FHA Update

FHA Update. Florida Association of Mortgage Brokers Miami Chapter February 18, 2009 Selene Proenza FHA Customer Liaison FHA - Office of Business Development (305) 520-5066 Selene.proenza@hud.gov. FHA’s Role in the Mortgage Market.

FHA Update

E N D

Presentation Transcript

FHA Update Florida Association of Mortgage Brokers Miami Chapter February 18, 2009 Selene Proenza FHA Customer Liaison FHA - Office of Business Development (305) 520-5066 Selene.proenza@hud.gov FHA - Serving Homebuyers Since 1934

FHA’s Role in the Mortgage Market • The FHA-insured share of all home purchases has been above 17 percent since July 2008. • It has not been this high since 1990. • The FHA share of new home sales is 24 percent. • FHA’s mortgage market share is somewhere between 25 and 30 percent, based on dollar volumes. • In 2006 it was around 2 percent.

FHA’s Role in the Mortgage Market(Source: US Department of HUD, National Association of Realtors, and US Bureau of the Census)

FHA’s Role in the Community • Help families achieve their “American Dream” (Homeownership) • First-time homebuyers • Minority groups • Elderly and disabled • Create an educated consumer – housing counseling • Stabilize and rehabilitate communities • Promote economic growth • Preserve neighborhoods • Help increase the value of the property (Equity)

Welcome to FHA MISSION STATEMENT “Promote affordable housing by helping people underserved in the private sector with homeownership, rental housing and health care facilities. We will accomplish this by providing consumer education, quality mortgage insurance products to the financial and real estate communities and best-in-class customer service.”

Welcome to FHA Office of Business Development Strategic Customer-Focused Mission “To strategically align with and tactically support FHA industry customers while educating the end user community about the value of FHA programs.” • Customer-centric business model • Cross-functional teamwork and matrix management • Coordinated approach to the market

► FHA Business Model Consumers • Homebuyers • Developers The Market FHA Customers • Lenders • Industry Influencers FHA Listening Posts Marketing Channels Customer Liaison Team MAR-COM Team HOC/Field/ HQ Market Research Web Portal Dynamic Customer Knowledge Customer/Industry Intelligence • Customer Requirements, Needs, Preferences , Expectations • Evolving Industry Patterns K.P.I.s Process and Technology Enabling Infrastructure • FHA Business Processes − Business Process Reengineering • CRM, Business Intelligence Apps ►

FHA Outreach & Education Investments in New Programs and Infrastructure −SAS business intelligence − Upgrading of GIS mapping capability 1. Customer Liaison 2. Market Data & BI − Lender-focused − Geographic coverage by named customer − 4-tiered program Systems 5. Systems 3. Marketing & Communications − Co-Branding − Advertising campaign − FHA.gov 4. Quality /BPR − New Web Portal − New Customer Relationship Management (CRM) − Lean office BPR − Customer participation in re-engineering

Customer Liaison Program • Geographic coverage by named customer • Four-tiered program − Strategic: Senior Customer Liaison − Customer Advocate − Tactical: Customer Liaison − Day-to-day: 1-800-CALL-FHA − 24x7: FHA.gov Resource Center (1-800-CALL-FHA) Customer Liaison Senior Customer Liaison Customer FHA.gov

Customer Liaison Program continued • Primary point of contact for: −Strategic planning −Marketing communications and planning − Communicating customer concerns to policymakers − Training, education, and brand awareness building − Major event support − Timely FHA-related information • Handle origination, servicing, and asset management issues • Support training and education delivery • Event support • Distribute FHA information to customers • Support Senior Customer Liaisons Resource Center (1-800-CALL-FHA) Customer Liaison Senior Customer Liaison Customer FHA.gov • Information source • Self-service– automated process • Solve day-to-day issues

What is FHA? An FHA-insured mortgage is a viable option for all. A mortgage product tailored to the buyer's needs benefits everyone… • The homeowner can afford the payments – low costs • The homeowner is happy and satisfied • A happy homeowner refers family and friends to you, their real estate agent or broker 1-800-Call FHA FHA - Serving Homebuyers Since 1934

