Download

1 / 36

360 likes | 544 Vues

Learning Outcomes : MFRS 3 & MFRS 136 Understand different types of goodwill Understand the accounting treatments for purchased goodwill Understand the impairment test (MFRS 136). TOPIC 6 Accounting for Goodwill.

E N D

Learning Outcomes: MFRS 3 & MFRS 136 Understand different types of goodwill Understand the accounting treatments for purchased goodwill Understand the impairment test (MFRS 136) TOPIC 6Accounting for Goodwill

Goodwill acquired in a business combination represents a payment made by the acquirer in anticipation of future economics benefits from assets that are not capable of being individually identified and separately recognised. MFRS 3

Two types: (a) Purchased Goodwill The difference between total price paid for an acquired business and the fair value of its net identifiable assets Types of Goodwill

(b) Inherent Goodwill Internally generated within the business such as valuable brands e.g. Sony, Pepsi. Sony was created over decades and it is difficult to arrive at the cost of generating these asset internally Cont.

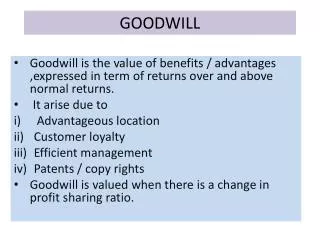

Goodwill Total price paid exceeds the fair value of net identifiable assets May denote distinctive advantage that enable a business to generate expected earnings in excess of anticipated normal earnings due to good location, technological competence, a strong management team etc. Purchased GW

Bargain Purchase The fair value of net identifiable assets exceeds total purchase price May be due to liquidation, unfavorable customer perception, ‘distressed’ firms etc. However, illogical to sell a business less than its fair value Cont.

Our previous examples on computing GW on combination assumed no premium paid by the acquirer over fair value of the acquiree in acquiring its stake. Thus, the computed GW on combination is allocated rateably between parent and NCI. Goodwill allocated rateably

It is not uncommon for acquirer to pay a premium over and above the fair value of acquirer in order to gain control The excess payment is a control premium Issue – the allocation of GW on comb to parent and NCI. It is not to be allocated rateably but as follows: First, allocate the GW to acquirer based on the difference between the FV on the consideration given (including premium paid) and acquirer’s share in FV of identifiable net assets acquired Then, the balance of the GW allocate to NCI. See example 3.1, p. 136, TLT Control premium

It arises when the acquirer pay the consideration less than the its proportionate share of the FV of the acquiree as a whole. i.e. aggregate of the FV of the consideration transferred and the NCI less than the FV of the acquiree as a whole. Thus, GW on comb will be less than the inherent GW that otherwise would be determined based on a full FV. See example 3.2, p. 136, TLT Minority interest discount

MFRS 3 – (Para 51-55) The acquirer shall, at the acquisition date: (a) recognise goodwill acquired in a business combination as an asset; and Accounting for Goodwill

(b) initially measure that goodwill at its cost, being the excess of the cost of the business combination over the acquirer’s interest in the net fair value of identifiable assets, liabilities and contingent liabilities recognised in accordance with para 36. Cont.

Para 54 After initial recognition, the acquirer shall measure goodwill acquired in a business combination at cost less any accumulated impairment losses Para 55 Goodwill acquired in a business combination shall not be amortised. Instead the acquirer shall test it for impairment annually or more frequently if events or changes in circumstances indicate that it might be impaired in accordance with MFRS136 Impairment of Assets Cont.

MFRS 136 -Goodwill is not amortized because it has an indefinite life. Instead, impairment test is performed at least annually or may be more frequent. Examples of events/circumstances that indicate impairment test must be conducted: Unanticipated competition Loss of key personnel Adverse action or assessment by a regulator Adverse change in business climate Impairment Losses

Cash-generating units (CGUs) • Where the FVLCTS < CA it is necessary to calculate the VIU of an asset to determine whether or not it has been impaired • It may not be possible to identify an individual assets VIU when the asset only has a value due to its relationship with other assets.Eg – a machine in a factory works in conjunction with the rest of the assets in the factory • Para 66 – where there is any indication an asset may be impaired, if possible the recoverable amount should be estimated…if not…determine the recoverable amount of the CGU to which the asset belongs.

Cash-generating units (CGUs) • In the previous case (i.e. a machine in a factory) the VIU of the asset must be determined in the context of the asset’s cash-generating unit (CGU) • Para 6 - Defined as the smallest identifiable group of assets (generating cash flows from continuing use) that are independent of the cash inflows from other assets or groups of assets

Identifying CGUs • Identification of CGUs requires consideration of (para 67 – 73) • How management monitors the entity’s operations; • How management makes decisions about continuing or disposing of the entity’s assets and operations See illustrative examples, p.577, Picker et al. • If an active market exists for the output of a group of assets (even if some of the output of the group of assets is used internally), this group of assets is classified as a CGU

Identifying CGUs • CGUs must be identified consistently from period to period • Identification of a particular unit within an entity is arbitrary (require judgement and consider other factors). • IAS 36 allows a segment (determined in accordance with IFRS 8 Operating Segments) to be used as a CGU where the segment equates to the smallest group of assets generating independent cash flows.

