via XX Settembre, 1 00187 RomaTel. 06 42020939Fax. 06 42020951 www.epf.it epf@epf.it