FHA was established in 1934 and became a part of the U.S. Department of Housing and Urban Development in 1965 FHA is the U.S. Government’s largest insurer of loans - 4.68 million loans in portfolio FHA offers mortgage insurance to protect lenders in event of borrower default The insurance protection allows lenders to originate mortgages to those who may not qualify under conventional guidelines FHA does not: Originate, close, fund, or service loans Set the interest rate Determine fees and charges Have income limits FHA Overview

What About FHA Loans? • Let FHA Loans Help You & Your Buyer • Find an FHA-approved Lender FHA - Serving Homebuyers Since 1934

Advantages for Buyers Smaller Down Payment – 3½% Flexible Down Payment Sources - evidence No Maximum Income or Sales Price Limits – (Subject to Maximum Loan Limits) Buyer doesn’t need to have perfect credit No Prepayment Penalty Loss Mitigation options Standard MIP 1-800-Call FHA FHA - Serving Homebuyers Since 1934

FHA Benefits • Fully Amortizing Loans – Fixed & ARM • Automated and Manual Underwriting • Traditional and non-traditional credit • Low Down Payment – can be Gifted or Borrowed • Assumable loan • Ability to Streamline Refinance without Credit Qualifying • Loss Mitigation options – financial incentives for lender FHA - Serving Homebuyers Since 1934

Borrower Characteristics • Owner-Occupant only • Co-borrowers (occupying and non-occupying) • Co-signers • Citizenship not required; SSN is required • No maximum age • No income limits

FHA Modernization Legislation Housing and Economic Recovery Act of 2008 • Changed Down Payment – 3½% (Loan Amount is 96.5% of SP or Appraised Value, whichever is less) • Eliminated Seller-funded Down Payment Assistance • Moratorium on Implementation of Risk-Based Premiums – protect the borrower

FHA Modernization Legislation • Condominium Project Approvals – eliminates environmental review • Tax Credit for first-time homebuyers • HECM for Purchase – seniors can purchase a home and convert to HECM in single transaction thus reducing closing costs • HECM Maximum Loan Limit - $417,000 • HECM Counseling Requirements – only trained and tested counselors who follow uniform protocols • Independence of HECM Mortgage Originators – requires all parties participating in origination to be approved by FHA • Prohibition against requirements to purchase additional products as a condition for HECM eligibility

FHA Modernization Legislation • Energy Efficient Mortgages –increases amount of home modification costs that can be included in mortgage to 5% of property value • Mfg. Housing (Title I) – Raised Maximum Mortgage amounts to: - $25,090 for Repair/improvements - $69,678 Unit - $92,904 Unit and Lot - $23,226 Lot only

FHA Modernization Legislation • FHA Rescue Plan – Authorizes a new FHA “Hope for Homeowners” program to refinance existing borrowers into fixed-rate FHA mortgage products (only for loans originated on or before January 1, 2008) • Neighborhood Stabilization Program – State block grant funds to be spent for the redevelopment of abandoned and foreclosed homes and residential properties

What This Means for You? • Higher Income Limits, Higher Sales Prices, Larger Loan Amounts • Client and Market Expansion • More opportunities for the Industry • More business for you! • More Options for More Consumers • More Sensible Mortgage Products • Simplification of Lending Process FHA - Serving Homebuyers Since 1934

