Download

1 / 66

660 likes | 899 Vues

Risk Management Lecturer : Mr. Frank Lee. Session 2. Analytics of Risk Management I: Sensitivity and Derivative Based Measures of Risk. Overview. Quantitative measures of risk - 3 main types Sensitivity and Derivative based measures of risk Sensitivity analysis Differentiation

E N D

Risk Management Lecturer: Mr. Frank Lee Session 2 Analytics of Risk Management I: Sensitivity and Derivative Based Measures of Risk

Overview • Quantitative measures of risk - 3 main types • Sensitivity and Derivative based measures of risk • Sensitivity analysis • Differentiation • Gap analysis • Duration • Convexity • The ‘Greeks’

Introduction • Risk management relies on quantitative measures of risk. • Various risk measures aim to capture the variation of a given target variable (e.g. earnings, market value or losses due to default) generated by uncertainty. • Three types of quantitative indicators: • Sensitivity • Volatility • Downside measures of risk

Emphasis on Quantitative Measures • When data become available risks are easier to measure - increased use of quantitative measures • Risks can be qualified and ranked even if they cannot be quantified (e.g. ratings agencies) • Regulators’ emphasis and requirements - e.g. banking industry capital requirements .

Sensitivity • Percentage sensitivities are ratios of relative variations of values to the same shock on (variations of) the underlying parameter • E.g. if the sensitivity of a bond price to a unit interest rate variation is 5, 1% interest rate variation generates a relative price variation of a bond of 5 x 1% = 5%. • A value sensitivity is the absolute value of change in value of an instrument for a given change in the underlying parameters • E.g. if the bond price is $1000, its variation is 5% x 1000 = $50

Sensitivity Continued • Return sensitivity - e.g. stock return sensitivity to the index return (Beta). • Market value of an instrument (V) depends on one or several market parameters (m), that can be priced (e.g indexes) or percentages (e.g interest rates) • By definition: s (% change of value) = (ΔV/V) x Δm S (value) = (ΔV/V) x V x Δm s (% change of value) = (ΔV/V) x (Δm/m) * *% change of parameter

Sensitivity Continued • The higher the sensitivity the higher the risk • The sensitivity quantifies the change • Sensitivity is only an approximation - it provides the change in value for a small variation of the underlying parameter. • It is a ‘local’ measure - it depends on current values of both the asset and the parameter. If they change both s and S do.

Sensitivities and Risk Controlling • Sources of uncertainty are beyond a firms control • random market or environment changes, changes in macroeconomic conditions • It is possible to control exposure or the sensitivities to those exogenous sources of uncertainties • Two ways to control risk: • Through Risk Exposures • Through Sensitivities

Sensitivities and Risk Controlling • Control risk through Risk Exposures - limit the size of the amount ‘at risk’ • e.g. banks can cap the exposure to an industry or country • drawback - it limits business volume • Risk control through Sensitivities • e.g. use derivative financial instruments to alter sensitivities • for market risk, hedging exposures help to keep the various sensitivities (the ‘Greeks’) within stated limits

Sensitivities and derivative calculus • Sensitivity is the first derivative of the value (V) with respect to m (parameter) • First derivative measures the rate with which the value changes with changes in an underlying factor • The next order derivative (second derivative) takes care of the change in the first derivative (sensitivity) • Second derivative measures how sensitive is the first derivative measure to changes in the underlying risk factor

Differentiation - A Reminder • Differentiation measures the rate of change • for a function: y = k xn • dy/dx = nk xn-1 • e.g. if y=10x2, then dy/dx = 20x • the original function is not constant, so ife.g. x=2, dy/dx = 10x = 20 • for a linear function there is no advantage in using the derivative approach - inspect the equation parameters (e.g. if y=10x, then dy/dx = 10, i.e. is constant) • When looking at a graph plot of y against x, the change can be defined in terms of slope

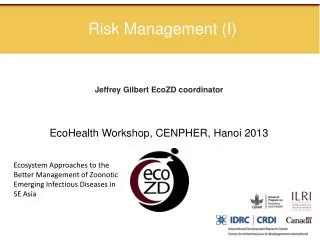

Derivative Measures of Risk • When looking at a graph plot of y against x, the change can be defined in terms of slope Value of Financial Obligation b a Underlying Risk Factor

The Second Derivative - a Reminder • In case of quadratic function (e.g. y=-5x2) we can recognise whether the turning point derived represents a maximum or a minimum. • If we develop business models using higher power expressions we may not be able to do so without looking at a graph • To do this numerically, we need to use the second derivative (the same differentiation rules apply) • If the second derivative is negative - maximum • If the second derivative is positive - minimum

The Second Derivative - a Reminder • E.g. a profit function: Π= -100 +100x - 5x2 • Its first derivative: d Π/dx = 100 - 10x • The second derivative: d 2Π/dx2 = - 10 • Since the second derivative is constant and negative - therefore the turning point is a maximum

Partial Differentiation - a Reminder • In case of partial differentiation we only differentiate with respect to one independent variable. Other variables are held constant • For example: if z=2x+3y • Its partial derivative (by x): δz/δx = 2 (since y is constant, 3y is constant - the derivative of a constant is 0) • Its partial derivative (by y): δz/δy = 3

Issues in Relation to Calculus Based Measures • Need to Specify Mathematical Relationship so require a Pricing Model - Bond Valuation, Option Pricing Models • Thus difficult to apply to complicated portfolios of obligations • Applies to Localised Measurement of Risk • An approximation of the function

Sensitivity based measures of risk: Tools and Application

Risk Management Tools • Interest Rate Risk Management: • Gap analysis • Duration • Convexity

Re-pricing Model for Banks • Repricing or funding gap model based on book value. • Contrasts with market value-based maturity and duration models recommended by the Bank for International Settlements (BIS). • Rate sensitivity means time to re-pricing. • Re-pricing gap is the difference between the rate sensitivity of each asset and the rate sensitivity of each liability: RSA - RSL.

Maturity Buckets • Commercial banks must report repricing gaps for assets and liabilities with maturities of: • One day. • More than one day to three months. • More than 3 three months to six months. • More than six months to twelve months. • More than one year to five years. • Over five years.

Repricing Gap Example AssetsLiabilitiesGap Cum. Gap 1-day $ 20 $ 30 $-10 $-10 >1day-3mos. 30 40 -10 -20 >3mos.-6mos. 70 85 -15 -35 >6mos.-12mos. 90 70 +20 -15 >1yr.-5yrs. 40 30 +10 -5 >5 years 10 5 +5 0

Applying the Repricing Model • DNIIi = (GAPi) DRi = (RSAi - RSLi) Dri Example: In the one day bucket, gap is -$10 million. If rates rise by 1%, DNIIi = (-$10 million) × .01 = -$100,000.

Applying the Repricing Model • Example II: If we consider the cumulative 1-year gap, DNIIi = (CGAPi) DRi = (-$15 million)(.01) = -$150,000.

CGAP Ratio • May be useful to express CGAP in ratio form as, CGAP/Assets. • Provides direction of exposure and • Scale of the exposure. • Example: • CGAP/A = $15 million / $270 million = 0.56, or 5.6 percent.

Equal Changes in Rates on RSAs & RSLs • Example: Suppose rates rise 2% for RSAs and RSLs. Expected annual change in NII, NII = CGAP × R = $15 million × .01 = $150,000 With positive CGAP, rates and NII move in the same direction.

Unequal Changes in Rates • If changes in rates on RSAs and RSLs are not equal, the spread changes. In this case, NII = (RSA × RRSA ) - (RSL × RRSL )

Unequal Rate Change Example • Spread effect example: RSA rate rises by 1.2% and RSL rate rises by 1.0% NII = interest revenue - interest expense = ($155 million × 1.2%) - ($155 million × 1.0%) = $310,000

Restructuring Assets and Liabilities • The FI can restructure its assets and liabilities, on or off the balance sheet, to benefit from projected interest rate changes. • Positive gap: increase in rates increases NII • Negative gap: decrease in rates increases NII

Weaknesses of Repricing Model • Weaknesses: • Ignores market value effects and off-balance sheet cash flows • Overaggregative • Distribution of assets & liabilities within individual buckets is not considered. Mismatches within buckets can be substantial. • Ignores effects of runoffs • Bank continuously originates and retires consumer and mortgage loans. Runoffs may be rate-sensitive.

The Maturity Model • Explicitly incorporates market value effects. • For fixed-income assets and liabilities: • Rise (fall) in interest rates leads to fall (rise) in market price. • The longer the maturity, the greater the effect of interest rate changes on market price. • Fall in value of longer-term securities increases at diminishing rate for given increase in interest rates.

