Download

1 / 34

350 likes | 626 Vues

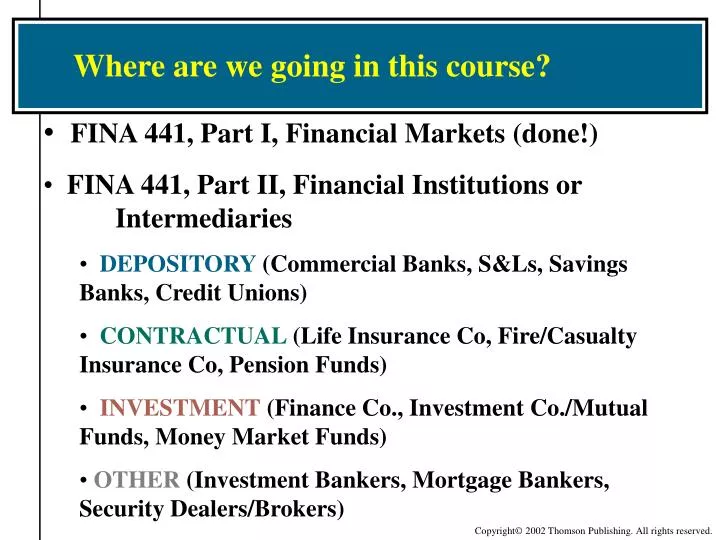

Where are we going in this course?. FINA 441, Part I, Financial Markets (done!) FINA 441, Part II, Financial Institutions or Intermediaries DEPOSITORY (Commercial Banks, S&Ls, Savings Banks, Credit Unions) CONTRACTUAL (Life Insurance Co, Fire/Casualty Insurance Co, Pension Funds)

E N D

Where are we going in this course? • FINA 441, Part I, Financial Markets (done!) • FINA 441, Part II, Financial Institutions or Intermediaries • DEPOSITORY (Commercial Banks, S&Ls, Savings Banks, Credit Unions) • CONTRACTUAL (Life Insurance Co, Fire/Casualty Insurance Co, Pension Funds) • INVESTMENT (Finance Co., Investment Co./Mutual Funds, Money Market Funds) • OTHER (Investment Bankers, Mortgage Bankers, Security Dealers/Brokers)

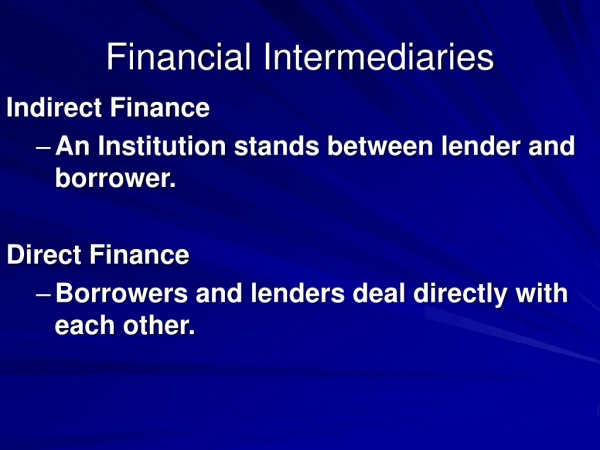

FINANCIAL INTERMEDIARIES DIRECT- involves only one contract between lender & borrower- called dis-intermediation- E.g. you loan money to your neighbor SEMI-DIRECT- Involves essentially one contract but . . .- A middle party is needed to execute it- E.g. you buy Intel stock through Charles Schwab from your neighbor INDIRECT- Involves two contracts - Financial intermediary is in the middle- E.g. you deposit money in the bank which loans it to your neighbor

FUNCTIONS OF FIN. INTERMEDIARIES Maturity & Liquidity IntermediationE.g. You deposit $ in savings account, which is loaned out in a 30-yr fixed-rate mortgage to your neighbor; even though the loan won’t be paid off for many years, yet you can get your money at any time. Financial intermediaries absorb liquidity risk! Interest-rate and Inflation Risk IntermediationE.g. Bank absorbs risk from borrower locking into fixed rate for 30 years. Repackaging SizeE.g. Bank can re-package the size of a security to the level desired. Most of us don’t have $100,000 sitting around to lend to our neighbor, so many of us poor investors can pool our $. Diversification & Default RiskE.g. You deposit $ in savings account, pooled together with other investors, so that no one investor is lending to only one borrower. Depository institutions also offer government deposit insurance. In short, financial intermediaries absorb default risk. Efficiencies & SpecializationE.g. Bank is better able to invest in mortgages (legal issues, credit approval, etc.). Since the bank has specialized in this, it has economies of scale (full-time lawyers, appraisers, credit specialists, etc.) Clearing House for PaymentsE.g. financial intermediaries make possible EFT, credit/debit cards, checks, etc. which wouldn’t exist otherwise

