Download

1 / 11

590 likes | 2.71k Vues

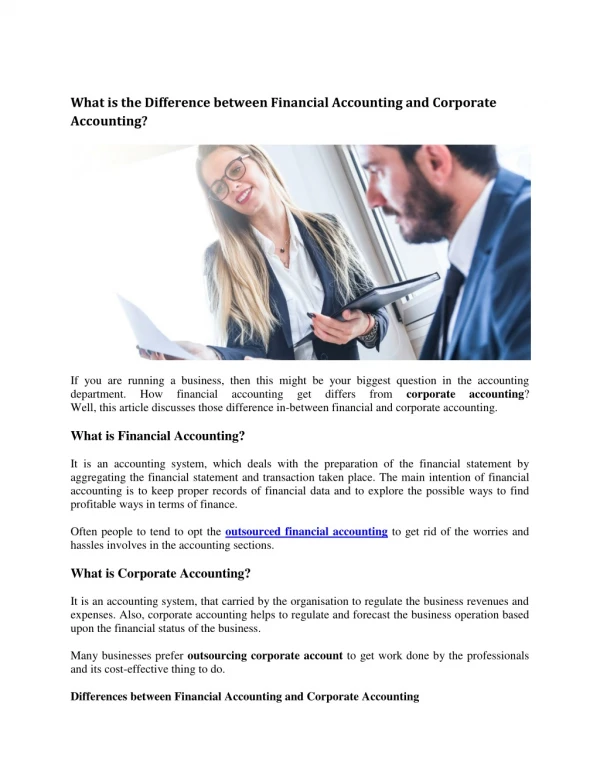

Corporate Accounting. PRESENTED BY PROF.S.N.MURUGANANTHAM. Corporate Accounting Meaning.

E N D

Corporate Accounting PRESENTED BY PROF.S.N.MURUGANANTHAM

Corporate Accounting Meaning Corporate Accounting is a special branch of accounting which deals with the accounting for companies ,preparation of their final accounts and cash flow statements, analysis and interpretation of companies's financial results and accounting for specific events like amalgamation, absorption, preparation of consolidated balance sheets.

Definition: A corporation is a legal form of business that is separate from its owners. In other words, it’s a business that is a separate legal entity from its shareholders.

What are Some of the Advantages or Disadvantages of Forming a Corporation? • Advantages • Generally, a corporation's shareholders are not liable for any debts incurred or judgments handed down against the corporation. Shareholders only risk their equity in the corporation. • Corporations may be able raise additional funds by selling shares in the corporation.

Corporations may deduct the cost of benefits it provides to employees and officers. • Some corporations may be able to elect treatment as an S corporation, which exempts them from federal income tax other than tax on certain capital gains and passive income.

Disadvantages • Forming a corporation requires more time and money than forming other business structures. • Governmental agencies monitor corporations, which may result in added paperwork. • Corporate profits may be subject to higher overall taxes since the government taxes profits at the corporate level and again at the individual level, if such profits are distributed to the shareholders. Furthermore, a corporation may not deduce from its business income any dividends it pays to its shareholders.

Share types 1. Ordinaryshares are the most common type of shares and are standard shares with no special rights or restrictions. They have the potential to give the highest financial gains, but also have the highest risk. Ordinary shareholders are entitled to voting rights, however, they are the last to be paid if the company is wound up. 2. Non-voting ordinary shares carry the same conditions as ordinary shares except with regards to voting rights. Shareholders may have voting rights under certain circumstances or they may have no voting rights at all.

3. Preference shares typically carry a right that gives the holder preferential treatment when annual dividends are distributed to shareholders. Shares in this category receive a fixed dividend, which means that a shareholder would not benefit from an increase in the business' profits. However, usually they have rights to their dividend ahead of ordinary shareholders if the business is in trouble. Preference shares carry no voting rights.

4. Cumulative preferenceshares give holders the right that, if a dividend cannot be paid one year, it will be carried forward to successive years. Dividends on cumulative preference shares must be paid, despite the earning levels of the business, provided the company has profits that can be distributed.

5. Redeemableshares come with an agreement that the company can buy them back at a future date - this can be at a fixed date or at the choice of the business. A company cannot issue only redeemable shares, so they must ensure that they also issue non-reedeemable shares.