Download

1 / 85

850 likes | 867 Vues

This presentation provides an overview of captive insurance, highlighting the benefits of using captive insurance companies. It also discusses the use of group captives, premium and loss funding, financial reports, and the Cayman Islands as a popular captive domicile.

E N D

Captive Insurance Overview Society of Risk Management Consultants April 2013

Today’s Presentation • Captive World Summary • Grand Cayman Overview • Captive Resources / Our World • Group Captives / Structure • Premium / Loss Funding • Financial Reports • Captive Investors Fund • 831B Micro Captive • Well Health Group Captive

Captive Insurance World • Over 55 Billion in Premiums • Over 5000 Captives Worldwide • Almost 50 % based in Vermont, Bermuda, and Grand Cayman • More than 30 States set up as Domiciles • Most Fortune 1000 and many Middle Market Companies are using them

Captive Insurance Companies 17.6%$59.7B Self-Insured Program29.4%$92.3B Risk Retention Groups,Pools & Trust 3.6%$10.9B TraditionalMarket 49.4% Alternative Market – 2011 Premium Estimates Alternatives exceed 50% of the market Source: A.M. Best Co.

Single Parent Group CaptiveHomogeneous Rent-a-Captive Group CaptiveHeterogeneous Agency Captive Types of Captives

Group Captives - Homogeneous Industry Specific Normally More Difficult Industry Classes Risk Management Programs Tailored To The Class Of Business Unrelated Companies Sharing Risk If Structured Correctly Meets All IRS Guidelines For Tax Deductibility

Group Captives - Heterogeneous Multiple Industries In The Same Captive Five Of The Top Ten Group Captives Geographic And Industry Class Spread Of Risk Usually Lower Operating Costs Individual Members Actuarially Priced Greater Leverage In The Market Due To Size

Reasons to Investigate Captives • Captives are interested in Best of Class accounts • Captives Mitigate the swings in the insurance market • Gain Control of the insurance process. • Gain greater Leverage in the insurance marketplace • GreaterIncentive to manage the loss control and claims programs

Captives allow for Predictability of premiums and operating costs: • Actuarially calculated loss sensitive premiums. • Aggregate stop loss can be provided to define maximum liability. • Exposure to specific excess losses shifted to reinsurance companies.

The Cayman Islands • Group of 3 islands in the western Caribbean • British Overseas Territory • Locally elected Legislative Assembly • Legal system based on English common law • Population approximately 55,000 • Economy based on diverse finance industry and tourism

300 banks, including 40 of the world’s top 50 8,500 + Mutual Funds 728 Insurance Companies Shipping Registry Stock Exchange The Cayman Finance Industry World’s 5th largest financial centre Home to:

The Cayman Islands as a Captive Domicile • Over 35 years experience with captives • 2nd largest captive domicile, writing premium of $12B & holding assets of $70B • Well developed infrastructure • Accessible & business-focused regulators • Compliance with international standards • Straightforward incorporation/licensing process • 20 year exemption from any local taxes • No requirement for local directors or attorneys

Captive Resources LLC 25 + years in existence. 27 member owned group captives. 5 of the top ten largest member owned alternative risk facilities (Business Insurance) Developed one of the first member owned group Benefits Captive Approaching $1,200,000,000 in premium. Nearly 2,500 member companies. Created and Oversee $1,700,000,000 Cayman Islands Mutual Fund (established in 1994) CIF. 100 employees in Schaumburg, IL. Sister company, Kensington Management, largest independent captive manager in the Cayman Islands. Who We Are

An Overview of Captive Management in the Cayman Islands

Role of the Insurance Manager • Licensing and incorporation of captive • Ensure regulatory compliance • Day to day management of the captive • Preparation of financial statements & reports • Liaison with auditors and tax advisors • Provision of Registered Office and Corporate Secretarial function

Profile of Kensington • Sister company to Captive Resources LLC. • Licensed in 1999 • 30+ captives managed, representing over 2,500 insured entities and over $1,000,000 million in premium, including 13 of top 20 group captives globally • Largest independent manager (premium) • 24 staff, including 14 chartered accountants • Team structure • Audited by & fully compliant with Cayman Islands Monetary Authority (“CIMA”) requirements

Raffles Overview • Largest Heterogeneous Group Captive • 100% Owned by Policyholders • Incorporated in 1984 • Domiciled in Cayman • Geographic Spread is National • 322 Member Companies • Returned More Than $200,000,000 of Dividends to Members to Date • Premiums exceeding $205,000,000

Control Your Losses!!! Work With Your Loss Prevention Consultant! Attend Risk Control Workshops! Be Aggressive/Participate In Claim Reviews! Member Expectations Attend and Participate at Board Meetings Refer New Members

Premium $ Why Are Your Costs Lower?Recapturing Previously Lost Dollars • Premiums based on your loss experience • Insulated from market conditions • Operating costs are lower • Only good risks are accepted • Enhanced loss prevention and claims management • Return of unused loss funds and investment income

Statutory Umbrella Excess $1,000,000 Statutory Workers Comp. GeneralLiability Auto $500,000 Basket & Clash Coverage Included Captive Retention Specific Excess Insurance

Experience Adjustment Aggregate Excess Insurance Loss Fund How Is the Captive Protected?