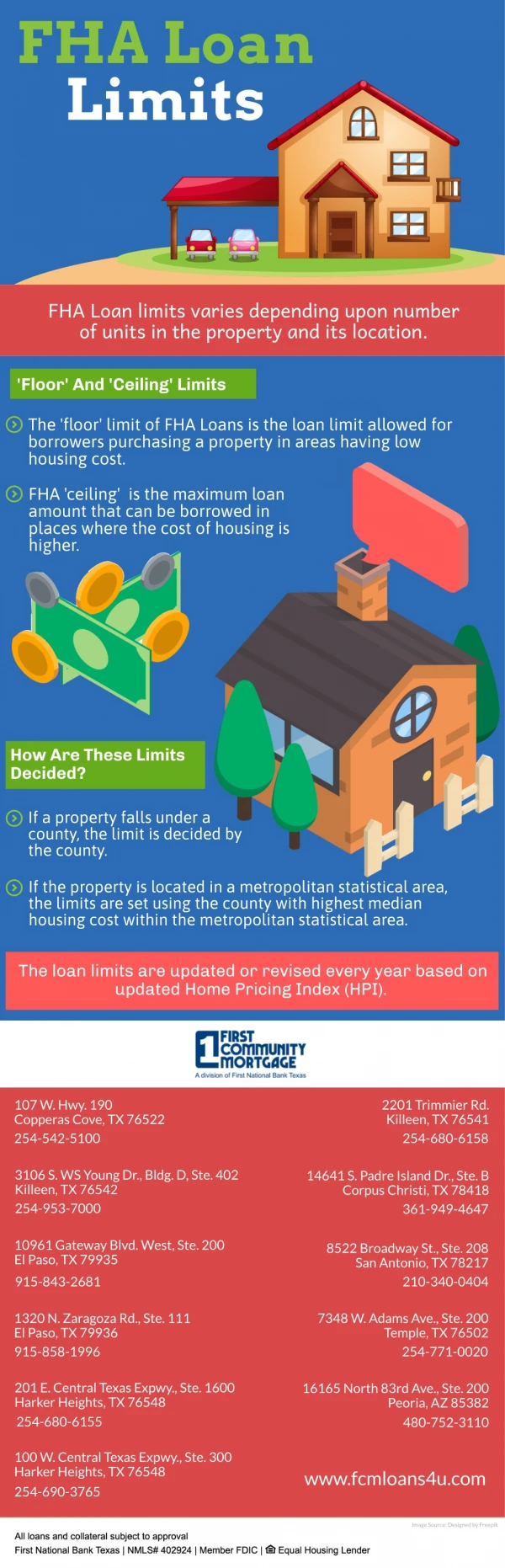

FHA Mortgage Limits • Established by law and based on the Metropolitan Statistical Area • Revised on January of each year https://entp.hud.gov/idapp/html/hicostlook.cfmwww.hud.gov

FHA Programs/Products • 203(b) - Fixed Rate/ARMs (most popular) -Purchase -Refinance – Cash-out (95%) • 234 (c) -Condominiums • 203(k) - Rehabilitation -Standard -Streamlined • HECM for Purchase (“Reverse Mortgage”) • Energy Efficient Mortgage • HUD Homes - REOs • Manufactured Homes FHA - Serving Homebuyers Since 1934

Standard (structural) Repairs/Improvements must be at least $5,000 Consultant required Architectural Exhibits required Borrower can make repairs/improvements if qualified Streamlined (minor) Facilitate uncomplicated repairs/improvements No consultant required No architect required Borrower can make repairs/improvements if qualified Include up to $35,000 FHA Programs/Products: Rehabilitation Mortgages

FHA Programs/Products: Home Equity Conversion Mortgage (HECM) • Borrower – seniors age 62 or more • Reverse Mortgage counseling required • Property – 1-4 family dwellings, existing only • Owner–Occupied only; within 60 days from closing • FHA’s Property Flipping prohibitions apply • Repayment not required until home is no longer occupied by borrower (nursing home, death). At that time, if the value has declined so that there is insufficient equity to repay FHA, then FHA will take the loss. If the value has increased over and above what is owed to FHA, that excess will be distributed to the heir(s).

FHA Programs/Products: Energy Efficient Mortgage (EEM) • Eligible for new or existing 1-4 family units • Maximum Loan in Area Can Be Exceeded by the EEM Amount • Eligible for use with Rehabilitation Mortgages (203K) • Available for Condos and Manufactured Homes • Cost of improvements that may be eligible for financing is either 5% of the property’s value (not to exceed $8,000) or $4,000, whichever is greater.

