Download

1 / 39

420 likes | 638 Vues

The Future of Bretton Woods II. Juha Seppälä Department of Economics University of Illinois. Starting Point. Paul Krugman summarizes the current state of the U.S. economy as follows: “Americans make a living selling each other houses, paid for with money borrowed from the Chinese.”

E N D

The Future of Bretton Woods II Juha Seppälä Department of Economics University of Illinois

Starting Point • Paul Krugman summarizes the current state of the U.S. economy as follows: “Americans make a living selling each other houses, paid for with money borrowed from the Chinese.” (New York Times, 8/12/2005)

Outline of the Talk • Bretton Woods I • Bretton Woods II • Problems with Bretton Woods II (U.S. and China) • Other Players • New Chinese Exchange Rate Mechanism • Conclusions

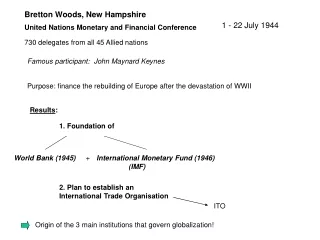

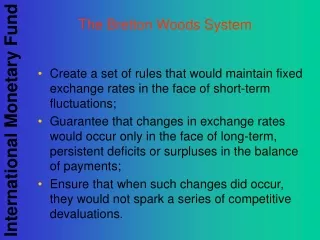

1. Bretton Woods I • The original Bretton Woods system was the system of fixed exchange rates that existed from the end of World War II (1946), until its collapse in 1971. • John Maynard Keynes was a principle architect of the Bretton Woods System. • Global financial system would have fixed exchange rates in order to prevent the beggar-thy-neighbor policies of currency devaluations that characterized the 1930’s. • The dollar could be converted to any other major currency or gold at a fixed exchange rate.

1. Bretton Woods I • The Bretton Woods System was already criticized in 1953 by Milton Friedman: • His argument was that in the face of external or internal shocks, for most economies, the most important channel of adjustment is the real exchange rate. This can adjust in two different ways: either nominal exchange rate depreciates (appreciates) or the price level decreases (increases). The first way is much less costly. Therefore, it would be best to let the nominal exchange rate be flexible.

1. Bretton Woods I • In 1960, the economist Robert Triffin, testifying before the U.S. Congress, exposed a fundamental problem in the international monetary system: • Continuous U.S. balance of payments deficits during the 1950s had provided the world with liquidity, but had also caused dollar reserves to build up in the central banks of Europe and Japan. The U.S. gold reserves were going dangerously low. • If the United States stopped running balance of payments deficits, the resulting shortage of liquidity could pull the world economy into a contractionary spiral, leading to instability. • Excessive U.S. deficits would erode confidence in the value of the U.S. dollar. Hence, it would no longer be accepted as the world's reserve currency. The fixed exchange rate system would break down.

1. Bretton Woods I • By the early 1970s, as the Vietnam War accelerated inflation, the United States was running not just a balance of payments deficit but also a trade deficit. The crucial turning point was 1970, which saw U.S. gold coverage deteriorate from 55% to 22%. • In the first six months of 1971, assets for $22 billion fled the United States. In response, on August 15, 1971, President Nixon unilaterally “closed the gold window.”

2. Bretton Woods II • “Bretton Woods II” is a term coined by three Deutsche Bank economists — Michael Dooley, Peter Garber, and David Folkers-Landau — in a series of papers in 2003–2004 to describe the current international monetary system: • In this system, the United States and the Asian economies have entered into an implicit contract where the U.S. runs current account deficits and the Asian countries keep their currencies fixed and undervalued by buying U.S. government debt.

2. Bretton Woods II • According to Dooley, Folkert-Landau, and Garber (DFG), this system has benefits to both parties: • The U.S. obtains a stable and low-cost source of funding for its current account and budget deficits, and can easily reduce taxes, fight two wars, and increase government spending at the same time. • For the Asian countries, the undervalued currency creates export-led development strategy that produces economic and employment growth to keep the lid on potentially explosive pressures rising large pools of surplus labor.

2. Bretton Woods II • At the time when DFG were writing, many countries in Asia exporting to the United States had fixed exchange rates with the United States, such as China (8.28 renminbi per dollar), or had quasi-fixed rates, such as Japan (Japan will intervene to keep the Yen above 100 per dollar). • DFG predicted that the Bretton Woods II system can last for a generation, or at least for eight years. • Remember that Bretton Woods II system lasted for 11 years after Robert Triffin presented his dilemma.