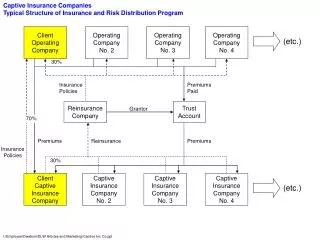

Insured Profits Marsh, Inc. Zurich N. America Raffles Insurance, Ltd. Axis Reinsurance Zurich Claims Administration Gallagher Bassett Claimant Captive Flow

Risk Control Services • Services Provided • Safety –assessment completed on all members/prospects • Claims –Special claims handling instructions • Risk Control Workshops • Webinars • Web-Based Safety Training • Quality Assurance • Group Purchasing Programs • Watchlist and Awards • Member Report Card at September Meeting

Risk Control Workshops • Requested topics • Member Presentations • Speaker variety • Breakout sessions • Networking • National Workshops (Risk Management, Owners, CFOs, Safety Staff) • Regional Workshops (Front Line Supervisors) Next National Workshops: October 22-24, 2012 Orlando, FL w/NSC April 29 – May 1, 2013 Phoenix, Arizona

Risk Control Workshops (continued) Regional Workshops: Date Location • May 23 Harrisburg, PA • May 24 Lancaster, PA • May 25 York, PA • June 6 Captive Resources, Schaumburg, IL • June 7 Raleigh, NC • June 28 Shreveport, LA • August 6 Newport Beach, CA • August 8 Sacramento, CA

2012 Webinars - The Third Tuesday of Each Month at 10AM & 2PM DateSubject Jan 17 OSHA Update/Recordkeeping Review Feb 21 Accident Investigation Best Practices Mar 20 Getting the most out of your loss control dollar! Apr 17 Hazard Communication (HazCom) and The Globally Harmonized System of Classification and Labeling of Chemicals. May 15 What can we do about accident repeaters? Jun 19 Warehouse Safety/Racking Safety Jul 17 Behavior Based Safety Basics Aug 21 Slip/Fall Prevention Sep 18 Use of Social Media in Risk Control Oct 16 Back Injury Prevention Best Practices Nov 20 Transitional Duty/Return-to-work Best Practices Dec 18 Safety Accountability Ideas

Quality Assurance • Web-based Surveys • Claims Management • Loss Prevention Consultant • Workshop Evaluations • Consultant Follow-up

Consultant Captive Resources, LLC Insurance Manager Kensington Management Group Audit Firm PricewaterhouseCoopers Financial Institution RBC - Cayman Actuarial Firm Pinnacle Actuarial Res. Tax Firm Ernst & Young Independent Financial Analyst John Brown Financial Service Providers

Operating Costs: $230,000 Premium: $700,000 AROs : $ 0 Total Pay-In: $700,000 Sample Member Loss Forecast: $470,000

Reinsurance $500,000 $50,000 CFund $300,000 BFund (Captive Shock Loss Layer) $70,000 $125,000 AFund (Captive Frequency Loss Layer) $350,000 Sample Member Premium distribution into funds: Loss forecast = $470,000

a typical year The Power of Group Captives

Reinsurance C Fund Accounting $500,000 CFund B Fund Accounting $300,000 BFund A Fund Accounting $125,000 AFund Loss Example #1 $210,000 of total claims less than $125,000 $50,000 Beginning balance $70,000 Beginning balance $350,000 Beginning balance • 210,000(Total claims less than $125,000) • $140,000 Remaining balance

“Typical Year” Results $140,000 A Fund Balance $ 40,000 Investment Income Remaining B Fund Balance Remaining C Fund Balance

catastrophic claim year The Power of Group Captives

Reinsurance $500,000 CFund $300,000 BFund $125,000 AFund Loss Example #2 $210,000 of total claims less than $125,000 and a $1,000,000 catastrophe claim C Fund Accounting $50,000 Beginning balance B Fund Accounting $70,000 Beginning balance A Fund Accounting $350,000 Beginning balance - 210,000 Total claims less than $125,000 - 125,000 1st $125,000 catastrophe loss $15,000Remaining balance

