Welfare Benefit Changes

This document outlines significant changes to Housing Benefit and Council Tax Benefit from 2011 to 2017. Key topics include the introduction of Local Housing Allowance (LHA) limits for private tenants, modifications to non-dependent deductions, and the transition from Housing Benefit to Universal Credit. It highlights the new criteria for benefits, such as capping rent for over-occupied homes and the impact of benefit caps on recipients. The aim is to simplify the benefits system and improve work incentives while reducing fraud and errors.

Welfare Benefit Changes

E N D

Presentation Transcript

Welfare Benefit Changes 2011 to 2017 Anne Jordan Housing Benefits Service

Overview of Housing Benefit & Council Tax Benefit Means Tested • Amount needed to live on (set amounts) compared to income • Excess income? 65% goes towards rent 20% goes towards Council Tax bill • Limit on rent payable - Local Housing Allowance

April 2011 LHA Changes – Private Tenants • Removal of £15 ‘excess’ • LHA levels set at 30th percentile - was 50th • Removal of 5 room rate (capped to 4 rooms) • Absolute caps • 1 bed £250 • 2 bed £290 • 3 bed £340 • 4 bed £400

April 2011 changes Private Tenants only • Extend the circumstances in which HB can be paid direct to the landlord • Extra room allowed for a non-resident carer Everyone • Increase in non dependent deductions • Full disregard of special guardianship order and residence order payments • Removal of the Baby premium

Non Dependant Deductions • Will be increased over the next three years to match the level had they not been frozen since April 2001 • 2010 deduction £0 to £47.75 weekly Now • 2011 deduction £0 to £60.60 weekly • Amount depends on circumstances

Housing Benefit changes 2012 to 2013 • HB for Single people under 35 restricted to Shared Accommodation Rate from Jan 2012 (£67.50 weekly) April 2013 • Changes to social housing so that claimants living in a property too large for their needs will have their HB capped • LHA will be index linked and up-rated with the consumer price index

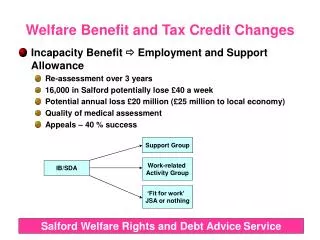

Towards 2013 • Government intentions; • simplify the system, making it easier for people to understand, and easier and cheaper for staff to administer • improve work incentives • smooth the transitions into and out of work • reduce in-work poverty • cut back on fraud and error • Incapacity Benefit to Employment Support Allowance conversion • Universal Credit

Universal Credit • Single Universal Credit to replace work-related benefits, including: • Income Support • Job Seekers Allowance (IB) • Employment Support Allowance (IB) • Child Tax Credit • Working Tax Credit, and • HOUSING BENEFIT • paid to working age claimants • Not included: • Pensioners – but housing costs for pensioners may be included within their Pensions Credit. • DLA, Child Benefit, SSP, Maternity Pay, Bereavement benefits, Carers Allowance • COUNCIL TAX BENEFIT • Exempt and temporary accommodation

Universal Credit – what do we know? • Total Maximum Benefit Cap • Single £18,000 pa • Family £26,000 pa • Those in work will have maximum benefit tapered down using a Single Taper of 65% • Commitment that no one will be worse off by utilising an initial transition scheme • Delivery model uncertain - internet & call centre suggested • Payments will not be made to landlords – including Council.

When is Housing Benefit affected? • New claims for Housing Benefit from October 2013 • Existing claims transferred across in stages until 2017

2013 onwards – what else? • Council Tax Benefit to be abolished • Possible transfer of crisis loans and social fund payments from DWP • Administration of residual housing costs which are to stay with local authorities • End to child benefit for higher rate tax payers