Download

1 / 59

590 likes | 1k Vues

Financial and Market Impacts of Hurricanes on Property/Casualty Insurers Past, Present & Future 2007 National Hurricane Conference New Orleans, LA April 5, 2007 Download at: www.iii.org/media/presentations/nhc2007 Robert P. Hartwig, Ph.D., CPCU, President & Chief Economist

E N D

Financial and Market Impacts of Hurricanes on Property/Casualty InsurersPast, Present & Future 2007 National Hurricane Conference New Orleans, LA April 5, 2007 Download at: www.iii.org/media/presentations/nhc2007 Robert P. Hartwig, Ph.D., CPCU, President & Chief Economist Insurance Information Institute 110 William Street New York, NY 10038 Tel: (212) 346-5520 Fax: (212) 732-1916 bobh@iii.org www.iii.org

Presentation Outline • Catastrophe Losses are Growing Globally • US: Hurricanes are Now #1 Source of Insured CAT Losses • Displacing Tornados • Loss Potential from Future Storms is Immense & Growing Rapidly • Acts of God & The Bottom Line • Hurricanes & The Price of Property Insurance • Claims Paying Capacity: The Worst Has Yet to Come • Why US Hurricanes Become a Global Insurance Problem • The Role of State-Run Insurers • Post-Katrina Litigation

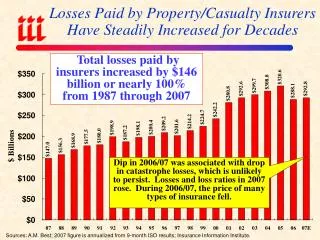

U.S. Insured Catastrophe Losses* $ Billions $100 Billion CAT year is coming soon 2006 was a welcome respite. 2005 was by far the worst year ever for insured catastrophe losses in the US, but the worst has yet to come. *Excludes $4B-$6b offshore energy losses from Hurricanes Katrina & Rita. Note: 2001 figure includes $20.3B for 9/11 losses reported through 12/31/01. Includes only business and personal property claims, business interruption and auto claims. Non-prop/BI losses = $12.2B. Source: Property Claims Service/ISO; Insurance Information Institute

Global Number of Catastrophic Events, 1970–2005 The number of natural and man-made catastrophes has been increasing on a global scale for 20 years Record 248 man-made CATs & record 149 natural CATs in 2005 Man-made disasters: without road disasters. Source: Swiss Re, sigma No. 1/2005 and 2/2006.

Top 10 Most Costly Hurricanes in US History, (Insured Losses, $2005) Seven of the 10 most expensive hurricanes in US history occurred in the 14 months from Aug. 2004 – Oct. 2005: Katrina, Rita, Wilma, Charley, Ivan, Frances & Jeanne Sources: ISO/PCS; Insurance Information Institute.

Insured Loss & Claim Count for Major Storms of 2005* Hurricanes Katrina, Rita, Wilma & Dennis produced a record 3.3 million claims *Property and business interruption losses only. Excludes offshore energy & marine losses. Source: ISO/PCS as of June 8, 2006; Insurance Information Institute.

Inflation-Adjusted U.S. Insured Catastrophe Losses By Cause of Loss, 1986-2005¹ Insured disaster losses totaled $289.1 billion from 1984-2005 (in 2005 dollars). Tropical systems accounted for nearly half of all CAT losses from 1986-2005, up from 27.1% from 1984-2003. 1 Catastrophes are all events causing direct insured losses to property of $25 million or more in 2005 dollars. Catastrophe threshold changed from $5 million to $25 million beginning in 1997. Adjusted for inflation by the III. 2 Excludes snow. 3 Includes hurricanes and tropical storms. 4 Includes other geologic events such as volcanic eruptions and other earth movement. 5 Does not include flood damage covered by the federally administered National Flood Insurance Program. 6 Includes wildland fires. Source: Insurance Services Office (ISO)..

Hurricane Katrina Insured Loss Distribution by State ($ Millions)* Louisiana accounted for 62% of the insured losses paid and 56% of the claims filed Total Insured Losses = $40.579 Billion *As of June 8, 2006 Source: PCS division of ISO.

Hurricane Katrina Loss Distribution by Line ($ Billions)* Total insured losses are estimated at $40.579 billion from 1.7438 million claims. Excludes $2-$3B in offshore energy losses *As of June 8, 2006 Source: PCS division of ISO.

Hurricane Rita Loss Distribution, by Line ($ Millions)* Total insured losses are estimated at $5.0 billion (excl. offshore energy of $2-$3B) from 383,000 claims. *As of June 8, 2006 Source: PCS division of ISO.

Insurers are committed to improving the ability of homes and businesses to withstand major disasters

Figure 8. Free Home Inventory Software at www.iii.org Source: Insurance Information Institute

HURRICANES: INSURED LOSS POTENTIAL Katrina:Just the Beginning?