Role of Financial Institutions Types of Depository Financial Institutions Commercial Banks Total Assets $14.1T (2009) Savings Institutions Total Assets $1.3 T Credit Unions Total Assets $0.9 T

Commercial Bank Operations 17

Commercial Bank Consolidations Today there are half as many banks as there were in 1985. Today, the largest 100 banks control 75% of bank assets vs. 50% in 1985.

Bank Participation in Financial Conglomerates • Impact of the Financial Services Modernization Act (1999) • Prompted by the Citicorp-Traveler’s merger • Gave more freedom to merge and offer a range of financial services • Insurance • Securities services • Many banks are now subsidiaries of a financial conglomerate

Bank Participation in Financial Conglomerates • Benefits of diversified services • To Individuals: they can obtain all their financial services at a single place (one stop shop) • Deposits • Loans • Investing (brokerage) • Insurance • To Businesses: they can obtain loans, issue stocks and bonds, and have their pension fund managed by the same institution

Bank Participation in Financial Conglomerates • Benefits of diversified services to the financial institution • Reduce reliance on demand for single service • Economies of scale and scope • Diversification (service and geographical) may result in less risk • Generate new business • Risks of conglomerates: too big to fail NOTE: there are bills currently before Congress now that would split big banks and their diversified services. This is an attempt to prevent the “too-big-to-fail” syndrome.

Sources of Funds (right hand of Balance Sheet) Source: Federal Reserve, 2012

Bank Sources of Funds • Transaction deposits • Demand deposit account • Checking account that does not pay interest • Negotiable order of withdrawal (NOW) account • Interest-bearing checking account • Requires larger minimum balance • Savings Deposits • Passbook savings • Regulation Q until 1986 – max. interest rate • Auto Transfer Service (ATS) created in 1978 allows ZBA accounts and overdraft protection.

Bank Sources of Funds • Time Deposits (have specific maturity) • Retail certificate of deposit (CD) • No secondary market • Early withdrawal penalty • New: Bull-market, bear-market and callable CDs • Negotiable CD • Short-term, minimum $100,000, usually $1m, no FDIC insurance • Marketable -- can trade among investors via dealer • Money Market Deposit Accts (MMDAs) • More liquid than CDs with no maturity • Limited check writing (e.g. 5 per month) • Created in 1982 with Garn St. Germain Act

Bank Sources of Funds • Federal Funds Purchased • Short-term loans between banks (usually 1-7 days), often to meet reserve requirements (most report weekly on Wed.) • Allows banks to borrow S/T (seasonal, etc.) or may provide a S/T investment • Interest rate is the Federal Funds Rate, typically above the T-bill rate since small amounts of liquidity and default risk may exist. • Borrowing from the Federal Reserve Banks • Borrowing at the discount window, which is discouraged • Discount Rate (usually 1% higher than Fed Fds Rate) • Intended for meeting temporary short-term reserve requirement needs • Must get Fed approval, Fed may frown at you

Bank Sources of Funds • Repurchase agreements • Sale of T-bills (usually) by bank to a business with excess cash and an agreement to repurchase the securities at a later date and higher price • Source of funds for a few days for the bank • Collateralized by the Treasury bills • Form of paying interest on large customer checking balances (Rogers Elementary!)

Bank Sources of Funds • Eurodollar borrowings • Banks outside the United States make dollar-denominated loans (maybe even to US banks) • Eurodollar market is very large (Saddam Hussein was caught with a briefcase full of what?) • Bonds issued by the bank • Like other businesses, banks issue bonds to finance long-term fixed assets • Usually subordinated to deposits

Bank Sources of Funds • Bank capital • Represents amount of equity stockholders have • Obtained from issuing stock and retaining earnings • The more capital, the more “safe” the bank is because capital is a buffer to absorb future losses • Banks often resist building up too much capital because it lowers the return on equity (ROE). Stated another way, the more leverage the bank, the more ROE is magnified. • Capital is usually approx. 6-12% of assets but it really depends on risk-based capital requirement and size of bank • Primary capital (stock & RE) is of higher quality than secondary capital (subordinated notes & bonds)

Bank Capital Regulation A major reason banks failed during the financial crisis because of inadequate capital. Basel III (or the Third Basel Accord) is a global regulatory standard on bank capital adequacy, stress testing, and market liquidity risk agreed upon by the members of the Basel Committee on Banking Supervision in 2010–11, and scheduled to be introduced from 2013 until 2018. (Basel is a town in Switzerland where they meet.) Basel III strengthens bank capital and introduces new regs on liquidity and leverage.

