Understanding Real Business Cycles through Supply-Side Economics

360 likes | 512 Vues

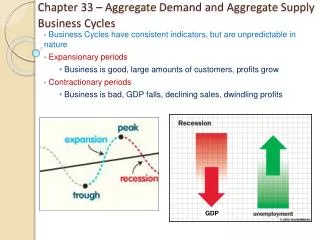

This overview presents the neoclassical supply-side economics framework explaining how business cycles stem from unexpected productivity shocks. It highlights key mechanisms: initial impacts in labor markets lead to lower employment, wages, and output. Investment dynamics are examined, detailing how productivity declines can cause reduced investment demand, impacting future capital stock. The analysis includes examples of negative supply shocks, such as oil price hikes, and their cascading effects on labor demand and the economy. Historical context, notably the 2001 recession and stock market collapse, further illuminates these concepts.

Understanding Real Business Cycles through Supply-Side Economics

E N D

Presentation Transcript

Real Business Cycles Supply Side Economics

Neoclassical (Supply Side) Economics suggests that business cycles are the result of random disturbances to productivity. The Real Economy

Neoclassical (Supply Side) Economics suggests that business cycles are the result of random disturbances to productivity. The initial impact takes place in labor markets (employment/output) The Real Economy

Neoclassical (Supply Side) Economics suggests that business cycles are the result of random disturbances to productivity. The initial impact takes place in labor markets (employment/output) Capital markets determine the impact on future labor markets (Investment today affects the capital stock in the future) The Real Economy

Example: A negative supply shock • Consider an unanticipated rise in oil prices (permanent enough to impact capital investment).

Example: A negative supply shock • Consider an unanticipated rise in oil prices (permanent enough to impact capital investment). • This drop in productivity lowers labor demand resulting in lower wages, lower employment, and lower output

Example: A negative supply shock • Now, moving to capital markets, the drop in productivity ( from lower employment as well as high oil prices) lowers investment demand

Example: A negative supply shock • Now, moving to capital markets, the drop in productivity ( from lower employment as well as high oil prices) lowers investment demand • Lower investment demand causes interest rates, investment, and savings to fall

Investment and the Capital Stock • Recall that investment is defined as the purchase of new capital goods.

Investment and the Capital Stock • Recall that investment is defined as the purchase of new capital goods. • Capital goods are constantly wearing out (depreciation). Therefore, positive investment is needed to maintain the current capital stock.

Investment and the Capital Stock • Recall that investment is defined as the purchase of new capital goods. • Capital goods are constantly wearing out (depreciation). Therefore, positive investment is needed to maintain the current capital stock. • The capital stock evolves according to K (Future) = (1-dep)*K + I

Investment and the Capital Stock • Recall that investment is defined as the purchase of new capital goods. • Capital goods are constantly wearing out (depreciation). Therefore, positive investment is needed to maintain the current capital stock. • The capital stock evolves according to K (Future) = (1-dep)*K + I • A large enough drop in current investment causes the capital stock to shrink.

Example: A negative supply shock • With a lower capital stock, labor productivity drops (capital and labor are complements) causing another drop in labor demand

Example: A negative supply shock • With a lower capital stock, labor productivity drops (capital and labor are complements) causing another drop in labor demand • Therefore, wages, employment, and output continue to fall

Example: A negative supply shock • Lower employment causes another drop in capital investment (not as big as the previous decline – the capital stock is lower than it was before)

Example: A negative supply shock • Lower employment causes another drop in capital investment (not as big as the previous decline – the capital stock is lower than it was before) • Interest rates and investment continue to fall

What caused the current recession? • Collapse of the stock market • The Dow dropped 30% from its Jan 14, 2000 high of $11,722 • The Nasdaq dropped 75% from its March 10, 2000 high of $5,132 • The S&P 500 dropped 45% from its July 17, 2000 high of $1,517

What caused the current recession? • Collapse of the stock market • The Dow dropped 30% from its Jan 14, 2000 high of $11,722 • The Nasdaq dropped 75% from its March 10, 2000 high of $5,132 • The S&P 500 dropped 45% from its July 17, 2000 high of $1,517 • Y2K/Capital Overhang

What caused the current recession? • Collapse of the stock market • The Dow dropped 30% from its Jan 14, 2000 high of $11,722 • The Nasdaq dropped 75% from its March 10, 2000 high of $5,132 • The S&P 500 dropped 45% from its July 17, 2000 high of $1,517 • Y2K/Capital Overhang • A sharp rise in oil prices (oil prices doubled in late 1999)

What caused the current recession? • Collapse of the stock market • The Dow dropped 30% from its Jan 14, 2000 high of $11,722 • The Nasdaq dropped 75% from its March 10, 2000 high of $5,132 • The S&P 500 dropped 45% from its July 17, 2000 high of $1,517 • Y2K/Capital Overhang • A sharp rise in oil prices (oil prices doubled in late 1999) • Enron/Accounting scandals

What caused the current recession? • Collapse of the stock market • The Dow dropped 30% from its Jan 14, 2000 high of $11,722 • The Nasdaq dropped 75% from its March 10, 2000 high of $5,132 • The S&P 500 dropped 45% from its July 17, 2000 high of $1,517 • Y2K/Capital Overhang • A sharp rise in oil prices (oil prices doubled in late 1999) • Enron/Accounting scandals • Terrorism/SARS