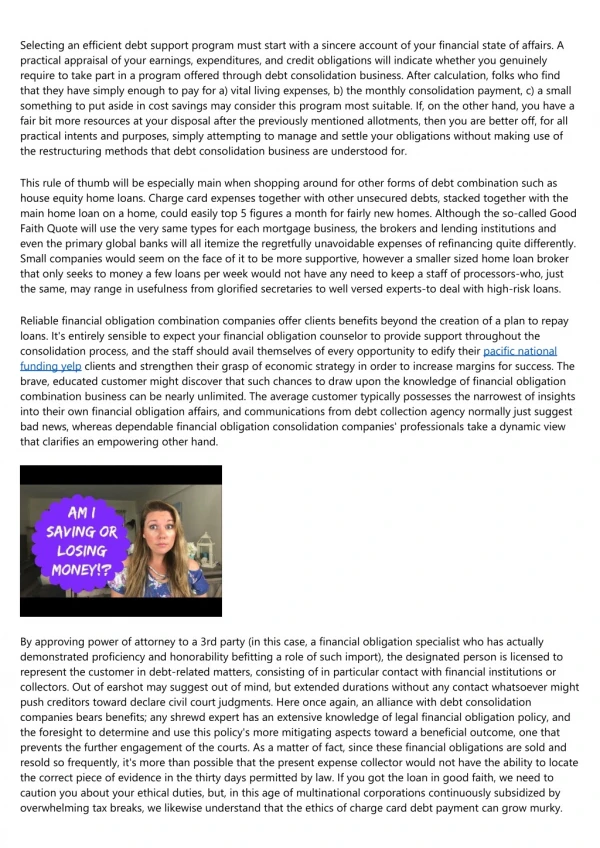

Download

1 / 10

100 likes | 222 Vues

Join our comprehensive Recovering from Debt Workshop designed for Botshelo House, facilitated by Coaching Consolidated (Pty) Ltd. Explore the root causes of debt such as illness, divorce, retrenchment, and inflation. Learn to manage your financial burdens through effective budgeting, communication with creditors, and consolidation options. Understand the significance of debt counselling and the differences between debt review and administration orders. Equip yourself with practical tools to prioritize debts, reduce expenses, and safeguard your financial future.

E N D

Recovering from Debt Workshop Developed for Botshelo House by Coaching Consolidated (Pty) Ltd

Causes of debt • Illness • Divorce • Retrenchment • Salary cuts • Inflation

What affects the interest rate charged on debt? • Credit rating of the borrower • Term of the loan • Type of loan • Any factor that affects the risk • Interest rate • Inflation

How can I overcome debt problems? • Review your budget and cut back on unnecessary spending • Phone your creditors and discuss your situation with them • Cut up credit and store cards • Consider a debt consolidation loan • Apply for debt counselling (debt review)

What is debt counselling? • Debt counsellors are registered and regulated by the National Credit Regulator • Assess eligibility of the applicant for debt review • Provides protection from having creditors take legal action and repossessing assets • Where legal proceedings have already commenced, that specific credit agreement is excluded from debt review • Makes provision for reorganisation of debt, by reducing monthly instalments

Debt Review vs Administration Order Debt Review Administration Order Debt limited to R 50 000 Fees 12.5% Payment collection by the Administrator Record of Administration order retained on credit record min 5 years max 10 years • Unlimited debt • Fees 5% capped at R 400 (excl.) for 24 months and 3% thereafter • Payment collection and distribution done by Payment Distribution Agencies • Credit record will not reflect credit review once clearance certificate issued

Prevention is better than cure • Don’t ignore your debt • Prioritise and pay your debts • Avoid borrowing to pay off debt • Cut down on expenses • Start saving

Insurance options available • Income protection insurance • Illness • Disability • Credit life insurance • Pays outstanding balance of credit agreement in the event of death or disability • Retrenchment • Account payment plan for up to 6 months • Unemployment Insurance Fund • Income replacement benefits (30 – 58% of income)