Uses of Funds (left hand side of balance sheet) Source: Federal Reserve, 2012

Uses of Funds by Banks • Cash and “due from” balances at institutions • Currency/coin provided via banks • Reserve requirements imposed by Fed • Due from Fed and vault cash count as reserves • Hold cash and due from balances to maintain liquidity and accommodate withdrawal requests by depositors

Uses of Funds by Banks • Bank Loans (59% of assets) • Types of business loans • Working capital loans (business operating cycle) • Term loans • Purchasing fixed assets • Protective covenants & conditions • Informal line of credit (bank not obligated to lend) • Revolving credit loan (bank obligated)

Uses of Funds by Banks • Bank Loans • Loan participations (syndicates) • Sometimes large firms seek to borrow more money than an individual bank can provide • Lead bank will organize the syndicate • Loans supporting leveraged buyouts • Banks charge a high loan rate • Monitored by bank regulators • Highly-leveraged transactions (HLTs) where debt ratio > 75%.

Uses of Funds by Banks • Bank Loans • Collateral requirements on business loans • Increasingly accepting intangible assets • Important to service-oriented firms which have few hard assets • Increased lending risk with service businesses--telecomm • Types of consumer loans • Installment loans (cars, furniture, etc.) • Credit cards • Usury laws • Real estate loans

Bank Prime Rate Over Time • Theoretically, the prime rate is the rate charged to most creditworthy customers – moves in tandem with Fed funds rate, often 3% above. http://research.stlouisfed.org/fred2/series/MPRIME?cid=117

Uses of Funds by Banks • Investment securities (bank income and liquidity) • Treasury securities • Government agency securities • Corporate and municipal securities • Investment grade only • Federal funds sold

Uses of Funds by Banks • Repurchase agreements • Eurodollar loans • Branches of U.S. banks located outside of the U.S. • Foreign-owned banks • Fixed assets • Office buildings • Land

Off-Balance Sheet Activities • Loan commitments • Obligation of bank to provide a specified loan amount to a particular business upon request • Banks earn fee income for risk assumed • Standby letters of credit (SLC) • Backs a customer’s obligation to a third party • Banks earn fee income

Off-Balance Sheet Activities • Forward contracts in foreign currency • Agreement between a customer and bank to exchange one currency for another on a particular future date at a specified exchange rate • Allows customers to hedge their exchange-rate risk

Off-Balance Sheet Activities • Interest rate swap contracts • Two parties agree to periodically exchange interest payments on a specified notional amount of principal • Banks serve as intermediaries or dealer and/or guarantor for a fee • Credit default swap contacts • Privately negotiated contracts to protect investors against the risk of default on debt securities

Baker Boyer Bank • In the 1800s, Walla Walla was the largest city in the Northwest and the financial and cultural center of the NW region (and it almost became the state capitol). • Baker Boyer Bank (BBB) was founded in 1869, twenty years before Washington became a state. The bank really started as a mercantile store where gold miners would keep their gold in the store’s safe. As much as $40,000 in gold would be left in the safe for more than a year, and though it wasn't common to give or ask for receipts, no losses were ever suffered. • At one point in 1911, the BBB building was the tallest building west of the Mississippi River. • During the banking crisis of the 1930s, most banks were forced to close, at least temporarily. But BBB was determined to remain open, even though it had been ordered closed. BBB allowed customers to use the back door of the bank until banks were allowed to reopen. • BBB is still partly owned by the families of the original founders, Dorsey Baker and John Boyer. Today the president and CEO of BBB is the great-great-granddaughter of Dorsey Baker. 1911, tallest building west of the Miss. River Megan Clubb, President & CEO

Banner Bank • Banner Bank (BB) started in the 1890 (one year after Washington gained statehood and two years before the founding of WWU). • For most of its history, it was known as First Washington Bank and remained a small, community-based bank in Eastern Washington. • In 1995, the bank did an IPO and become a public company traded on the Nasdaq (ticker of BANR). • Since then, the bank has pursued a path of tremendous growth through mergers/acquisitions. • Today it has expanded to 85 branches in 28 counties throughout WA, OR and ID. • In 2000, the bank changed its name to Banner Bank. WW Headquarters Bank in Boise