Download

1 / 35

350 likes | 674 Vues

OIL MONEY: BLESSING OR CURSE?. Sweder van Wijnbergen University of Amsterdam s.j.g.vanwijnbergen@uva.nl. OIL MONEY: BLESSING OR CURSE?. What are the stylized facts? Economic Mechanisms Dutch Disease, Overheating and Macroeconomic policy Oil Income, Volatility and Economic Growth

E N D

OIL MONEY: BLESSING OR CURSE? Sweder van Wijnbergen University of Amsterdam s.j.g.vanwijnbergen@uva.nl

OIL MONEY: BLESSING OR CURSE? What are the stylized facts? Economic Mechanisms Dutch Disease, Overheating and Macroeconomic policy Oil Income, Volatility and Economic Growth Oil, Corruption and Economic Growth Policy Implications Fiscal Sustainability assessment in Oil Countries Towards a Medium term Budgetary Framework

What are the stylized facts? • Do Resource Rich Countries (RRCs) have slower non-oil growth than Resource Poor Countries (RPCs)? • Oil discovery triggers initial boom • Once mature, slow non-oil growth • On balance mixed evidence • RRCs face upward pressure on their real exchange rate • RRCs face much higher volatility in income, spending and real exchange rates than RPCs • RRCs are more than average plagued by corruption

All stylized facts are related to poor growth performance • Real appreciation causes a small T-sector. • If T-sector has higher productivity growth (Balassa-Samuelson), this explains slow non-oil growth (Dutch Disease) • High volatility is also related to slow growth • Volatility is like a tax on investment • Corruption has strongly negative effects on economic growth

Oil, Exchange Rates and the Dutch Disease • Oil, spending and the real exchange rate • Oil wealth, capital inflows and exchange rates • Policy Issues: • Overheating, Inflation and Exchange Rate Policy • Oil wealth, capital inflows and exchange rate overshooting • Commercial banks, external debt and currency crises

Oil, Dutch Disease and Exchange Rates • Simple Model

Oil, Spending and the real exchange rate • High expenditure (private or public) increases demand for NT-goods => real appreciation unavoidable • Real Appreciation is the mechanism through which supply NT goods up: resource pull from T- towards NT-sector • Two ways to get real appreciation: • Nominal appreciation • Domestic inflation in excess of foreign inflation (plus nominal depreciation) • Conflict: expenditure increases versus maintaining stable real exchange rate • Maintain low exchange rate while expenditure up anyhow: overheating • Abandon exchange rate target OR limit expenditure • Temporary real appreciation reason for concern • Diversification subsidies or invest in human capital, financial market development?

Oil, DD and the real exchange rate:Is there a Case for Intervention? • Is there an externality in T-goods production? • For example: • Learning by Doing in T-sector (van Wijnbergen, EJ 1986) • Irreversibilities in sectoral skills & Financial Market Imperfections (Caballero and Lorenzoni 2007) • Learning by Doing externalities: • With perfect capital markets no clear result on whether optimal intervention increases with more oil, because real appreciation permanent • Temporary spending increases lead to temporary real appreciation, optimal subsidy (explicit diversification policy) does increase • Occurs after • Overshooting (Neary-van Wijnbergen: Private Capital Inflows in early stage boom) • Inappropriate spending policies when oil revenue is temporary (no PI approach) • Irreversibilities and Financial Market Imperfections • Option value capital in T-sector may get lost if there are liquidity constraints • Common Element: Only when boom is temporary a reason to worry • Azerbeijian yes, Kazakhstan no

Real Appreciation and Expenditure policies in Azerbeijian • Spending unavoidably leads to upward pressure on Real Exchange Rate • Do not resist UNLESS spending restrained • Oil money relaxes borrowing constraint • can invest in long overdue public infrastructure • increases FUTURE productivity at expense current appreciation • Risks • maintain quality control public investment • inflexibility in downturns • Policy response • strengthen public investment appraisal (Chile example) • build up strong oil fund, limits on non-oil deficit (self insurance)

