Download

1 / 9

90 likes | 308 Vues

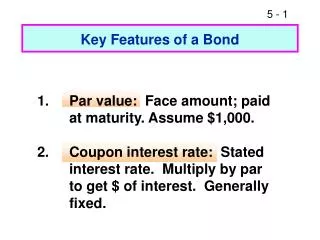

Ch. 18 BASIC BOND CONCEPTS I. BOND FEATURES A. Maturity B. Coupon rate C. Par value D. Pay off provisions E. Denomination currency F. Options 1. Issuer a. Call & refunding provisions b. Prepayment options

E N D

Ch. 18 BASIC BOND CONCEPTS I. BOND FEATURES A. Maturity B. Coupon rate C. Par value D. Pay off provisions E. Denomination currency F. Options 1. Issuer a. Call & refunding provisions b. Prepayment options c. Accelerated sinking fund d. Caps on floating coupon rate 2. Investor a. Conversion privilege b. Put provision c. Floor on floating coupon rate G. Classifications 1. Issuer a. Government b. Corporate 1. Industry 2. Quality

BOND RISKS • I. Types • A. Credit (quality) • 1. Default • a. Ratings • 1. Moodys • 2. S&P • b. Downgrade/upgrade • B. Interest rate (greatest) • 1. Price/yield curve • 2. Reinvestment rate • C. Call • D. Liquidity • E. Inflation • F. Exchange rate • G. Volatility

VALUATION OF FIXED-INCOME SECURITIES • Bond valuation model • A. Noncallable • where • BNC = current bond price • Ct = semiannual coupon pmt. • MT = maturity value • rt = semiannual YTM • II. Bond value computations • A. Bond price • 1. Discount • 2. Premium • B. YTM

COMPUTING BOND MEASURES I. Bond valuation calculator terms A. PMT = period coupon dollar payment B. n = number of periods to maturity C. i = periodic market interest rate = (YTM) D. FV = bond face value at maturity E. PV = bond price

BOND PRICE CHANGES I. Bond theorems A. Changes in bond prices are inversely related to changes in market YTMs B. Holding coupon rate constant, the longer (shorter) the term to maturity, the more (less) sensitive the bond price is to changes in market YTMs C. Holding maturity constant, the higher (lower) the coupon payment, the less (more) sensitive the bond is to changes in market YTMs

BOND RISK MEASUREMENT I. Conventional bonds A. Risk measures 1. Macauley’s Duration = price if yields decline – price if yields rise (2 x initial price X decimal change in yield) 2. Modified duration (D*) D* = D / (1 + r) 3. Convexity II. Bond portfolio duration (DP) = S wiDit III. Use of duration A. Estimate bond price change % price change = [-D* x % change in YTM] $ price change = [- D* x B0 x YTM change] RELATIONSHIP TO D THEOREM A. YTM - A B. Maturity + B C. Coupon - C