Housing Credits

Housing credits are vital for financing affordable housing. They provide tax benefits to investors while ensuring low-income units are developed. The program allows for various tax credit rates (9% and 4%) based on project specifics. With current volume caps in place, developers can strategize partnerships and syndication for funding. Local governments can help by offering financial incentives and streamlining processes to promote housing development. This overview explores credit calculations, bond options, and challenges faced by developers today.

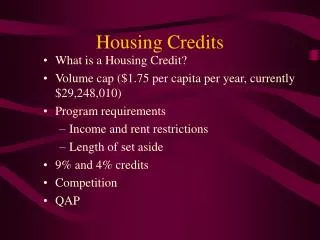

Housing Credits

E N D

Presentation Transcript

Housing Credits • What is a Housing Credit? • Volume cap ($1.75 per capita per year, currently $29,248,010) • Program requirements • Income and rent restrictions • Length of set aside • 9% and 4% credits • Competition • QAP

Housing Credit Syndication • Tax credit received annually for 10 years • Requires entity with tax liability to join partnership • For profit limited partnership formed • Developer (for profit or non-profit) is general partner with .01% ownership • Investor(s) with tax liability become limited partners with 99.99% ownership • 99.99% of tax credits flow to limited partners, who pay funds up front in exchange for 10 years of tax credits

Tax Credit Calculation • Net Equity = Eligible basis (project cost less land and other ineligible items such as federal funds)x DDA/QCT factor (130%)X Credit rate (9% or 4%)X % Low Income UnitsX 10 (number of years credit granted)X 99.99% (% sold)X Current syndication rate

9% Tax Credit Example • $11,000,000 total project cost • $1,000,000 land and other ineligible costs • Not located in QCT • 90% low income • $10,000,000 eligible basisX 8.01% (current 9% credit rate)X 90% low income = $720,900 annuallyX 10 yearsX $0.80 syndication rateX 99.99% = $5,766,623 (52% of cost)

Bonds for Rental Housing • Bond volume cap ($75 per capita per year, currently $1,253,486,175 - not all housing) • Loan program • Credit enhancement • Private placement • Difficulty of program • Expensive cost of issuance • Automatic 4% tax credits (50% test)

4% Tax Credit Example • $11,000,000 total project cost • $1,000,000 land and other ineligible costs • Not located in QCT • 90% low income • $10,000,000 eligible basisX 3.43% (current 4% credit rate)X 90% low income = $308,700 annuallyX 10 yearsX $0.82 (syndication rate)X 99.99% = $2,531,087 (23% of cost)

HOME CDBG Federal Home Loan Bank Essential function bonds 501c3 bonds CRA SHIP SAIL Section 8 PHA Capital Funds Property tax exemption Other Programs

Today’s Challenges • Astronomical insurance costs • High real estate taxes • No annual rent increases • Utility costs increasing • Lack of suitable, affordable land • Minimal opportunities for additional subsidy

What Local Government Can Do: • Provide significant financial incentives • Recognize more subsidy per deal may be required; which may mean less overall production • Waive fees (especially school board) • Consider tax exemption

What Local Government Can Do: • Combat NIMBYism • Shorten permitting time frames • Align funding cycles (i.e., County HOME program) • Work with the municipalities within Broward County to enact similar strategies