Maturity of Portfolio • Maturity of portfolio of assets (liabilities) equals weighted average of maturities of individual components of the portfolio. • Principles stated on previous slide apply to portfolio as well as to individual assets or liabilities. • Typically, MA - ML > 0 for most banks

Effects of Interest Rate Changes • Size of the gap determines the size of interest rate change that would drive net worth to zero. • Immunization and effect of setting MA - ML = 0.

Maturity Matching and Interest Rate Exposure • If MA - ML = 0, is the FI immunized? • Extreme example: Suppose liabilities consist of 1-year zero coupon bond with face value $100. Assets consist of 1-year loan, which pays back $99.99 shortly after origination, and 1¢ at the end of the year. Both have maturities of 1 year. • Not immunized, although maturities are equal. • Reason: Differences in duration.

Price Sensitivity and Maturity • In general, the longer the term to maturity, the greater the sensitivity to interest rate changes. • Example: Suppose the zero coupon yield curve is flat at 12%. Bond A pays $1762.34 in five years. Bond B pays $3105.85 in ten years, and both are currently priced at $1000. • Bond A: P = $1000 = $1762.34/(1.12)5 • Bond B: P = $1000 = $3105.84/(1.12)10

Example continued... • Now suppose the interest rate increases by 1%. • Bond A: P = $1762.34/(1.13)5 = $956.53 • Bond B: P = $3105.84/(1.13)10 = $914.94 • The longer maturity bond has the greater drop in price because the payment is discounted a greater number of times.

Coupon Effect • Bonds with identical maturities will respond differently to interest rate changes when the coupons differ. This is more readily understood by recognizing that coupon bonds consist of a bundle of “zero-coupon” bonds. With higher coupons, more of the bond’s value is generated by cash flows which take place sooner in time. Consequently, less sensitive to changes in R.

Remarks on Preceding Slides • The longer maturity bonds experience greater price changes in response to any change in the discount rate. • The range of prices is greater when the coupon is lower. • The 6% bond shows greater changes in price in response to a 2% change than the 8% bond. The first bond is has greater interest rate risk.

Duration • Duration • Weighted average time to maturity using the relative present values of the cash flows as weights. • Combines the effects of differences in coupon rates and differences in maturity. • Based on elasticity of bond price with respect to interest rate.

Duration • Duration D = Snt=1[Ct• t/(1+r)t]/ Snt=1 [Ct/(1+r)t] Where D = duration t = number of periods in the future Ct = cash flow to be delivered in t periods n= term-to-maturity & r = yield to maturity (per period basis).

Duration • Since the price of the bond must equal the present value of all its cash flows, we can state the duration formula another way: D = Snt=1[t (Present Value of Ct/Price)] • Notice that the weights correspond to the relative present values of the cash flows.

Duration of Zero-coupon Bond • For a zero coupon bond, duration equals maturity since 100% of its present value is generated by the payment of the face value, at maturity. • For all other bonds: • duration < maturity

Computing duration • Consider a 2-year, 8% coupon bond, with a face value of $1,000 and yield-to-maturity of 12%. Coupons are paid semi-annually. • Therefore, each coupon payment is $40 and the per period YTM is (1/2) × 12% = 6%. • Present value of each cash flow equals CFt ÷ (1+ 0.06)t where t is the period number.

Special Case • Maturity of a consol: M = . • Duration of a consol: D = 1 + 1/R

Duration Gap • Suppose the bond in the previous example is the only loan asset (L) of an FI, funded by a 2-year certificate of deposit (D). • Maturity gap: ML - MD = 2 -2 = 0 • Duration Gap: DL - DD = 1.885 - 2.0 = -0.115 • Deposit has greater interest rate sensitivity than the loan, so DGAP is negative. • FI exposed to rising interest rates.

Features of Duration • Duration and maturity: • D increases with M, but at a decreasing rate. • Duration and yield-to-maturity: • D decreases as yield increases. • Duration and coupon interest: • D decreases as coupon increases

Economic Interpretation • Duration is a measure of interest rate sensitivity or elasticity of a liability or asset: [dP/P] [dR/(1+R)] = -D Or equivalently, dP/P = -D[dR/(1+R)] = -MD × dR where MD is modified duration.

Economic Interpretation • To estimate the change in price, we can rewrite this as: dP = -D[dR/(1+R)]P = -(MD) × (dR) × (P) • Note the direct linear relationship between dP and -D.