Total Value of Insured Coastal Exposure (2004, $ Billions) Florida & New York lead the way for insured coastal property at more than $1.9 trillion each. Northeast state insured coastal exposure totals $3.73 trillion. Source: AIR Worldwide

Insured Coastal Exposure as a % of Statewide Insured Exposure (2004, $ Billions) After FL, many Northeast states have among the highest coastal exposure as a share of all insured exposure in the state. Source: AIR Worldwide

New Condo Construction inSouth Miami Beach, 2007-2009 • Number of New Developments: 15 • Number of Individual Units: 2,111 • Avg. Price of Cheapest Unit: $940,333 • Avg. Price of Most Expensive Unit: $6,460,000 • Range: $395,000 - $16,000,000 • Overall Average Price per Unit: $3,700,167* • Aggregate Property Value: At least $6 Billion *Based on average of high/low value for each of the 15 developments Source: Insurance Information Institute from www.miamicondolifestyle.com accessed April 5, 2007.

Historical Hurricane Strikes in Galveston County, TX, 1900-2002 Population of Galveston County is 5 times what it was when the hurricane of 1900 struck, killing 8,000 Source: NOAA Coastal Services Center, http://hurricane.csc.noaa.gov/hurricanes/pop.jsp; Insurance Info. Institute.

Historical Hurricane Strikes in Suffolk County, NY, 1900-2002 Population in Suffolk County is 4.5 times what it was in the 1940s Source: NOAA Coastal Services Center, http://hurricane.csc.noaa.gov/hurricanes/pop.jsp; Insurance Info. Institute.

Historical Hurricane Strikes in Suffolk County, NY, 1900-2002 Population in Barnstable County (Cape Cod) is 5 times what it was in the 1950s Source: NOAA Coastal Services Center, http://hurricane.csc.noaa.gov/hurricanes/pop.jsp; Insurance Info. Institute.

Historical Hurricane Strikes in Dare County, NC, 1900-2002 Source: NOAA Coastal Services Center, http://hurricane.csc.noaa.gov/hurricanes/pop.jsp; Insurance Info. Institute.

Increase in Population of Coastal/Near Coastal Counties in South Carolina(% Change, 1990 - 2005) Several SC coastal counties have experienced very strong population growth since 1990. Home values have also skyrocketed—up 120% in Charleston, Berkeley & Dorchester counties between 1996-2005. Sources: Charleston Metro Chamber of Commerce, SC Statistical Abstract, US Census Bureau.

Nightmare Scenario: Insured Property Losses for NJ/NY CAT 3/4 Storm Insured Losses: $110B Economic Losses: $200B+ Distribution of Insured Property Losses, by State, ($ Billions) Total Insured Property Losses = $110B, nearly 3 times that of Hurricane Katrina Source: AIR Worldwide

Outlook for 2007 Hurricane Season: 85% Worse Than Average *Average over the period 1950-2000. Source: Philip Klotzbach and Dr. William Gray, Colorado State University, April 3, 2007.

Probability of Major Hurricane Landfall (CAT 3, 4, 5) in 2007 *Average over the period 1950-2000. Source: Philip Klotzbach and Dr. William Gray, Colorado State University, April 3, 2007.

ACTS OF GOD & THE BOTTOM LINECatastrophic Loss & Insurer Financial Performance

ROE: P/C vs. All Industries 1987–2008E P/C profitability is cyclical, volatile and vulnerable Sept. 11 Hugo Katrina, Rita, Wilma Lowest CAT losses in 15 years Andrew Northridge 4 Hurricanes *2006-8 P/C insurer ROEs are I.I.I. estimates. Source: Insurance Information Institute; Fortune

Profitability Peaks & Troughs in the P/C Insurance Industry, 1975 – 2008F 1977:19.0% 1987:17.3% 2006E:14.0% 10 Years 1997:11.6% 9 Years 10 Years 1975: 2.4% 1984: 1.8% 1992: 4.5% 2001: -1.2% *2006-8 P/C insurer ROEs are I.I.I. estimates. Source: Insurance Information Institute; ISO, A.M. Best.

Share of Losses Paid by Reinsurers, by Disaster* Reinsurance is playing an increasingly important role in the financing of mega-CATs; Reins. Costs are skyrocketing *Excludes losses paid by the Florida Hurricane Catastrophe Fund, a FL-only windstorm reinsurer, which was established in 1994 after Hurricane Andrew. FHCF payments to insurers are estimated at $3.85 billion for 2004 and $4.5 billion for 2005. Sources: Wharton Risk Center, Disaster Insurance Project; Insurance Information Institute.

Underwriting Gain (Loss) in Florida Homeowners Insurance, 1992-2006E* $ Billions Florida’s homeowners insurance market produces small profits in most years and enormous losses in others *2005 estimate by Insurance Information Institute based on historical loss and expense data for FL adjusted for estimated 2005 residential windstorm losses of $7.35B. 2006 estimate from Ins. Info. Inst.

