Download

1 / 5

50 likes | 226 Vues

The monetary model of exchange rate determination comprises stable money demand functions, money market equilibrium, interest parity, and purchasing power parity. Learn how economic fundamentals and equations influence exchange rate outcomes.

E N D

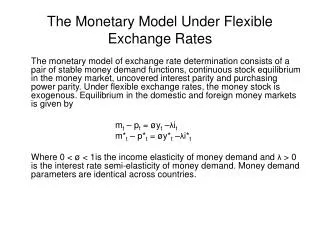

The Monetary Model Under Flexible Exchange Rates The monetary model of exchange rate determination consists of a pair of stable money demand functions, continuous stock equilibrium in the money market, uncovered interest parity and purchasing power parity. Under flexible exchange rates, the money stock is exogenous. Equilibrium in the domestic and foreign money markets is given by mt – pt = øyt –λit m*t – p*t = øy*t –λi*t Where 0 < ø < 1is the income elasticity of money demand and λ > 0 is the interest rate semi-elasticity of money demand. Money demand parameters are identical across countries.

International capital market equilibrium is given by uncovered interest parity: it – i*t = Etst+1- st Where Etst+1 E(st+1| It) is the expectation of the exchange rate at date t+1, conditioned on all public information, It, available to economic agents at date t. Price levels and the exchange rate are related through purchasing power parity: st = pt – p*t To simplify the notation, call ft (mt – m*t) – ø(yt – y*t) The economic fundamentals. Now substitute and we get st = ft + λ(Etst+1 - st)

Solving for st gives where The first equation is the basic first order stochastic difference equation on the monetary model and serves the same function as an “Euler Equation” in optimizing models. It says that expectations of future values of the exchange rate are embodied in the current exchange rate. High relative money growth at the home leads to a weakening of the home currency, while high relative income growth leads to a strengthening of the home currency.

Next, advance time by one period, to get Take expectations conditional on time t information, use the law of iterated expectations to get substitute back into the last equation. Now do this for st+2, st+3,…..,st+k and you have Eventually, you will want to drive , but in doing so you need to specify the behavior of the term: