Download

1 / 13

130 likes | 234 Vues

Financial regulation: a market failure interpretation Peter Howells. No shortage of problems in financial products and services:. The misselling of private pension schemes in the 1990s The Equitable Life affair, beginning in 2000 (or maybe earlier)

E N D

Financial regulation: a market failure interpretation Peter Howells

No shortage of problems in financial products and services: • The misselling of private pension schemes in the 1990s • The Equitable Life affair, beginning in 2000 (or maybe earlier) • The ‘split-cap’ investment trust collapse in 2003 • The problems of endowment-linked mortgages after 2000 • The crisis in occupational pensions from 2001 …and accompanying calls for more, better, different regulation.

In economics, the standard justifications for regulation/intervention: • Externalities • Asymmetric information • Monopoly • Public goods • Q: Can we apply this framework to arguments for financial regulation? • A: Can certainly apply first three (then we’ll look at costs of regulation).

Externalities Externalities: costs (or benefits) for people other than the transactors. Central to arguments for banking regulation. We assume that banks, borrowers and depositors receive private benefits which just equal marginal cost. But the more people that have cheque accounts, the more efficient is the payment system with widespread (external) economic benefits. If a bank fails and the payments system collapses there are major (external) costs. Hence: lender of last resort, deposit protection schemes, liquidity requirements etc…

Widespread belief that society as a whole benefits if retired/elderly individuals enjoy a secure and adequate standard of living. (= external benefits). • Hence policy-makers concern with current inadequate level of long-term saving. • Events like - • Equitable Life • retrospective changes to occupational pension rules • underfunding of occupational pensions • reduce confidence in the financial system and in long-term saving. • We will all lose if this produces future generations of impoverished elderly. • So we have calls for tighter regulation/supervision, pension protection fund, simpler (‘CAT’ standard) products).

Asymmetric information • Prevalent in financial goods and services: • Complex products (purchase of specialist information) • ‘One-off’, lifetime purchase (no scope for learning, reputation building) • Official policy encourages ill-informed to participate • Hence, scope for misselling (impossible without asymmetric information). • Claims of inadequate information/warnings are the basis of compensation claims in connection with: • the split-cap investment trust collapse • endowment mortgage disappointments • Arguments over whether joining a pension scheme should be compulsory, reflect an anxiety that ‘financial myopia’ (we only get old once) encourages people to undersave.

Monopoly • Built in tendency in much financial activity, because: • FA subject to economies of scale, but also • Diversification (=risk reduction) increases with size • Not clear that UK banking regulators are especially concerned about this but: • The UK’s Competition Commission refused to approve the Lloyd-TSB merger with Abbey National in 2001 on the grounds that it reduced choice to retail customers. • But allowed the Abbey’s merger with Banco Santander in 2004.

Types of intervention • Disclosure requirements • Licensing requirements • Regulation of exchanges (for traded securities) • Restrictions on activity • Capital adequacy • Liquidity requirements (mainly banks and other DTIs) • Deposit protection (mainly banks and other DTIs) • Exposure (to risk) limits

Costs of regulation: Easy to make a case for regulation but remember it involves costs (and other disadvantages). In theory, we should ‘regulate’ up to the point where the marginal cost of the regulation = marginal benefit. Not clear what that means in practice – and anyway many regulation decisions are based on political costs and benefits.

Moral hazard • This is the argument that if people feel they are protected they will behave more recklessly than if they were not. • For example, with a scheme that guarantees some protection for employers’ pension schemes, firms (and their employees) have less incentive to monitor the scheme to make sure that it is being run prudently. • 2. Agency capture • This refers to the possibility that the regulatory body comes to see things too much from the point of view of the regulated firm. • This can happen because the regulator has often to recruit people from the regulated firms, who know how the firms work. They retain contacts within the firms and want to appear helpful to ex-colleagues. • This can be made worse if employees of the regulator know that they can take careers later in the regulated firms.

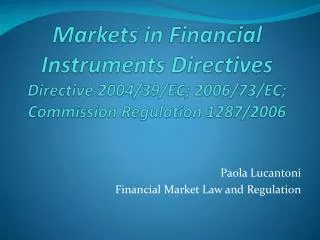

3. Compliance costs All regulation involves some degree of cost for those being regulated. For example: • Providing additional information about products and giving buyers a ‘cooling-off’ period involve additional costs. • Firms will often find that they have to set up internal controls (‘compliance departments’) to make sure they are meeting the regulations. Adding to firms costs by regulation has exactly the same effect as adding to its costs by imposing a tax on the product.

The additional cost is shown by the red line and the effect is to shift SLto SL’. 0 The volume of activity falls from 0L to 0M And its price rises from P to P’ SL’ Price SL P’ P Quantity M L

Finally, barriers to entry. Market participants may have to satisfy regulators about a wide range of issues before being allowed to practice. This has the effect of restricting entry. Firms may be required to employ staff with a specific professional qualification. If these are in short supply, then entry to the market will be restricted. Licensing, which may seem an obvious way of ensuring that only well-run firms can offer a particular kind of service, by definition restricts entry. If this is the case then it leads to potential inefficiencies by reducing competition.