Cumulative Underwriting Gain (Loss) in Florida Homeowners Insurance, 1992-2006E* Regulator under US law has duty to allow rates that are “fair,” “not excessive” and “not unduly discriminatory.” Reality is that regulators in CAT-prone states suppress rates. $ Billions It took insurers 11 years (1993-2003) to erase the UW loss associated with Andrew, but the 4 hurricanes of 2004 erased the prior 7 years of profits & 2005 deepened the hole. *2005 estimate by Insurance Information Institute based on historical loss and expense data for FL adjusted for estimated 2005 residential windstorm losses of $7.35B. 2006 estimate from Ins. Info. Inst.

Rates of Return on Net Worth for Homeowners Ins: US vs. Florida Averages: 1990 to 2006E US HO Insurance = -0.7% FL HO Average = -38.1% 4 Hurricanes Andrew Wilma, Dennis, Katrina Source: NAIC; 2005/6 US and FL estimates from the Insurance Information Institute.

PRICESFlat or Down Almost Everywhere: Coastal Increases Reflect Risk

Strength of Recent Hard Markets by NWP Growth* 1975-78 1984-87 2001-04 2006-2010 (post-Katrina) period could resemble 1993-97 (post-Andrew) 2005: biggest real drop in premium since early 1980s *2006-10 figures are III forecasts/estimates. 2005 growth of 0.4% equates to 1.8% after adjustment for a special one-time transaction between one company and its foreign parent. 2006-2008 figures from III Groundhog Survey. Note: Shaded areas denote hard market periods. Source: A.M. Best, Insurance Information Institute

*Insurance Information Institute Estimates/Forecasts Source: NAIC, Insurance Information Institute Average Expenditures on Homeowners Insurance Countrywide home insurance expenditures are expected to rise 4% in 2007, but much more in hurricane zones Hurricane zone residents can expect increases in the 20%-100% range, especially if insured by a state entity

Price Increases for Louisiana Citizens—State’s High Risk Insurer of Last Resort +57.4% +2.3% +13.6% +64.6% LACPIC went broke in 2005 by $965 million. Source: Louisiana Citizens Property Insurance Corp. from USA Today, April 3, 2007, p. 1A..

Price Increases for MS Windstorm Underwriting Association—State’s Insurer of Last Resort MWUA went broke in 2005 by $595 million an has received massive state tax subsidies Source: Mississippi Windstorm Underwriting Association from USA Today, April 3, 2007, p. 1A..

Percent of Commercial Accounts Renewing w/Positive Rate Changes, 2ndQtr. 2006 Largest increases for Commercial Property & Business Interruption are in the Southeast, smallest in Midwest Source: Council of Insurance Agents and Brokers

Percent of Commercial Accounts Renewing w/Positive Rate Changes, 4thQtr. 2006 Largest increases for Commercial Property & Business Interruption are in the Southeast, but are diminishing; Smallest in Midwest Source: Council of Insurance Agents and Brokers

U.S. Policyholder Surplus: 1975-2006E* Capacity as of 12/31/06 is $481.5B (est.), 13.1% above year-end 2005, 69% above its 2002 trough and 44% above its 1999 peak. $ Billions Foreign reinsurance and residual market mechanisms absorbed 45% of 2005 CAT losses of $62.1B “Surplus” is a measure of underwriting capacity. It is analogous to “Owners Equity” or “Net Worth” in non-insurance organizations Source: A.M. Best, ISO, Insurance Information Institute *III Estimate.

Capital Raising by Class Within 15 Months of KRW $ Billions Insurers & Reinsurers raised $33.7 billion in the wake of Katrina, Rita, Wilma Source: Lane Financial Trade Notes, January 31, 2007.

Annual Catastrophe Bond Transactions Volume, 1997-2006 Catastrophe bond issuance has soared in the wake of Hurricanes Katrina and the hurricane seasons of 2004/2005 Source: MMC Securities and Guy Carpenter; Insurance Information Institute.

Reinsurance & Capital Markets are Globally Linked Global Reinsurance Market Premiums Ceded States like LA, MS paid little into the global reinsurance pool but got a lot in return, shrinking global claims paying resources and pushing up reinsurance costs for all Losses Paid

Florida Citizens Exposure to Loss (Billions of Dollars) Exposure to loss in Florida Citizens nearly doubled in 2006 and is now the largest home insurer in the state Source: PIPSO; Insurance Information Institute

MS Windstorm Plan: Exposure to Loss (Millions of Dollars) Total exposure to loss in the Mississippi Windstorm Underwriting Association (MWUA) has surged by 431 percent, from $352.9m in 1990 to $1.9bn in 2005. Source: PIPSO; Insurance Information Institute

TX Windstorm Insurance Assoc.:Growth In Exposure to Loss Building & Contents Only, $ Billions TWIA’s liability in-force for building & contents has surged by nearly 200 percent in the last six years from $12.1bn in 2000 to $35.9bn in 2006 Source: TWIA (as of 11/30/06); Insurance Information Institute