Download

1 / 6

80 likes | 327 Vues

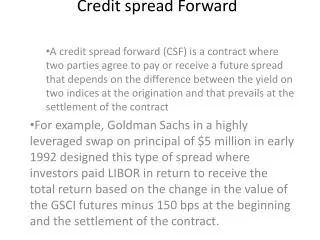

Credit spread Forward. A credit spread forward (CSF) is a contract where two parties agree to pay or receive a future spread that depends on the difference between the yield on two indices at the origination and that prevails at the settlement of the contract

E N D

Credit spread Forward A credit spread forward (CSF) is a contract where two parties agree to pay or receive a future spread that depends on the difference between the yield on two indices at the origination and that prevails at the settlement of the contract For example, Goldman Sachs in a highly leveraged swap on principal of $5 million in early 1992 designed this type of spread where investors paid LIBOR in return to receive the total return based on the change in the value of the GSCI futures minus 150 bps at the beginning and the settlement of the contract.

Example CSF • Suppose an investor entered into a CSF transaction in three months over a period of 182 days with GS on notional principal of $5 million. Assume that in three months the LIBOR is at 3.75 percent and the GSCI is at 2530. The GSCI is equal to 2565 at the end of the contract. The investor at the settlement of the contract pays $93,750 and receives $31,669.96 for a net payment of –$62,080.04 as follows: • Pay: (.0375). 1/2 (5,000,000) = $93,750 • Receive: {[2565/2530 –1]-1/2 (.0150)}(5,000,000) = $31,669.96 • Net: -$62,080.04

Credit Spread Option • This OTC option contract allows two parties to enter into a contract where the buyer/writer pays/receives an upfront fee for contingent cash flow in the future if the spread, widens/tightens above the strike price.

Credit Spread Option • Spread/call put buyer: Investor • Spread/call put writer: Bank • Notional Principal NP: $25 million • Current spread: 2.25 % • Strike (exercise) spread call/put: 2.15 % (out of the money forward call, in the money forward put) • Duration DUR: 12.5 years • Exercise date: 6 months from today • Call option premium: 55 bps of the notional principal payable by investor to the bank • Put option premium: 105 bps of the notional principal payable by investor to the bank • Settlement date: Today, February 14, 2002 • Underlying index: XYZ bonds due July 10, 2022 • Reference benchmark Index: 5.785 % U.S. Treasury bond offer yield due September 2022 • Index credit spread: the yield to maturity of the underlying index 6.25 % coupon is estimated as (bid price net of any accrued interest) bid yield less the offer yield of the U.S. Treasury bonds at 12.00 PM New York EST time two days prior to exercise date. • Call option payment: NP x DUR x Max (2.15 % - index spread, 0) • Put option payment: NP x DUR x Max (Index credit spread –2.15%, 0)

Asset Swap Switch • Example: Consider a bank that is long on an Argentine bond at a spread of LIBOR + 450 bps that wishes to offload this bond and acquire an alternative New Zealand sovereign bond currently trading at a spread of LIBOR +120 bps if the Argentine spread widens to LIBOR + 500 bps without widening in the New Zealand spread in the next six months. The spread of the two issues against LIBOR are not correlated in the above scenario.

Asset Swap Switch • 30 bps • Conditional on widening of • Argentina spread to LIBOR +500 bps • The parties exchange bonds. • Argentina Bonds Asset Swap New Zealand Bonds Asset Swap • LIBOR + 450 bps LIBOR + 120 bps • Long put in one asset plus short put in another asset conditional on widening of the spread produces asset swap switch. Counter party Bank