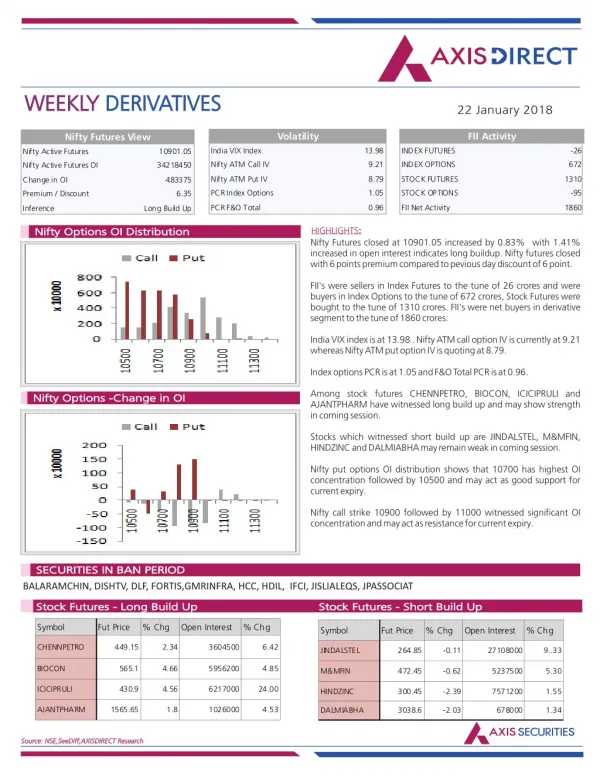

Download

1 / 10

100 likes | 316 Vues

American Accounting Association Government Nonprofit Section 2006 Mid Year Meeting Miami Florida Emergent Research Workshop. An Analysis of Debt – Related Derivatives Usage by US State Governments & Municipalities. Louis J. Stewart Kean University Carol A. Cox George Mason University

E N D

American Accounting Association Government Nonprofit Section 2006 Mid Year Meeting Miami Florida Emergent Research Workshop An Analysis of Debt – Related Derivatives Usage by US State Governments & Municipalities Louis J. Stewart Kean University Carol A. Cox George Mason University Elizabeth K. KeatingHarvard University

A derivative financial instrument (DFI) is an asset or liability that derives its value or obligated cash flows from some other security or collection of securities (index). DFIs can be used to speculate for profit or hedge against existing financial risk. This research focuses primarily on debt related DFI Interest rate swaps Swaptions Forward delivery swaps Interest rate caps What is a DFI?

Descriptive Research Results • Reviewed FY 2002, 2003, & 2004 CAFR • 50 states • 100 largest cities • Debt related DFI enjoyed widespread but not universal utilization • 23 state governments • 24 municipalities • Aggregate notional value of debt related derivatives exceeding $32.7 billion.

Distribution between Types of Governmental Units & Types of DFI

The State of North CarolinaFloating to Fixed Interest Rate Swap Cash Flows and Interest Rates

The State of North CarolinaDebt Related DFI Usage Risks • Falling interest rates such as those seen in the municipal securities markets during the first years of the 21st century can reduce the market value of a fixed rate payer swap to a negative value (liability). • Because interest rates have declined since execution of the swaps, the two swaps have an aggregate negative fair values of $26,582,228 as of June 30, 2003. • When a swap’s fair value is negative, a state government can be exposed to the risk of an unscheduled termination payment under certain circumstances. • Basis risk • LIBOR & BMA Swap index may move different directions over time.

Research Questions • What are the drivers of US governmental debt related DFI usage? • Do debt related DFI usage increase or decrease governmental risk exposure? • What are the drivers of derivative disclosure quality?

Bicksler and Chen (1986), Wall and Pringle, (1989) and Li and Mao, (2003) advances five primary hypotheses that explain the use of debt related DFIs among US investor owned firms. Information asymmetry Agency cost Comparative advantage Downsizing Project completion Debt related DFI use among government and nonprofit debt issuers Brailford, Heaney, & Oliver (2003) Public sector DFI use are positively related to: Size Level of liabilities Stewart and Trussel (2005) Nonprofit DFI users are significantly larger than non DFI users that use significantly higher amounts of floating rate long term debt to finance their significantly greater capital expenditures. Literature Review

Research MethodologyOLS & Logit Regression • Dependent variable • DFI usage (yes or no) • DFI notional value • Independent variables • Size • (total assets or total revenues) • Liquidity • (current assets/ current liabilities or cash equivalents / total assets) • Debt level • (Debt / Total Assets or Debt / Net Assets) • Interest rate exposure • (Floating rate Debt / Total Debt)