Download

1 / 92

920 likes | 1.07k Vues

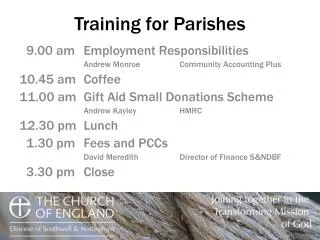

Join us for a comprehensive training session on Employment Responsibilities and Gift Aid for Parishes. Starting at 9:00 AM, Andrew Monroe will guide participants through essential topics including employment status, contracts, and compliance with HMRC regulations. After a coffee break at 10:45 AM, Andrew Kayley will discuss recent changes to Gift Aid and the Small Charitable Donations Scheme. This event will close at 3:30 PM, ensuring all attendees leave with valuable insights to effectively manage their parish’s employment and charitable donations.

E N D

Training for Parishes 9.00 am Employment Responsibilities Andrew Monroe Community Accounting Plus 10.45 am Coffee 11.00 am Gift Aid Small Donations Scheme Andrew Kayley HMRC 12.30 pm Lunch 1.30 pm Fees and PCCs David Meredith Director of Finance S&NDBF 3.30 pm Close

Employment Responsibilities: Parishes By Andrew Monroe Employment Service Manager Community Accounting Plus

Main Topics for Today:“Whistle-stop Tour” • Status • Employed or Self-employed? • Worker or Employee? • Contracts of Employment • HMRC: PAYE and RTI • Further Advice

Status Why is this important? Worker or Employee or Self-employed (Gardener, Verger and Organist) Where does liability rest PCC, if not self-employed?

The Daily Mail Forget clawing back billions from Starbucks, Google and Amazon... The taxman is targetting village cricket clubs! Payments to weekend scorers, Sawbridgworth Cricket Club was sent a bill for £14,403 plus £3,000 in ‘penalties and interest’. Chairman Val Waring said it was a 'David versus Goliath' battle for the club. HMRC eventually waived some of the penalties. But the 151-year-old club was forced to take out a loan, and to ask its 350 members to help pay the final bill of almost £15,500.

Employee Status Are they Employed or Self-Employed? • Not determined by choice • Determined by the facts of the employment relationship • Self-employment elsewhere may not count • HMRC Website: Employment Status Indicator (ESI) • www.hmrc/calcs/esi.htm e.g • Do they have a Contract of Employment • Do they have to do the work or can they hire someone? • Do they get paid by the hour/weekly? • Do they set hours of work? • Do they supply their main tools of work? • Do they have an established “business”?

Casual (Worker) Status • No legal definition • They carry out work personally, but have no Contract of Employment • Concept of “No Mutuality of Obligation”. If you do offer any work, they do not have to accept • Hence each period of employment does not link to another, thus continuity does not happen • Employment status is a “worker” • Limited employment rights • Beware “familiarity” leading to employee status

Offers of Employment • A contract exists as soon as an offer is made and is accepted • Conditional or Unconditional offers • References / DBS checks • Withdrawal of job offers • Need for contract of employment to have full terms and conditions of employment • Contract type, fixed/permanent etc. • Written main statement MUST be provided within 2 months of starting work if employment expected to last longer than 8 weeks.

HMRC - PAYE Legal obligation to deduct PAYE and NI (if applicable) No longer any exemption for local religious centres. Do you need to register for PAYE? Yes if: Pay above the PAYE threshold Pay above the NI Lower Earnings Threshold (£109/wk) Worker has another job Worker is receiving a state, company or occupational pension IF REGISTERED YOU MUST REPORT ALL PAYMENTS IN RTI

HMRC, PAYE • Employment status? • Includes payments to employees and workers • Does new starter have a P45? • No – issue a P46 and get them to sign it • Where eligible *, if pay > £109/week (as of April 6th 2013) • * Obligations to pay Statutory Sick Pay • * Obligations to pay Statutory Maternity / Adoption or Paternity Pay

Real Time Information (RTI) New as from April 2013 All payments must be reported via RTI, on or before payment is made HMRC can levy penalties for non-compliance RTI can only be reported via compliant software Manual payroll no longer possible HMRC provide their basic tools payroll which is RTI compliant Provide end of year P60’s to staff

Reporting in RTI EAS – Employer Alignment Submission, a one off submission before reporting, to provide basic data on workers (full name, NI number etc.) FPS – Full Payment Submission, reports what is paid to worker. MUST be on or before any payment made to worker (weekly/monthly/quarterly etc.) EPS – Employer Payment Submission, made if what you pay does not match the FPS (eg. SSP payments) Beware irregular payments. If no FPS for 3 consecutive payments, HMRC will assume they are a leaver unless reported they are irregular!

