Download

1 / 7

70 likes | 87 Vues

Learn how to record and adjust accrued revenue and interest income entries in accounting, including calculating accrued interest, journalizing entries, and posting to ledgers. Understand reversing entries and collecting notes receivable from previous fiscal periods. Review terms and examples.

E N D

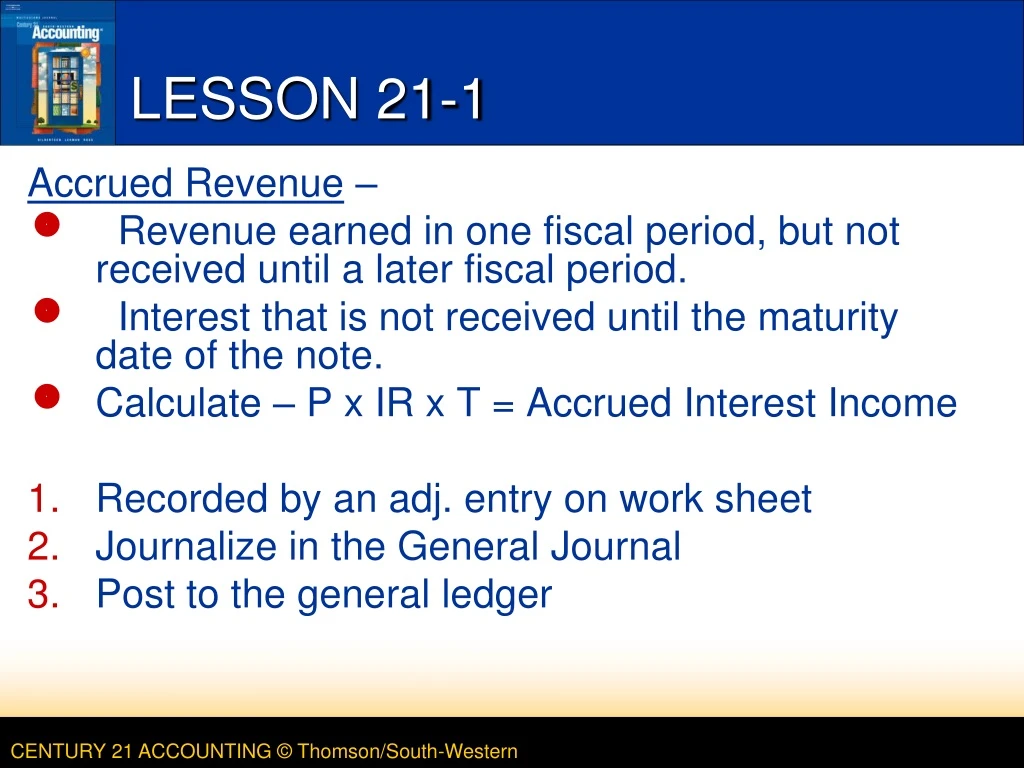

LESSON 21-1 Accrued Revenue – Revenue earned in one fiscal period, but not received until a later fiscal period. Interest that is not received until the maturity date of the note. Calculate – P x IR x T = Accrued Interest Income Recorded by an adj. entry on work sheet Journalize in the General Journal Post to the general ledger

3 ANALYZING AN ADJUSTMENT FOR ACCRUED INTEREST INCOME page 617 1 2 1. Debit Interest Receivable. 2. Credit Interest Income. 3. Record the adjusting entry. LESSON 21-1

1 2 POSTING AN ADJUSTING ENTRY FOR ACCRUED INTEREST INCOME page 618 1. Post the debit. 2. Post the credit. LESSON 21-1

REVERSING ENTRY FOR ACCRUED INTEREST INCOME page 619 1 2 3 • Reversing entry – made at the beginning of a new fiscal period. • Opposite of adjusting entry. • Reduces the balance of Interest Receivable to zero. 1. Write the heading. 2. Debit Interest Income. 3. Credit Interest Receivable. LESSON 21-1

4 4 COLLECTING A NOTE RECEIVABLE ISSUED IN A PREVIOUS FISCAL PERIOD page 620 January 30. Received cash for the maturity value of a 90-day, 6% note: principal, $2,000.00, plus interest, $30.00; total, $2,030.00. Receipt No. 9. 1 3 2 1. Credit for the principal of the note. 2. Credit for the total interest. 3. Debit for the maturity value. 4. Post the amounts in the General columns. LESSON 21-1

TERMS REVIEW page 621 • accrued revenue • intellectual property • accrued interest income • reversing entry • CLOSING ENTRY - closing interest income for the fiscal period. Completed BEFORE reversing entry. • Debit – Interest Income (balance in the ledger after posting of adjusting entry) • Credit – Income Summary LESSON 21-1

Why do we accrue revenue? • Examples: • Bank Loan • Construction Company Example LESSON 21-1