Download

1 / 25

250 likes | 350 Vues

Delve into the history, challenges, and successes of CPA firm mobility within the accounting profession, exploring the development of legislation, collaborative efforts, and current implementation status. Learn about the impact on practitioners and the public, addressing concerns and the future outlook for firm mobility.

E N D

An Overview of CPA Firm Mobility Gary McIntosh AICPA Co-Chair, Uniform Accountancy Act Committee September 9, 2014

Mobility: A Short History • Prior to the Profession’s Individual CPA Campaign, CPAs often had to hold multiple reciprocal state licenses • Bureaucratic Compliance Nightmare • Inconsistent Standards Across the States

Mobility: A Short History • Approximately a decade ago, profession leaders joined together to try to resolve the problem • Idea launched to treat a CPA license like a driver’s license – portable across state lines

Mobility • Basic concept • No notice • No fee • No escape (strong protections)

Mobility • Additionally, a CPA license, like a driver’s license, must be predicated on substantial equivalency • A CPA = a CPA = a CPA • 150 hours of education, CPA Exam passed, 1 year of experience

Uniform Accountancy Act • Individual CPA Mobility Language was inserted into the Uniform Accountancy Act (UAA) in 2006 • UAA is the profession’s model state act • Written jointly by AICPA and NASBA • States then model their accountancy statutes off of the UAA

Mobility • The original plan allowed full individual and CPA firm mobility • Concerns arose, however, about how the new concept would work in practice • Untested • Particular interest in being cautious about the attest function • Final proposal changed to allow individual CPA mobility and CPA firm mobility for non-attest services • Attest services would still require the registration of a CPA firm in any state where attest services are offered, however the firms’ CPAs could operate without reciprocal licenses • Additional concerns at the time about peer review, use of firm names, and CPA ownership standards – mostly now resolved

The Campaign Begins • A True Partnership of the Entire Profession • State CPA Societies • State Boards of Accountancy • AICPA • NASBA • CPA Firms and individual CPAs

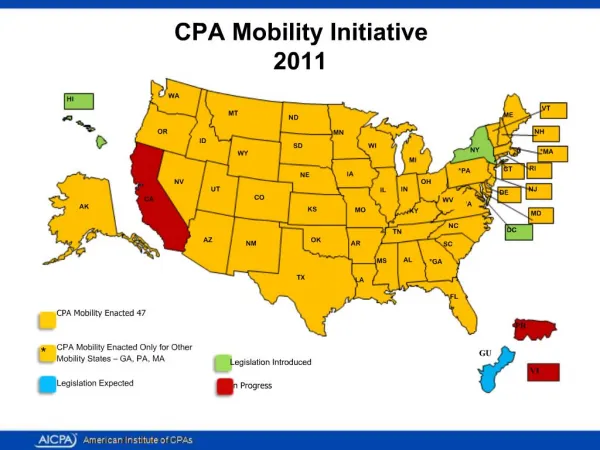

Mobility • Only 3 Jurisdictions Remain • Hawaii (Discussions occurring regarding a 2015 push) • Guam (legislation expected in Summer/Fall 2014) • Commonwealth of the Northern Mariana Islands (legislation expected in Summer/Fall 2014)

Mobility • Additionally, AICPA and NASBA have established resources for CPA Firms and Individual CPAs • CPAMobility.org

An Incredible Success Story • Statutes modernized to reflect actual way CPAs practice around the country • No complaints about enforcement by state BOAs • Bureaucratic red tape and fees that don’t serve public interest eliminated • Envy of other professions

Mobility • Nonetheless, some minor implementation issues remain • Some states still have a few state-specific provisions (ex. casinos, ag audits) • Massachusetts and Georgia have “quid pro quo” provisions

Firm Mobility • Profession now revisiting CPA Firm Mobility for attest • Completion of a promise made in 2006 • Timely after successful history with individual mobility

Uniform Accountancy Act Initiative on CPA Firm Mobility for Attest • Multi-year project • Exposure draft with 90 day comment period • Approximately 3 dozen comment letters received • Language approved Spring 2014 by AICPA and NASBA • States being asked to look at the new language

Firm Mobility Model for Attest Services • Same as individual mobility • “no notice, no fee, no escape” • Already in place for non-attest services • States will gain additional explicit authority to go after unregistered firms

Firm Mobility: Public Protections • To be eligible, must comply with peer review and CPA ownership requirements of mobility state • If not in compliance, then must seek to register as an ‘out-of-state’ firm

Firm Mobility • 14 states already have CPA firm mobility and it appears to be working well • States like OH and VA have had firm mobility for over a decade

Firm Mobility • This new language will not be a concerted campaign. • Commitment not to push like with individual CPA mobility • Reasons: • Individual CPA mobility is too new in some states • Other pressing state issues needing to take precedent • Boards and societies need to review the concept, discuss with stakeholders and members, consider if appropriate

Firm Mobility • What are the biggest obstacles and concerns in regard to CPA Firm Mobility? • Same common concerns we heard in regard to individual mobility in the past • Need to educate, discuss, and develop a comfort level among our partners

Firm Mobility • Lessons from the UAA Comment Period on the CPA Firm Mobility Language • State Societies and CPA Firms all broadly supportive • State BOAs mixed, some strongly supportive, others opposed or had questions or concerns • States BOAs with CPA firm mobility already in place often proved to be the most supportive of other states joining them

Firm Mobility • Common Concerns That Needed to be Examined • Understanding the peer review protections • Potential Insufficient Information without registration/notification • Questions about enforcement • Inconsistency between states (e.g. compilations) • Concerns about insufficient information or study of the issue. • Potential Loss of Revenue from Out-of-state Registration Fees