Selling HUD Homes • What are HUD Homes? • Register to Sell HUD Homes • Electronic Internet Bidding • Current Listings • Management & Marketing Contractors

What Are HUD Homes? • HUD-owned houses are often referred to as “HUD Homes.” HUD Homes are houses that had an FHA-insured mortgage and the homeowner defaulted. The lender then deeded the home to the Secretary of HUD in exchange for an insurance claim payment.

It’s Easy to Sell HUD Homes • Brokers can register with HUD’s M&M Contractor for Florida properties, National Home Management Solutions through their website, www.nhmsi.com • Once completed, the broker can show, advertise, and submit offers on HUD Homes • HUD pays the broker a commission of up to five (5) percent • HUD-registered brokers and their agents are able to submit bids 24/7 over the Internet. Electronic bidding is the only method to submit bids for HUD Homes

How to Become a HUD-Approved Lender FHA Lender Approval Types: (Six Types of FHA Lenders) • Nonsupervised Loan Correspondent Mortgage Broker, Mortgage Lender or Correspondent Lender • Nonsupervised Mortgagee Mortgage Lender & Correspondent Lender • Supervised Mortgagee Banks and Credit Unions

How to Become a HUD-Approved Lender • Supervised Loan Correspondent Banks and Credit Unions • Investing Mortgagee Entities that only want to own FHA loans • Government Mortgagee Federal, State and Local Agencies

Ways Lenders Can Participate in FHA Loan Programs • Originate All lender types can originate except Investing Mortgagees • Underwrite Single Family Loans Supervised, Nonsupervised and Government Mortgagees can underwrite once they obtain DE (Sponsor Mortgagee) approval from one of the Single Family Homeownership Centers

Ways Lenders Can Participate in FHA Loan Programs • Underwrite Mutifamily Loans Supervised, Nonsupervised and Government Mortgagees can underwrite once they obtain MAP approval from Multifamily Headquarters • Service Supervised, Nonsupervised and Government Mortgagees can service all types of loans. • Hold All types of lenders can hold (own) except Loan Correspondents

Ways Lenders Can Participate in FHA Loan Programs Non-supervised Loan Correspondent • Only one for mortgage brokers to originate • Correspondent lenders and mortgage lenders who only want to originate Non-supervised Mortgagee • In addition to origination: can underwrite, service and own any type of FHA loan

Ways Lenders Can Participate in FHA Loan Programs Supervised Loan Correspondent For banks, savings bank and credit unions that only want to originate FHA loans Supervised Mortgagee For banks, savings bank and credit unions that want to originate, underwrite, service and own any type of FHA loan.

Ways Lenders Can Participate in FHA Loan Programs Government Mortgagee Government agencies that want to originate, underwrite, service and own FHA loans Investing Mortgagee Any entity that only wants to own FHA insured loans

How to Become an FHA-Approved Lender • The FHA lender approval requirements vary from different levels and types of lender participation • The first step is to obtain an application package: • Title II Lender Application Package (for home purchases, refinances and reverse mortgages) • Title I Lender Application Package (for home improvement loans)

Title II Mortgagee Application Package • Cover Sheet - Payment of Title II mortgagee application fee - $1,000 fee except for Gov’t mortgagee • Application Form for lender approval - HUD 11701 • Handbook 4060.1 - Approval requirements & procedures

Title II Lender Application Package – Cover Sheet • APPLICATION FEE for TITLE I LENDER APPROVAL • This form MUST accompany all application fee payments. Mail this form and your • check to: HUD, P. O. Box 198608, Atlanta, GA 30384. A copy should be included with • your application. • ____________________________________________________________ Lender Name • ________________________________________Federal Tax Identification Number - 10 • digit • _______________________________________ HUD/FHA Identification Number - 10 • digit • (if applicable) • Type of application: (please check the appropriate box) • _____ Initial Application ($1,000) • _____ Additional Branch ($300) • _____ Additional Sponsor ($300) • _____ Conversion of Mortgagee Type ($300) • Lenders seeking first time approval (initial applications) must enter their federal tax • identification number in the memo portion of the check. Lenders filing all other types • of applications should put their 10 digit HUD/FHA identification number in the memo • portion of the check.

