Download

1 / 6

60 likes | 136 Vues

Explore the impact of securitization on the financial industry, role of FNMA & FHLMC, home loan rates, mortgage challenges faced by institutions, and foreclosure issues. Stay informed to navigate the complexities of the mortgage market.

E N D

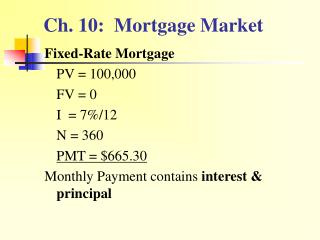

Securitization • Securitization has been the most significant trend in the financial industry for the past 30 years • Primary reason for decline in bank share of assets • Reduces costs to consumers • Increases complexity • Introduces possible moral hazard/conflicts • Moves assets from banks to institutional investors

Role of FNMA & FHLMC • Finance directly $2T mortgages • Guarantee even more • Establish underwriting standards for the “prime” mortgage market • Cause distortions • Credit allocation programs • Do not discern between “good” markets/states and “bad” markets/states

Home Loan Rates Article • 30 year mortgages at 4.27% • Could be 3.80% • Larger than normal spread between note and secondary market rate • Oligopoly of big banks? • Risk that loans might not qualify • MBS rate is 3.21% • 4.27% - 3.21% = 1.06% • Normal around .60% • Loan rate could be 3.21% + .60% = 3.81%

Pimco/NY Fed/BofA Article • Totla of $47B mortgages challenged • $105B of original par • Failures by Countryside • Origination • Servicing • Servicer required to put back loans • Loan modification question puts banks/servicer in the middle

Foreclosure Article • Purchase of Countrywide is source of problems for B of A • Article as of 10/15 • From 10/12 to 10/21, BAC lost 16% while the S&P 500 gained 1% • Independent money manager estimated BAC loss at 50% of market cap • How mortgage modifications hurt investors • Particularly senior tranches