Download

1 / 17

170 likes | 268 Vues

Understand the key elements driving positive member outcomes in Defined Contribution pension schemes and the evolving DC landscape to ensure a secure retirement income.

E N D

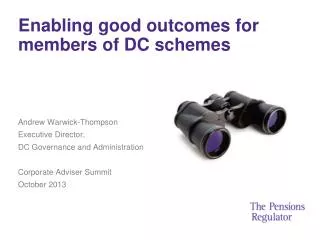

Enabling good outcomes for members of DC schemes Andrew Warwick-Thompson Executive Director, DC Governance and Administration Corporate Adviser Summit October 2013

The DC landscape • The long-term shift in the landscape places greater prominence on DC • There are 36,000 occupational micro DC schemes • Active membership is expected to increase significantly as automatic enrolment is introduced

Anticipated growth of the major DC segments Total active membership in DC schemes through staging *central estimate Source: The Pensions Regulator projections

The DC journey January 2011 - published discussion paper ‘Enabling good member outcomes in work-based pension provision’ reviewed DC regulatory strategy to tackle current and future challenges in the DC landscape, particularly impact of automatic enrolment from 2012 identified six elements necessary to achieve good member outcome of adequate income in retirement appropriate contribution decisions appropriate investment decisions efficient and effective administration value for money appropriate retirement decisions protection of assets segmented the market based on scheme type / employer engagement assessed risk to achievement of good member outcomes for each segment

The DC journey continued • Responses to the discussion paper • Strong consensus that the six elements of a good member outcome were right • Suggested that we refine the segmentation approach • We challenged industry to define how they might: • Embrace voluntary accreditation of auto-enrolment schemes • Better enable trustees and employers to compare value for money from schemes • Better clarify accountabilities in DC provision • November 2011 – published six DC principles • Standards and characteristics of a good DC scheme • June 2012 – published draft DC features • Features that underpin the six DC Principles • January 2013 – DC consultation • DC code, regulatory guidance, regulatory approach

TPR/DWP joint publications revised timetable – Proposal Lay DC Code DC Code “made” DC Regulatory Strategy published Consultation response published DC Regulatory Guidance DC Code Summary Compliance & enforcement policy targeted consultation DC Toolkit modules Employer and Adviser guides & Management Committee Guidance C&E Policy published July August September October November Quality Standards Call for Evidence Defined Ambition & Quality Standards

Our regulatory approach • We are committed to increasing confidence and participation in work-based pensions To promote, and improve the understanding of, the good administration of work-based schemes To protect the benefits of members of work based pensions EDUCATE ENABLE ENFORCE Enable good member outcomes Prevent serious loss Risk tolerance Guidance Trustee toolkit Regulatory statements Thematic reviews Use of powers Web tools Codes of practice

Topics for discussion • Good member outcomes • Pension liberation fraud • Small schemes • Retirement choices • Value for money • Anything else?

Appropriate contribution decisions Appropriate investment decisions Appropriate decumulation decisions Adequate retirement income Effective and efficient administration Value for money Protection of assets Good member outcomes

Small schemes Base: All DC schemes (152); *All DC schemes that document their internal controls (110)

Retirement choices Current initiatives to drive better member outcomes • ABI code of conduct on retirement choices/annuity window • DWP/HMT OMO review group • FCA thematic review of annuity market • Money Advice Service guide • TPR revised retirement guidance Longer term • Re-thinking decumulation • Effective de-risking • Emergence of Managed DC • Innovative product development when scale is reached

Value for money A scheme offers value for money where member-borne costs and charges deliver good value in relation to the benefits provided to members, relative to other options available in the market The regulator’s role: Working with the market, to deliver an approach that allows employers and trustees to undertake meaningful value for money assessments on an ongoing basis. The regulator does not seek to specify what represents value, but will seek to intervene where employers and trustees are frustrated in their ability to assess it.

Value for money continued • Progress is required so that: • All costs and charges (product and scheme) are captured and consistently reported • Costs and charges are attributable to specific benefits • Investment returns are captured and their benefits relatable to costs • Comparison via benchmarking is facilitated • However: absent effective demand-side pressure – even this may not be enough, hence the DWP’s consultation on a charge cap for qualifying schemes.

Value for money: a potential process Do similar schemes with similar charges deliver similar benefits? What are my members getting? What are my members paying? Trustees/employer; negotiate/change provider/do nothing Do similar charges deliver similar outcomes? TPR Publish Segmented Data This presentation remains the property of The Pensions Regulator. The contents of these slides should not be reproduced without express permission.

Enabling good outcomes for members of DC schemes Andrew Warwick-Thompson Executive Director, DC Governance and Administration Corporate Adviser Summit October 2013