Form HUD-11701 Application for Approval: FHA Lender and/or Ginnie Mae Mortgage-Backed Securities Issuer U.S. Department of Housing and Urban Development Federal Housing Administration and Government National Mortgage Association OMB Approval No. 2503-0033 (exp. 09/30/2010) Public reporting burden for this collection of information is estimated to average 1 hour per response, including the time for reviewing instructions, searching existing data sources, gathering and maintaining the data needed, and completing and reviewing the collection of information. The information requested on this form is required by 24 CFR Part 202 and Sec. 306(g) of the National Housing Act or by HUD Handbooks 4060.1 and 5500.3. The information collected assists FHA and Ginnie Mae in determining which lenders should be approved to participate in the FHA single and multifamily insurance programs and/or the Ginnie Mae Mortgage-Backed Securities Program. It is used to help FHA minimize its risk in insuring single-family and multifamily mortgages and Ginnie Mae to minimize its risk. Applicants are not required to respond to this collection of information unless a current OMB approval number is displayed on the form. Privacy Act Statement. Names and Social Security Numbers are requested in order for the Department to obtain positive identification of the applicant’s officers, directors, stockholders and employees who have authority to obligate the applicant. The information requested will be used solely to determine the eligibility of the individuals to participate in the Department’s mortgage insurance programs. The Department is authorized to request this information by Executive Order 9397. The information collected will not be disclosed outside the Department except as required by law. The Social Security Numbers are provided to HUD on a voluntary basis. Failure to provide this information could cause delay in processing of the applications. Instructions for Completing Form HUD-11701 Applicants seeking qualification as a FHA-approved lender/mortgagee or loan correspondent under the Title I and/or Title II programs and/or as an approved issuer with the Government National Mortgage Association (“Ginnie Mae”), must complete the appropriate sections of this form. Qualified applicants may obtain one of the following three types of approval: 1. FHA Approval Only Replaces HUD-92001, 92001-D and LD Page i form HUD-11701 (11/2008) ref. Handbooks 5500.3, Rev. 1 and 4060.1

FHA Title II Mortgagee Approval Handbook 4060.1, REV-2 Chapter 2 - Part A. Requirements for all Mortgagees Acceptable Business Forms • Be a Corporation, Limited Liability Company (LLC) or Partnership that meets FHA’s Requirements • Have State License, State DBA, if applicable

General FHA Approval Requirements Owners and Officers • Cannot be debarred, suspended or otherwise ineligible (Certify via Sanction Letter) • 3 years of experience required (at least one officer) • Cannot be self employed in the mortgage or real estate industry or related field

General FHA Approval Requirements Staffing • At least two full time employees • A shared receptionist is permitted but cannot be used to meet this requirement • All employees (except shared receptionist) must be paid by W-2 • No outside or self employment in the mortgage or real estate industry or related field

General FHA Approval Requirements Office Facilities • Must be separate and apart from any other entity in commercially zoned space • Can share reception areas with other companies • Must be clearly identified to the public with a permanent business sign

General FHA Approval Requirements • Quality Control Plan except Investing Lender • Audited Financials and Adjusted Net Worth

Net Worth Requirements For Nonsupervised Applicants • $63,000 Net Worth for Nonsupervised Loan Correspondents (20% must be Liquid Assets) • $250,000 Net Worth for Nonsupervised Mortgagees (20% must be Liquid Assets)

Funding Requirements For Nonsupervised Applicants • Documented $1,000,000 funding program for its originations • Loan Correspondent applicants may provide a funding letter from their Sponsoring Mortgagee

Additional Requirements For Loan Correspondents • Must Have a Sponsoring (DE) Mortgagee to Underwrite the Originations • Sponsor (DE) can also fund the Originations • A sponsor of a loan correspondent must be a DE mortgagee. The sponsor is responsible for the actions of each of its loan correspondents in originating FHA-insured mortgages • A sponsor must supervise and perform quality control reviews of each of its loan correspondents