3. Problems with Bretton Woods II: Definitions • A national trade balance (surplus/deficit) is the net value of exports of tradable goods and services minus imports. • A national current account balance is the net value of exports of goods, services, assets, and transfers – minus the imports of goods, services, assets, and transfers

3. Problems with BW2: U.S. CAD • Volume of U.S. recent current account deficits (CAD): • In 2003, U.S. CAD was $530 billion. • In 2003, foreign central banks added $440 billion of dollar reserves, thus 90 percent of total U.S. CAD. • In 2004, U.S. CAD was $660 billion.

3. Problems with BW2: People’ Bank of China • U.S. absorbs 80 percent of world’s savings not invested at their home country. • The large CAD sends billions of dollars abroad, particularly to China. • People’s Bank of China uses the inflow of dollars to purchase assets, mostly U.S. Treasuries. • Much of the $400 billion fiscal deficit is financed by China. • If China stops purchasing U.S. assets and switches to Japan, Europe, or other markets, it will cause a fall in the dollar and long-term interest rates will increase.

3. Problems with BW2: Nightmare Scenario • If dollar depreciates against Renminbi by 33%, this could lead to capital losses for People’s Bank of China of nearly 10 percent of China’s GDP. • In addition, higher interest rates in the U.S. would lead to the end of U.S. housing bubble, U.S. recession, fall in U.S. imports, and finally a global recession.

3. Problems with BW2: Interest Rates • How much does the interest subsidy from the foreign central banks lower U.S. interest rates? • Goldman Sachs: CB’s narrow yields by only 40 bps. • Federal Reserve: 50 – 100 bps. • PIMCO: 100 bps. • Morgan-Stanley, Stephen Roach: 100-150 bps. • Roubini and Setser: 200 bps.

3. Problems with BW2: Interest Rates • Roubini and Setser get a larger number because they try to take into account also general equilibrium effects: • If Asian central banks purchase fewer Treasuries, this would affect the dollar, U.S. growth and inflation numbers, which all impact Treasury yields. • In addition, private investors believe that central bank purchases will inhibit currency rate movements. Hence they are more willing to invest in the U.S.

3. Problems with BW2: U.S. Financing Needs • U.S. external debt to GDP only 30 percent, though could rise to 50 percent by 2008. • Most experts believe that deficits will continue “as far as eye can see.”

3. Problems with BW2: Reducing CAD • Reducing the CAD would require either or all of: • Stronger growth in world demand. • Slower growth in overall U.S. demand. • Change in the real exchange rate. • Roubini and Setser believe that a 20 percent fall in dollar is needed to impact CAD.

3. Problems with BW2: Imports vs. Exports • Continuation of BW2 means imports rising faster than economy. • This implies resources are leaving import competing sectors toward sectors supported by low interest rates. • Imports from China are increasing 25% year on year. • By 2008, Chinese imports could be double the value of oil imports. • Exports to U.S. account for 12 percent of China’s GDP.

3. Problems with BW2: Housing Sector • Job growth in interest sensitive sectors actually exceeds losses in competing sectors. • Interest rate subsidy from Asia discourages saving. • Promotes overinvestment in housing and under-investment in tradable goods.

3. Problems with BW2: Some Numbers • In 2004, U.S. CAD was $660 billion. • Asia’s CA surplus was $313 billion. • Asia’s central bank reserves increased $535 billion. • From 2003 to 2005, China’s gross CB reserves will go from 32 to 48 percent of GDP.

Problems with BW2: Case of China • Impact of reserve growth on China: • Expanding reserves increases the money supply, fueling excess credit and bad lending. • Klitgaard finds that only half the increases in reserves from 2000 to 2003 were sterilized. • In 2004, reserve increases were $200 billion dollars, 13 percent of GDP. According to Roubini and Setser (2005), China sold only $70 billion in bonds, so only 35 percent sterilized.

3. Problems with BW2: Central Banks • Of the world’s $3.8 trillion in reserves, $2.5 trillion is held in dollars. • Asia’s central banks have $2.4 trillion in assets, with $1.8 trillion in dollars. • If a 33 percent average appreciation of Asian currencies is needed to reduce the U.S. CAD, the loss to Asia’s stock of $1.8 trillion in dollar reserves will be $600 billion. • If the dollar falls 33 percent against the renminbi, losses will be $150 billion for China, or 10 percent of their GDP.

3. Problems with BW2: Weak Structure • There are no institutional constraints on the anchor currency (dollar): U.S. can run deficits and doesn’t need gold. • In addition to maintaining dollar levels of reserves, Asian CB’s must continue to add more dollars to their reserves to absorb the additional deficits in the United States. • Roubini and Setser in their paper “Will the Bretton Woods 2 Regime Unravel Soon? The Risk of a Hard Landing in 2005-2006” (February 2005) predict that BW2 will unravel in the next couple of years.