Oil wealth, capital inflows and exchange rates • Future Increases in oil income may lead to capital inflows now • What if oil income does not materialize (price uncertainty!) • Overshooting risk (excessive appreciation) • Capital Inflows how? • DFI less volatile: can dry up in downturns, can not exit • Bank borrowing can lead to negative resource flows in down turns • Bank borrowing likely to be excessive • Gamble on bail outs by Government, IFIs • One way bets when exchange rate appreciation resisted by CB • Sterilization attempts under limited capital mobility lead to high domestic interest rates • But exchange rate pressure towards appreciation • Speculators get a one-way bet as long as oil price stays high • Currency Mismatch: => risk of TWIN CRISES in downturns

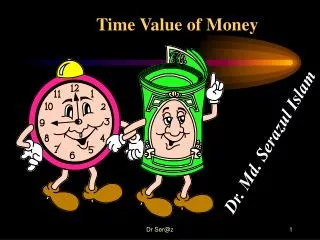

1980 1974 1998 120 100 80 l 60 40 20 0 2004 1981 1993 1921 1933 1945 1957 1969 1873 1885 1897 1909 1861 Orange bands reflect mean and median prices. (Mean = $23.88, Median = $18.07) Volatility: Oil Price Uncertainty $/barrel Source: BP Statistical Review of World Energy

Causes of High Spending Volatility-I • High marginal propensity to spend out of CURRENT income => income volatility leads to expenditure volatility • Government failure to smooth expenditure • Pressure of different interest groups => MPC > 1 (Voracity effect) • Oil wealth = collateral => easier to borrow internationally • Value collateral correlated with income (drops in value when you need it most) • Temptation to ignore recurrent costs • Gov. investment inflexible, high stopping costs in downturns • High income volatility may trigger Debt Overhang Problems: many RRCs experience debt crises in downturns!!!

Debt Overhang • Debt Overhang a problem when debt trades at deep discounts: debt then has equity characteristics • When resource flows dry up, old debt shares in new project returns, so investment incentives distorted: Debt Overhang • Debt relief coupled with commitment to investment program (structural adjustment program?) leads to efficiency gain, borrower gains without loss to lender • Ineffective commitment to investment program leads to break down of the process, win-win not possible without efficiency gains • Role WB in debt restructuring: makes investment commitment credible

Causes of High Spending Volatility-II • Capital Inflows may lead to overshooting exchange rate • Upward pressure on exchange rate => Commercial banks incentive to borrow in $$ and lend in LC • Rapid growth credit to private sector • Large FX exposure, risk of TWIN CRISES in down turns • All approaches to lower cap inflows lead to higher domestic interest rates (so difficult to enforce) • But e-rigidity (volatility e “too” low) => volatility y “too” high • Combination high volatility expenditure AND rigid exchange rates causes Boom-Bust cycles

Volatility and Growth • Volatility deters irreversible investment (option value of waiting) • Particularly important in countries with limited financial sector development (limited possibility for risk sharing) • Aghion: in Financially underdeveloped countries, 50% increase in volatility => 1/3 decline in TFP growth • High Insurance value reserves (oil fund, bird in the hand policy)

Corruption, Natural Resources and Growth • Significant causal link between Natural resource wealth and corruption • Rental income increases opportunity for theft • Significant causal link between corruption and slow growth • Corruption = weak property rights enforcements, exacerbates hold up problems => deters investment • Corruption opportunities increase with discretionary powers government officials => cost of doing business up • Discretionary powers up to increase corruption revenues => allocative inefficiency up

Policy Implications: Macroeconomics • Dutch Disease • Pressure on real exchange rate unavoidable if/when oil income spent • Capital inflows/bank borrowing may lead to overshooting • Resistance appreciation WITHOUT curbs on G-spending, Cap Inflows leads to overheating, high inflation • Oil income and real appreciation long term: Invest in quality and accessability education, not in diversification subsidies • Volatility • Smooth G-expenditure through Oil Fund & non-oil deficit rules • Oil fund rules based on Long Term Oil Price • Accompany Oil Fund rules with limits on NON-OIL deficits • Limit Commercial Bank Borrowing in FX • Assess efficiency, NPV public investment especially in upturns • Share risk: issue GDP-linked debt or debt linked to oil prices • Corruption • Anti-corruption programs crucial, but political support difficult for obvious reasons