Determining the CA in CGU • Determining CA – must include all assets that directly attributable to the CGU that contribute to cash flows. • IAS36 para 76(b) – CA of CGU does not include CA of any liabilities (i.e. in computing CA not to include cash outflows). .

Impairment losses and CGUs – with goodwill • Where a CGU includes goodwill, IAS 36 contains specific requirements for accounting for the allocation of impairment losses arising in relation to the CGU • Goodwill is a residual balance, consisting of assets that cannot be individually identified or separately recognised • Therefore it is not possible to determine a FVLCTS for goodwill, or to identify cash flows relating specifically to goodwill • Rather, goodwill can only be tested for impairment at the CGU level

Cont. • Para 80 – GW on business comb is allocated to one or more CGUs. • How? Consider how internal management monitors the GW. (i.e. to be allocated to the lowest level at which management monitors the goodwill)

Cont. • Recall that goodwill is required to be tested for impairment annually (or more frequently if there is an indication that the CGU may be impaired), i.e. comparing CA of the unit’s assets, including GW, with its RA

Cont. RA > CA • No impairment loss • GW remains unadjusted (i.e. not reduced due to impairment loss) How no impairment loss for GW – entity should carry out screening test? May due to the GW protected by internally generated GW, unrecognised identifiable net assets, excess value over CA of recognised assets.

Cont. RA < CA • There is impairment loss • Para 104 – allocate the impairment loss to reduce the CA of assets of the unit / groups of units in the following order : • First – reduce the CA of any GW allocated to CGU • Then – to the other assets of the unit pro rata of the CA of each asset in the unit

Cont. RA < CA • Para 105 – some restrictions to write-down the value of individual assets in the unit: “ In allocating an impairment loss – an entity shall not reduce the CA of an asset below of the highest of : • Its FVLCTS (if measurable) • Its VIU (if determinable); and • Zero The amount of impairment loss that should would be otherwise have been allocated to the asset shall be allocated pro rata to other assets in the unit”

Example • A Ltd has identified an impairment loss of $300,000 on one of its CGUs • The CGU consists of the following assets (stated at current carrying amounts): • Buildings 500,000 • Equipment 300,000 • Land 250,000 • Goodwill 150,000 Required: • Calculate the allocation of impairment loss against all assets in the CGU.

Cont. 150,000* - 500/1,050 71,429** 428,571 42,857 300/1,050 257,143 35,714 250/1,050 214,286 300,000 1,050,000 * Remaining impairment loss still to be allocated = $150,000 ** 500/1,050 x $150,000 = 71,429

Cont. RA < CA • Refer example 15.3, p. 585, Picker et al. Note: there is criticism on impairment test when CGU has GW – it does not measure whether GW has been impaired (i.e. no subsequent test for impairment of GW). It arbitrarily allocates the loss firstly to GW. Thus, ED to IAS 36 suggested a two-step approach (refer Figure 15.11, page 586, Picker et al.)

The aggregate amount of goodwill impairment losses is presented in the income statement as a separate line item before income from continuing operation Cont.

Cont. Impairment loss is written-off against parent’s and NCI interest to the holding interest Example: H acquired 75% equity interest in S and the GW was RM40,000. The parent’s share of GW was RM32,000 and NCI was RM8,000. At the end of the year, the impairment loss of GW was RM10,000. Discuss the accounting treatment of the impairment loss. Answer: Though the parent’s share was RM32,000 which is 80% (paid controlpremium) of the full GW, the impairment loss is written-off in proportion to the holding interest, i.e. 75% and 25% Dr Parent’s income 7,500 Dr NCI 2,500 Cr GW 10,000

Current accounting standards Bargain Purchase MFRS 3 – If the acquirer’s interest in the net fair value of the identifiable assets, liabilities and contingent liabilities recognised in accordance with para 36 exceeds the cost of business combination, the acquirer shall: MFRS 3

(a) reassess the identification and measurement of the acquiree’s identifiable assets, liabilities and contingent liabilities and the measurement of the cost of combination; and (b) recognise immediately in profit and loss account any excess remaining after that assessment (para 56) FRS 3

Cont. Journal entries Dr Fair value adjustment/Bargain purchase Cr Gain on combination in PnL (to recognise gain on combination) Dr Share capital Dr Pre-acquisition reserve Cr Fair value adjustment Cr Cost of Investment (to eliminate inter-company of investment) Dr Share capital Dr Pre-acquisition reserve Cr Fair value adjustment Cr NCI in FP (to recognise NCI at acquisition date fair value)

Should the goodwill be amortized? Proponents: The goodwill are ‘used-up’ over time as the excess profits are earned & therefore should be charged against those profit. Over time, if the total of goodwill is not diminish, the goodwill is of necessity to be replaced by inherent goodwill which does not meet recognition criteria Goodwill & Amortization

Should the goodwill be amortized? Opponents: The goodwill has an infinite life that can be maintained and enhanced over time Objectivity – no clear measure of decline or of the appropriate period of amortization. Only reason to write down goodwill is when there is evidence of permanent impairment Cont.

Current accounting standards applicable to inherent Goodwill Para 48 Inherent goodwill should not be recognised as an asset and reported in SFP – does not meet criteria for asset recognition. MFRS 138 – INTANGIBLE ASSETS