Download

1 / 25

380 likes | 1.13k Vues

THE OECD PRINCIPLES OF CORPORATE GOVERNANCE. Stilpon NESTOR OECD. What is corporate governance?. A set of behavioural patterns A normative framework OECD Principles address both areas . Why corporate governance. Mobilisation of capital by corporations Allocation of capital

E N D

THE OECD PRINCIPLES OF CORPORATE GOVERNANCE Stilpon NESTOR OECD

What is corporate governance? • A set of behavioural patterns • A normative framework • OECD Principles address both areas

Why corporate governance • Mobilisation of capital by corporations • Allocation of capital • Monitoring of the use of capital

WHY IS CORPORATE GOVERNANCE IMPORTANT FOR POLICY? • The limited liability corporation • The public corporation and the agency problem • The growth of the private corporate sector • The growth of equity markets and their institutions • The new economy • The growth of international private capital flows

The limited liability company • More than a century- old debate: continuity and limited liability • Still relevant: Company law reform in UK, Sweden, France, Japan, Germany

The Agency problem • The public corporation: markets instead of monitors: market for corporate control, market for managers • Securities regulation: focus on market integrity the state intervenes when there are big information asymmetries to enhance credibility • In the past, largely an Anglo “problem”most countries have adopted Anglo solutions regulatory convergence

The growth of the private sector: privatisation totals more than $700 billion since 1990-- more than one trillion since 1980

Privatisation’s Impact on Stock Market Capitalisation • Market Cap Of Privatised Enterprises (PEs)Rose From <$50 Billion To $2.44 Trillion • PEs Are 10% Of Total, 21% Of Non-US Market Cap • About 30% of total equity issuance during the last 5 years. More than 50% of total issuance in Europe. • Market indices: 28% in UK and Germany, 30% in France, 48% in Spain, 46% in Italy • Five Largest--And 7 Of 8 Largest--Firms of the 200 largest firms in emerging markets are PEs

Over The Past Two Decades Institutional Investors Have Grown Steadily In Size and Importance

The new economy • high risk requires special financial structure and dynamics; few fixed assets; little debt; equity finance and the need of venture capital to exit: they all require a vibrant equity market

The private, market-based investment process, underpinned by better corporate governance is now much more important for most economies, then it used to be 10-15 years ago. The state has a clear interest in developing a domestic capital market if it wants to capture the benefits of increased investment both on the supply and demand side: otherwise flight towards the Nasdaq

FDI and Portfolio Investment Have Increased Their Share of International Investment Flows. 2,021 384 Direct Investment includes equity capital, reinvested earnings and inter-company loans. Portfolio Investment includes equity securities, bonds, notes and money market instruments. Other Investment includes loans and other financial assets and liabilities (both short term and long term), such as trade credits and currency deposits.

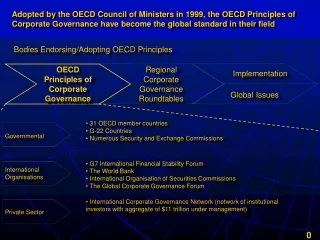

Decision to Develop Core Principles • Governance systems vary widely • No single model of good corporate governance: but need for a global language • Detailed codes, best practices should be established at national and regional levels • Task Force objective: to identify common elements or core principles underlying good corporate governance across the different systems: a multilateral policy framework

Intended Uses of the Principles • Primarily aimed at governments • Guidance also for stock exchanges, investors, corporations, commissions: • Views primarily listed companies

I. Rights of Shareholders • Protection of shareholders’ rights and the capability of shareholders to influence behaviour of the corporation are pillars of good corporate governance

I. Rights of Shareholders • Secure ownership and registration, • Participation in basic decisions (pre-emption and appraisal), • general shareholder meetings: accountability procedures, in absentia voting, proxy rules: the IT impact • disclosure of capital and control structures: corporate groups and block-holders • fair and transparent transfers of control: transparency and fair treatment of all • Institutional voting: pointing to the trend

II. Equitable Treatment of Shareholders • All shareholders - including foreign shareholders - should be treated fairly by controlling shareholders, boards and management

II. Equitable Treatment of Shareholders • Insider trading prohibition: a cornerstone of market integrity in developed economies • Self -dealing and the disclosure of potential conflicting interests: the curse of emerging markets • Effective redress: the possibility to seek remedies in courts for all shareholder: a key implementation aspect • Ex ante transparency with respect to distribution of voting rights and ways voting rights exercised • Beneficial ownership and the role of custodians: OECD trends and ADR issue

III. The Role of Stakeholders • most stakeholders’ rights are protected by other laws (labour law, environmental law, etc.) • In some countries, the Board is also accountable to some stakeholders, particularly the employees (but not only) • The Principles are agnostic on formal stakeholder participation, • The Principles urge transparency, including to stakeholders • They urge incentives for stakeholder participation as a value enhancing mechanism driven by the corporations themselves: i.e. encourage firm specific- investment.

IV. Disclosure and Transparency • A strong financial and non financial disclosure regime is the heart of corporate governance:

IV. Disclosure and Transparency • Financial and operating results • Company objectives • Ownership and control structure • Board and executive information and recommendation • Foreseeable risk factors • Stakeholder information • Governance information • Independent audit and high quality dissemination channels

V. The Role of the Board • The Board is the main mechanism for monitoring management and developing strategy

V. The Role of the Board • The key issue:independence from management • Target : non -executive participation (but “the boards should consider..”) with specific tasks: audit , remuneration, nomination • Act fairly with respect to various groups of shareholders, deal fairly with stakeholders, assure compliance with laws • Review strategy and planning, manage potential conflicts of interest, assure integrity of accounting, reporting and communications • Board members need to spend time and have good information

Often there is a tension between markets vs.. the law. The Principles do not address this issue. They provide a conceptual framework of issues. These are taken up in the OECD/World Bank Round tables and discussed in all the regions of the world. So these regions can provide their own agenda for reform and improvement of corporate governance.