Reinsurance $500,000 - 1,000Pro- rata contribution CFund $49,000Balance $300,000 BFund $125,000 AFund Loss Example #2 $210,000 of total claims less than $125,000 and a $1,000,000 catastrophe claim C Fund Accounting $50,000 Beginning balance B Fund Accounting $70,000 Beginning balance A Fund Accounting $350,000 Beginning balance - 210,000 Total claims less than $125,000 - 125,000 1st $125,000 catastrophe loss $15,000Remaining balance

Reinsurance $500,000 $50,000 Beginning balance - 1,000Pro- rata contribution CFund Catastrophe Claim: $49,000Balance $175,000 - 70,000 $ 105,000 $300,000 BFund - 70,000 $0Balance $125,000 AFund Loss Example #2 $210,000 of total claims less than $125,000 and a $1,000,000 catastrophe claim C Fund Accounting B Fund Accounting $70,000 Beginning balance A Fund Accounting $350,000 Beginning balance - 210,000 Total claims less than $125,000 - 125,000 1st $125,000 catastrophe loss $15,000Remaining balance

Reinsurance $500,000 $50,000 Beginning balance - 1,000Pro- rata contribution CFund Catastrophe Claim: $49,000Balance $175,000 - 70,000 $ 105,000 $300,000 - 15,000 $ 90,000 BFund - 70,000 $0Balance $125,000 AFund Loss Example #2 $210,000 of total claims less than $125,000 and a $1,000,000 catastrophe claim C Fund Accounting B Fund Accounting $70,000 Beginning balance A Fund Accounting $350,000 Beginning balance - 210,000 Total claims less than $125,000 - 125,000 1st $125,000 catastrophe loss $15,000Remaining balance • 15,000Additional for cat. loss $ 0Ending balance

Reinsurance $500,000 $50,000 Beginning balance - 1,000Pro- rata contribution CFund Catastrophe Claim: $49,000Balance $175,000 - 70,000 $ 105,000 $300,000 $70,000 Beginning balance - 15,000 $ 90,000 BFund - 70,000 $0Balance $125,000 $350,000 Beginning balance AFund - 210,000 Total claims less than $125,000 - 125,000 1st $125,000 catastrophe loss $15,000Remaining balance • 15,000Additional for cat. loss $ 0Ending balance Loss Example #2 $210,000 of total claims less than $125,000 and a $1,000,000 catastrophe claim C Fund Accounting B Fund Accounting Shared A Fund Accounting

“Catastrophic Year” Results • Majority of loss reinsured away • Impact on risk sharing minimized • Interest income still generated • C Fund balance still returned

high frequency year The Power of Group Captives

Reinsurance $500,000 CFund $300,000 BFund $125,000 AFund Loss Example #3 $500,000 of total claims less than $125,000 C Fund Accounting $50,000 Beginning balance B Fund Accounting $70,000 Beginning balance A Fund Accounting $350,000 Beginning balance - 500,000 - 150,000 +150,000A Fund Adjustment $0Ending balance

Premium = A + B + C + Operating Costs Expected Maximum Premium = 2A + B + C + Operating Costs • Assessment = A (one additional A Fund Premium) Assessment = Claim Indemnification = Experience Adjustment

how are adjustments funded? The Power of Group Captives

Year 1 Year 2 Year 3 Year 4 Experience Adjustment Schedule $700,000 Premium paid A Fund Claims Exceed A Fund contributions by $150,000 50%of experience adjustment due(Paid quarterly) $150,000 -75,000 $75,000 (Remaining balance) 30%of experience adjustment due (Paid quarterly) $75,000 -45,000 $30,000 (Remaining balance) 20%of experience adjustment due (Paid quarterly) $30,000 -30,000 $0(Remaining balance)

“High Frequency” Year Results $ 70,000 B Fund Balance * $ 50,000 C Fund Balance * $ 20,000Estimated Interest $140,000 Estimated Results ($150,000)Adjustment Paid ($ 10,000)Estimated Cost for $150,000 of additional claims frequency *Some of these dollars will be risk shared.

Adjustments Are Paid Directly Into Loss Fund Accounts • No operational costs (other than FET) • No lump-sum payment • Adjustments evaluated every 6 months • Return of funds if reserves are reduced below initial payments

what is my investment? The Power of Group Captives

Collateral Collateral Collateral Functions Cash Letters of credit Member to member obligations Capitalizes the captive Collateralize policy-issuing carrier