Download

1 / 78

780 likes | 1.16k Vues

Chapter 20 Corporations. Learning Objectives. What is a close corporation? In what circumstances might a court disregard the corporate entity (“pierce the corporate veil”) and hold the shareholders personally liable? What are the duties of corporate directors and officers? .

E N D

Learning Objectives • What is a close corporation? • In what circumstances might a court disregard the corporate entity (“pierce the corporate veil”) and hold the shareholders personally liable? • What are the duties of corporate directors and officers?

Learning Objectives • What is a voting proxy? • What are the basic differences between a merger, a consolidation, and a share exchange?

Nature and Classification • A corporation is a creature of statute. • Corporations can have one or more shareholders. • Owners can be natural persons or other businesses. • Corporation substitutes itself for shareholders.

Nature and Classification • A corporation is a creature of statute, an artificial “person.” • Can access to court systems. • Has constitutional guarantees of free speech, due process, and freedom from unreasonable search and seizures.

Nature and Classification • Corporate Personnel. • Responsibility for overall management of company rests with board of directors (elected by shareholders). • Board of directors makes policy decisions and hires officers to run corporation on a daily basis.

Nature and Classification • Corporate Personnel. • Shareholders can sue corporation and be sued by corporation and bring suit for corporation in some instances.

Nature and Classification • Limited Liability of Shareholders. • One of the key advantages of corporations is the limited liability of owners (shareholders). • In certain situations, the corporate “veil” of limited liability can be pierced, holding the shareholders personally liable.

Nature and Classification • Corporate Earnings and Taxation. • Corporate profits can either be kept as retained earnings or passed on to the shareholders as dividends. • Corporate Taxation: corporate taxes can be taxes twice, first to the corporation, then to the shareholders via dividends.

Nature and Classification • Corporate Earnings and Taxation. • Holding Companies (parent company): company whose business activity consists of holding shares in another company. • Typically holding company is established off-shore (Cayman Islands, Hong Kong, etc).

Nature and Classification • Torts and Criminal Acts. • Corporation is liable for the torts committed by its agents or officers under the doctrine of respondeat superior. • Corporation can also be liable for criminal acts, but only fined. However, responsible officers may go to prison.

Nature and Classification • Classification of Corporations. • Domestic corporation does business in its state of incorporation. • Foreign corporation from X state doing business in Z state. • Alien Corporation: formed in another country doing business in United States.

Nature and Classification • Classification of Corporations. • Public and Private Corporations. • Nonprofit Corporations. • Close Corporations: Shares held by few shareholders. • Informal management, like a partnership. • Restriction on transfer of sale and transfer of shares.

Nature and Classification • Classification of Corporations. • Close Corporations. • Management of Closely Held Corporations. • Transfer of Shares • Shareholder Agreement to Restrict Stock. • Misappropriation of Closely Held Corporation Funds.

Nature and Classification • Classification of Corporations. • “S” Corporations: avoids federal tax under IRS Code “Subchapter S.” • Avoids federal “double taxation” of regular corporations at the corporate level. Only dividends are taxed to the shareholders as personal income.

Nature and Classification • Classification of Corporations. • “S” Corporations: avoids federal tax under IRS Code “Subchapter S.” • IRS requirements: Corporation is domestic, fewer than 75 shareholders, only one class of stock, no shareholder can be a non-resident alien.

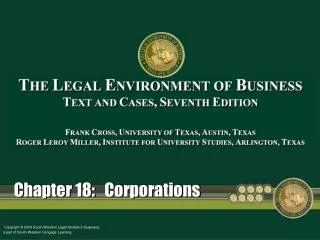

Formation and Powers • The process of incorporation generally involves two steps: • Preliminary and Promotional Activities; and • The Legal Process of Incorporation.

Formation and Powers • Promotional Activities. • Promoter’s Liability: Promoter is personally liable for pre-incorporation contracts on behalf of the corporation, unless 3rd party agrees to hold future corporation liable.

Incorporation Procedures Promotion Name Search Subscribers File Articles of Incorporation State Charter 1st Organiza-tional Meeting

Formation and Powers • Incorporation Procedures. • Selecting the State of Incorporation. • Securing the Corporate Name. • Preparing the Articles of Incorporation: which deals with shares, the registered agent and office, incorporators, duration and purpose, and internal organization. • File the Articles with State.

Formation and Powers • First Organizational Meeting to Adopt Bylaws. • After the corporation is “chartered” (created) it can do business. • At meeting, shareholders should approve the bylaws, elect directors, hire officers and ratify pre-incorporation contracts and activities.

Formation and Powers • Improper Incorporation. • De Jure: substantial statutory requirements are met; cannot be attacked by state or 3rd parties. • De Facto: statutory requirements not met, but promoters made good faith effort to comply with corporate law; can only be attacked by state.

Formation and Powers • Corporation by Estoppel. • If an entity holds itself out as a corporation to third parties, it cannot avoid subsequent liability by claiming that no corporation exists.

Formation and Powers • Corporate Powers. • Found in the corporation’s articles of incorporation, the laws of the state of incorporation, and in the state and federal corporations. • Corporate by-laws may also grant or limit a corporation’s express powers.

Formation and Powers • Piercing the Corporate Veil. • In certain situations, courts will “pierce the corporate veil” and hold shareholders personally liable in the interests of justice and fairness.