Further Advice • CA Plus Website (www.caplus.org.uk) • Employment Pages • Downloadable Advice Guides • Free monthly Employment Newsletter via email • (Registration via website) • Also, can be downloaded from website

What I will cover today? • Gift Aid declaration recent changes • Small Charitable Donations scheme • On-line Claim Service • Any other Gift Aid queries

Declaration Gift Aid declaration Declaration must contain • Name of charity • Name of donor • Donors home address • Description of payment(s)* • Declaration that payment(s) are Gift Aided Charities must explain that the donor must have paid sufficient UK income or capital gains tax to cover the tax claimed by the charity (not including Council Tax & VAT)

Declaration Gift Aid Declarations (GADs) Feb. 2012 – new guidance published on GADs & introduced a GAD tick list • Clarify (for donors) the requirement to pay sufficient income tax in each tax year • Charities must keep GADs for 6 years (not 4 years) after last payment was claimed on

Declaration Gift Aid Declarations(GADs) • All existing GADs (& any pre-April 2000 Deeds of Covenant) are still valid for claiming purposes • HMRC recommended all charities to update their GADs by 31 December 2012 • Do not have to introduce 3 tick box options on Gift Aid declarations • Signature is still not required to make GAD valid

Small Charitable Donations Act 2012 (Gift Aid small donations scheme) From 6 April 2013; Charities, Churches & CASCs that receive small cash donations of £20 or less will be able to apply for a Gift Aid style repayment without the need to obtain Gift Aid declarations for those donations. The total amount of the small donations will be capped at £5,000 per tax year = a top-uprepayment of £1,250.

Summary of GASDS Only applies to donations received on/after 6 April 2013 (or Sunday 7 April 2013) GASDS is a public spending initiative (not a repayment of tax) that gives Charities & CASCs a top-up payment on donations they receive Charities & CASCS will claim a top-up payment of upto £1,250 on £5,000 max. of small donations received in any tax year 2 year time limit for claiming on GASDS donations

A small donation? A cash donation of £20 or less from an individual Donations must be collected and/or banked in the UK Cash donations from Companies or Trusts cannot be GASDS Membership Fees are not small donations for GASDS purposes

Interaction between GASDS & Gift Aid Charities must claim Gift Aid on donations that are at least 10% of the amount of their GASDS payments, or The amount of GASDS received can be up to ten times the amount of Gift Aid payments received Called the “matching principle” ? Declaration

The “matching principle” A charity has income of £6,000 in 2013/14; Gift Aid = £500 + GASDS = £5,500 Small donations are 10 times the Gift Aid donations Charity can claim £125 on £500 Gift Aid + £1,250 on £5,000 of the total small donations received

Eligibility for claiming GASDS The charity must have been in existence for at least 2 full tax years before it claims GASDS Made successful GA claims in 2 of the previous 4 tax years, with no gap in claims of 2+ years Charity has not incurred an HMRC penalty in respect of its GA or GASDS claims in the previous 2 tax years. Why? - A good Gift Aid record gives some assurance to HMRC that a charity has appropriate internal processes in place to operate GASDS correctly

Connected Charities The limit on which a Charity may claim a top-up payment may be reduced if a charity is connected with one or more charities. This includes; The same person has control of both charities A group of two or more persons has control of both charities

Connected Charities The restriction ensures as far as possible that charities that operate in a broadly similar way but are structured differently receive the same entitlements under the scheme Prevents charities from fragmenting in order to be eligible for multiple GASDS allowances

Community Buildings The maximum small donations limit can be increased for charities running their charitable activities in community buildings. If a charity runs activities at several centres then each centre could satisfy the community buildings rules. “Running charitable activities in a community building” = local groups of at least 10 people that meet in the same building on at least 6 occasions each year. The people meeting must be beneficiaries of the charity

Community Buildings Includes; A village hall A town hall A church A synagogue A mosque etc. A school • Does not include buildings used wholly or mainly for residential purposes or the sale of goods e.g. • Vicarage / Manse • Care homes • Residential Hospice • Charity shops

Community Buildings Two or more buildings on the same or adjacent land will be treated as a single building for GASDS community building purposes; e.g. Church & Church Hall A school that has 6 buildings in total Church with a Garden Shed HMRC can make an order that a building is, or is not, to be treated as a community buildings

Collections in a Community Building Have to be 10 or more people present at every ‘Service’ for small cash donations to be eligible. Not eligible Money collected during a ‘Service’ when 9 or less people attended. Money given in Collection boxes, wall safes or for lighting a candle by visitors Cash donations handed to Vicar or Church Wardens whilst visiting Parish members in their home

Diocese of Southwell & Nottingham Central Gift Aid scheme Community Buildings £5,000 allowance divided equally amongst all 360 Parishes - Diocese will claim on up to £5,000 for each Community Building

Independent parishes £5,000 small donation limit divided equally amongst all 360 Parishes Connected Charities Each Parish will separately claim on up to £5,000 of the Community Building amount

GASDS record keeping HMRC will not be prescriptive but; Charities must be able to show that they have recorded cash collected in the UK & the cash was paid into a UK bank account Small donations & Gift Aid donations can be banked together – if supported by cash collection sheets The number of people that attended each service

HMRC Data Processing Centre Charity Repayment Service (Up to 1,000 donors) Option 2 Government Gateway Option 1 Paper Charity Claim form - ChR1 (2013) Option 3 3rd. Party Software (OOO’s of donors) Gift Aid, Other Income & Charity Small Donation scheme schedules Charity Repayment Claim Options in 2013 On line From own Laptop or PC By post Extracted Claim information Claim data HMRC Charities

Paper ChR1 Claim Form + ChR1CS (Continuation sheet) Only available direct from HMRC Form will be handwritten, scanned and data extracted ChR1 - space for 15 Gift Aid donors + 6 Other taxed income items + 2 Community Buildings + 5 Connected charities ChR1CS - space for 5 more extra Gift Aid donors Photocopies not acceptable Typed schedules & Covering letters not acceptable

Charity Repayment Claim service Went Live in April 2013. • only charities registered with HMRC can use the Service • must first register on the HMRC website - Online services • ID & Activation PIN posted to authorised official • then need to Register and activate online service • separate service for Agents that submit claims on behalf of charities