Policy Implications: Sharing the Gains with future generations through OIL FUNDS • Oil Funds • Permanent Income Approach, but • Future generations will be richer • What if PI overestimates oil wealth • Overestimating oil wealth • Type I error much costlier than type II • Spending too little: loss of interest only • Spending too much usually very costly (break up costs, debt overhang issues,…) • PI versus “bird in the hand”policy (Norway) • Equivalent if oil money stops per “now” • Governance issues • Investment problems • Underdeveloped capital markets at home • Gradual real appreciation lowers domestic return on investing abroad

Policy Implications: Fiscal Sustainability • In spite of oil wealth, special vulnerability to FX crises and Debt Overhang problems • FSA analysis should pay special attention to down side risk • Insurance Value of Reserves high: • implications for oil fund rules • Oil-linked debt? • Be careful before recommending diversification strategies • Expensive insurance policy • Properly managed oil fund to stretch out spending period and period of real appreciation is better alternative

Specific Policy Issues in Azerbeijian • Interaction Public Investment Program and • real appreciation • private sector productivity today (↓) versus tomorrow (↑) • Much bigger vulnerability problems • Oil price volatility • Significant possibility of big outliers, clustering of high volatility periods • Role for debt management (risk sharing) or oil fund (self insurance)

Agenda for Future Work • Explore link between real exchange rate, public investment and current and future profitability of T-sector • Oil Fund Strategies • trade offs between current and future consumption • trade offs between investment today versus oil fund accumulation • Impact on Oil Fund Rules • of spending inflexibility (High cost of stopping investment projects, debt overhang issues) • Clustering of volatility in oil prices

Designing a Medium Term Budgeting Strategy • Medium Term Framework • Implications Medium term Framework • Managing uncertainty • Implications for Year-to-Year Budgeting

Medium Term Framework • Sharing the Oil Wealth with Future Generations? • Permanent Income Approach to feasible increase in consumption • but future will be richer, so slant towards current generation? • Transforming Oil wealth into Physical Capital • Oil relaxes financing constraints • But how to avoid waste? • Public investment raises future productivity, but not necessarily public sector revenue • => financing issue? • => consume less from oil wealth or issue debt when needed • Public investment today • puts upward pressure on the real exchange rate and so lowers competitiveness today • but increases FUTURE competitiveness through higher productivity

Implications Medium Term Framework • Selection Public Investment Projects • easy financing does not mean anything goes • establish public investment office (PIO) for cost benefit analysis public sector projects • monitoring effectiveness and cost control key key tasks of public investment office • locate PIO in Finance Ministry • Define sequence of public investment projects • analyse recurrent costs, input in future budgets • financing in case public investment generates growth but insufficient public revenues to be fully self-financed

Managing Oil (Price) Uncertainty • Oil revenues highly uncertain • use higher discount rates to account for riskyness oil income • upside risk not a big issue, what matters is downside risk • Managing Downside Risk • How inflexible is future government expenditure? • trade off between financing and adjusting to negative price shocks • Role of debt management • can hedge short term fluctuations through derivatives markets, issue of oil-linked debt • longer term: fiscal adjustment • “self-insure” through Oil Fund

Year-to-Year Budgetting • Inputs • future growth/real exchange rate given public investment plans • feasible/desirable consumption out of oil wealth • recurrent expenditure flowing from public investment program • define allocations to/withdrawals from oil fund under different price scenarios • Formulate matching restrictions on non-oil-fiscal-deficits (nopd) • Fiscal Sustainability Analysis: V@R approach (Budina & van Wijnbergen • assess V@R future debt levels in bad case scenarios • assess value oil-linked debt?

Next Steps? • Quantify Long Term Policy Trade Offs • Public Investment, non-oil growth and the real exchange rate • implications for exchange rate & monetary policy framework • Institutional reforms PIO • Quantify • public investment program, • recurrent costs public investment, • oil fund rules, • allowable non-oil deficits • Stochastic analysis to assess vulnerability • debt/Oil Fund management, oil fund rules