Formation and Powers • Piercing the Corporate Veil. • Factors That Lead Courts to Pierce the Corporate Veil: • (1) A third party tricked into dealing with a corporation rather than the individual. • (2) Corporation is set up never to make a profit or remain insolvent or is “thinly” capitalized.

Formation and Powers • Piercing the Corporate Veil. • Factors That Lead Courts to Pierce the Corporate Veil: • (3) Statutory formalities are not followed. • (4) Commingling of personal and corporate interests or assets.

Formation and Powers • Piercing the Corporate Veil. • CASE 20.1 Brennan’s, Inc. v. Colbert (2012). Why did the court not allow the veil to be pierced in this case?

Corporate Financing • Bonds: issued by business firms and government at all levels. • Normally have a maturity date – when principal is returned to investor. • Sometimes referred to as fixed-income securities, because bondholders receive fixed-dollar interest payments. • Bond indenture: lending agreement.

Corporate Financing • Stocks. • Common Stock: Represents true ownership of a corporation. Provides pro-rata (proportional) ownership interest reflected in voting, control, earnings and assets. Shareholders receive dividends, declared by board of directors.

Corporate Financing • Stocks. • Preferred Stock: has preferences over common stock. • Cumulative Preferred. • Participating Preferred. • Convertible Preferred. • Redeemable or Callable Preferred.

Corporate Financing • Venture Capital and Private Equity Capital. • Venture Capital: start-up businesses and high-risk enterprises need start-up and expansion capital. The start-up typically gives a share of its stock.

Corporate Financing • Venture Capital and Private Equity Capital. • Private Equity Capital: capital from wealthy investors. Ultimately, the company may sell shares in an IPO.

Directors, Officers, andShareholders • Directors. • A corporation is governed by a board of directors elected by shareholders. • Individual directors are not agents of corporation, only the board itself can act as a “super-agent” and bind the corporation.

Directors, Officers, andShareholders • Directors. • A director can also be a shareholder, especially in closely-held corporations. • Generally, the number of directors is set forth in the articles of incorporation. • Directors appointed at the first organizational meeting, usually for a year.

Directors, Officers, andShareholders • Directors. • In closely held companies, directors are generally the incorporators and/or the shareholders. • Removal of Directors: directors can be removed for cause.

Directors, Officers, andShareholders • Compensation of Directors. • Inside director (officer), vs. outside director. • Often the same person is both an officer and director, and receives compensation as an officer.

Directors, Officers, andShareholders • Board of Directors’ Meetings. • Quorum must be present to conduct official business. • Rights of Directors. • Participate in corporate decisions and inspect corporate books and records.

Directors, Officers, andShareholders • Rights of Directors. • Compensation (usually a nominal sum). Corporation should guarantee reimbursement (indemnification) or purchase liability insurance to protect the board from personal liability.

Directors, Officers, andShareholders • Corporate Officers and Executives. • Officers serve at the pleasure of the Board of Directors but have fiduciary duties to company as well. • Their employment relationships are generally governed by contract law and employment law. • Officers may be terminated for cause.

Directors, Officers, andShareholders • Directors: Duties and Liabilities. • Directors and officers are fiduciaries and owe the company ethical and legal duties. • Duty to Make Informed and Reasonable Decisions. Directors are expected to be fully informed on corporate matters.

Directors, Officers, andShareholders • Directors: Duties and Liabilities. • Duty of Care. • Duty to Exercise Reasonable Supervision. Directors are expected to supervise officers when delegated work.

Directors, Officers, andShareholders • Directors: Duties and Liabilities. • Duty of Care. • Duty to Make Informed and Reasonable Decisions. Directors are expected to be fully informed on corporate matters. • Duty to Exercise Reasonable Supervision. Directors are expected to supervise officers when delegated work.

Directors, Officers, andShareholders • Directors: Duties and Liabilities. • Business Judgment Rule. • Immunizes a director or officer from liability from bad decisions. • Court will not require directors or officers to manage “in hindsight.” As long as decision was reasonable, informed, made in good faith and in the best interests of the corporation, BJR will apply.

Directors, Officers, andShareholders • Directors: Duties and Liabilities. • Duty of Loyalty. • Subordination of personal interests to the welfare of the corporation. • No competition with corporation. • No “corporate opportunity.” • No conflict of interests. • No insider trading.

Directors, Officers, andShareholders • Directors: Duties and Liabilities. • Duty of Loyalty. • No transaction that is detrimental to minority shareholders.. • CASE 20.2 Guth v. Loft, Inc.(1939). What were the two parts of the duty test the court used to determine whether the corporate executives had violated their duty of loyalty?

Directors, Officers, andShareholders • Directors: Duties and Liabilities. • Disclose Conflicts of Interest. • Full disclosure of any potential conflicts of interest and abstain from voting on any transaction that may benefit the director/officer personally. But if transaction was fair and reasonable, it can be approved by majority of disinterested directors.

Directors, Officers, andShareholders • Directors: Duties and Liabilities. • Liability of Officers and Directors. • May be liable for crimes and torts committed individually and/or those committed by employees under their supervision. • Shareholder derivative suits where shareholder(s) sue directors on behalf of corporation.

Directors, Officers, andShareholders • Shareholders. • Acquisition of shares grants an equitable ownership interest in a corporation. • Shareholders generally have no right to manage the daily affairs of the corporation, but do so indirectly by electing directors.