4. Other Players: Short Maturity of Debt • Average maturity of U.S. debt fell from 90 months in 1999 to 33.4 months in Dec. 2004. • This is due to current interest rates being low. • Because of short maturities, must roll over debt. • If CB’s accumulate U.S. debt slower, U.S. Treasuries will need a lot more other buyers. • Irony: To protect dollar assets, CB’s must purchase more of those assets. Similar to stock bubble.

4. Other Players: Non-Japan Asia • In 2003, only 12 percent of new CB accumulations went to Euros and non-dollars. In 2004, estimates are 25 percent. • Korea, Taiwan, and Hong Kong hold $500 billion. • Singapore, Malaysia, Thailand, and India hold $350 billion in reserves. • If these banks adjust to euros, this would move the market.

4. Other Players: Japan • In 2003, about $200 billion of $485 billion the U.S. received in CB reserve financing came from Japan. • In 2004, this dropped to $170 billion. • Many experts believe Japan’s Ministry of Finance will intervene to keep yen weak against dollar. • However, Japan alone cannot provide all the financing the U.S. needs, and Japan will provide less in 2005 and 2006.

4. Other Players: Europe • If the European Central Bank (ECB) sold euros, that would provide one of the easiest ways to prop up the BW2 and prevent Asian CB’s from taking a large hit. • However, ECB has shown little inclination in the past to cut interest rates, let alone foreign exchange market intervention. • ECB cannot intervene as readily as China or Japan.

4. Other Players: Foreign Investors • Private investors continue to buy U.S. assets. • If they believe their home CB’s will continue to also purchase Treasuries, foreign investors will also. • However, if investors anticipate their any CB hesitance, there will be a stampede out of U.S. assets.

4. Other Players: U.S. Investors • If U.S. investors leave U.S. assets, that could unravel the system. • Since the end of 2002, U.S. residents have bought more foreign securities than Treasuries. • Total U.S. outflows could reach $180 billion in 2005.

5. New Chinese Exchange Rate Mechanism • On July 21, 2005 China moved to a new exchange rate regime. Instead of pegging the dollar, China now pegs a basket of currencies with a band of 0.3%. It is still not known which currencies (or what weights) make up the basket. • For example, for the U.S. dollar the new median value is 8.11 renminbi to the U.S. dollar (previously 8.28 — 2% appreciation).

5. New Chinese ERM: The End of BW2? • In the Wall Street Journal (8/15/2005), John Taylor (Professor of Economics at Stanford University and a former U.S. Under Secretary of Treasury for International Affairs) called this the end of Bretton Woods II and wrote: • “The new policy shift in China from a pegged to a flexible exchange rate regime starts a new chapter in international finance, comparable to the dramatic end of the Bretton Woods system of pegged exchange rates in 1971.”

5. New Chinese ERM: Maybe Not • According to Stephen Jen (Morgan Stanley), the estimated weight of the U.S. dollar is 85% or more of the basket. • During the first month of the new basket regime, USD/CNY has declined by cumulative 0.15% — half the daily allowable range. • For all practical purposes, Bretton Woods II is alive and well.

5. New Chinese ERM: Japanese Example • There are strong parallels between Japanese currency policy after World War II and Chinese currency policy today: • After two decades of pegging at 360 yen, Japan decoupled from the dollar on August 1971 and then repegged at a revalued rate of 308 yen. • After stabilizing the exchange rate at this new level for about a year, greater flexibility was introduced. • This phased adjustment resembles recent Chinese policy initiatives.

5. New Chinese ERM: The Future? • If China intends to allow a series of small appreciations in the renminbi then it either has to • Keep its interest rates below U.S. rates, so that low interest rates offset the expected return from renminbi appreciation over time (currently bank deposit rates in China are capped at 2.5%, below the 3.5% federal funds rate). • Intervene a lot. • Or do both. • Either way, this policy prevents independent Chinese monetary policy.

6. Conclusions • In any case, the new Chinese Exchange Rate Mechanism is a step to the right direction. • The United States, in contrast, has not done anything. • President Bush has not vetoed a single spending bill. The government spending has increased faster than at any time since the 1960’s (“the Great Society” welfare programs and Vietnam War). • The massive tax cuts passed in 2001–2003 are set to expire in 2008–2010.

6. Conclusions: What the U.S. Should Do? • Since these are temporary tax cuts and the likelihood they will be made permanent is low, basic economic theory tells us that their positive incentive effects are small. • Since the President and the Congress are unable to control spending, the simplest way for the U.S. to reduce its fiscal deficit (and, indirectly, current account deficit) would be to repeal the 2001–2003 tax cuts.