Michigan School Districts 101

200 likes | 394 Vues

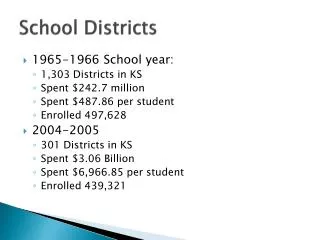

Michigan School Districts 101. Maner Costerisan 2014. Michigan Public School System . There are 882 Public School Districts within the State of Michigan as of 2013. Intermediate School Districts – 56 Local Education Authorities (K-12) – 549 Public School Academics – 277

Michigan School Districts 101

E N D

Presentation Transcript

Michigan School Districts 101 ManerCosterisan 2014

Michigan Public School System • There are 882 Public School Districts within the State of Michigan as of 2013. • Intermediate School Districts – 56 • Local Education Authorities (K-12) – 549 • Public School Academics – 277 • These institutions are servicing 1,529,887 students.

Michigan Public School System • Schools are considered a Local Unit of Government • Subject to Governmental Accounting Standards • Michigan Public Acts that govern Townships, Cities, Counties, etc. • Michigan Department of Education (MDE) is the state department that oversees all of these institutions. • MDE mandates annual audits • Require audits to be performed under Government Auditing Standards (Yellow Book) • Reason for this is because of how these institutions are funded.

Michigan Public School System • Approximately 90% of school district funding comes from three sources: • Property Taxes • State Aid • Federal Government

Property Taxes: • School Districts can levy up to 18 mills each year on non-principal residence property. • $18 for every $1,000 of taxable value • They are allowed to levy additional mills if approved by the voters, such items would include: • Debt (capital outlay to build or renovate facilities) • Community programs • Sinking Fund

Property Taxes: • Misconception that residential property directly fund the operating expenses for districts. • Homeowners are exempt from the 18 mills if the home is their primary residence • Homeowners do directly fund the additional mills (debt, community programs, etc.) • Homeowners do pay 6 mills for the State Education Property Tax, which goes to the State of Michigan to fund the School Aid Fund (SAF)

Property Taxes: • Property taxes that the district receives directly are from the following: • Commercial real estate (6 mills) • Non principal residence exempt property • Includes business, rental property, vacation homes and commercial agriculture

State Sources: • The state spent approximately $13.2 billion on funding for Michigan Schools for 2013 • The state funds the School Aid Fund by multiple sources: • Sales and use tax (42.6%) • Personal income tax (17.7%) • State Education Property Tax (13.4%) • Federal Revenue (12.5%) • Miscellaneous taxes (5.9%) • Lottery (5.5%) • General Fund (2.1%) • Other (.2%)

State Sources: • Districts receive a dollar amount on a per pupil basis (foundation): • This amount will fluctuate on a district by district basis • Districts that receive higher property taxes, will receive a lower state aid payment • The attempt is to level out funding for all districts across the state • The average amount paid on a per pupil basis for 2013 was $7,400 across the state for each student

State Sources: • The state also provides funding through items called “categorical” funds. These funds are above and beyond the foundation allowance. This money operates like grants. Such items include funding for: • Special Education • At risk

Federal Funding: • Funds received from the federal government. The majority of these funds are typically passed through the Michigan Department of Education. The most common programs for schools are the following: • Title I • National school lunch program • Districts that spend more than $500,000 in federal awards funds are subject to OMB Circular A-133, commonly referred to as Single Audit

Federal Funding: • Single Audits are considered to be compliance audits. The Single Audit reports on how the federal funds are being spent and if they are being spent according to the guidelines. • Effective for years beginning after January 1, 2015, the threshold for a single audit will increase to $750,000.

What are a district’s major expenditures? • The majority of a district’s expenditures, approximately 80%, consists of the following items: • Salaries and wages • Health insurance • Retirement expenses

What challenges will a district face going forward? • Since the recession, property taxes have gone down significantly, both commercial and residential values. This affects what a district receives locally from taxes and puts a strain on the School Aid Fund. In addition, how a district services its debt payments is also affected. • As property taxes remain lower, more and more districts are having to borrow from the State of Michigan to make the bond payments. What they are receiving from the property tax millage isn’t covering their obligations.

What challenges will a district face going forward? • The state budget cuts had a significant impact on school funding. • Since 2009, the average per student funding is down approximately $470. • Property tax values and funding on a per pupil basis have increased in the past year. However, they are not keeping pace with costs.

What challenges will a district face going forward? • Major expenditure issues are: • Ever increasing costs of health insurance • Increase cost for retirement benefits • Effective June 30, 2015, districts are required to report their portion of the unfunded pension obligation. The exact impact on a district by district basis has yet to be determined.